The sun rises in the East

2024-04-28 13:02:53 UTC+1Guten Tag

05.04.2024, US Arbeitslosenzahlen (März 2024 m/m: 3.8% -0.1%).

05.04.2024, US Arbeitslosenzahlen (März 2024 m/m: 3.8% -0.1%).

05.04.2024, US Lohnentwicklung (Stundenlohn Mittel y/y: 4.1% -0.2%).

09.04.2024, BoJ Vorsitzender Ueda, Erklärung vor dem Finanzausschuss des ‚House of Councilors‘.

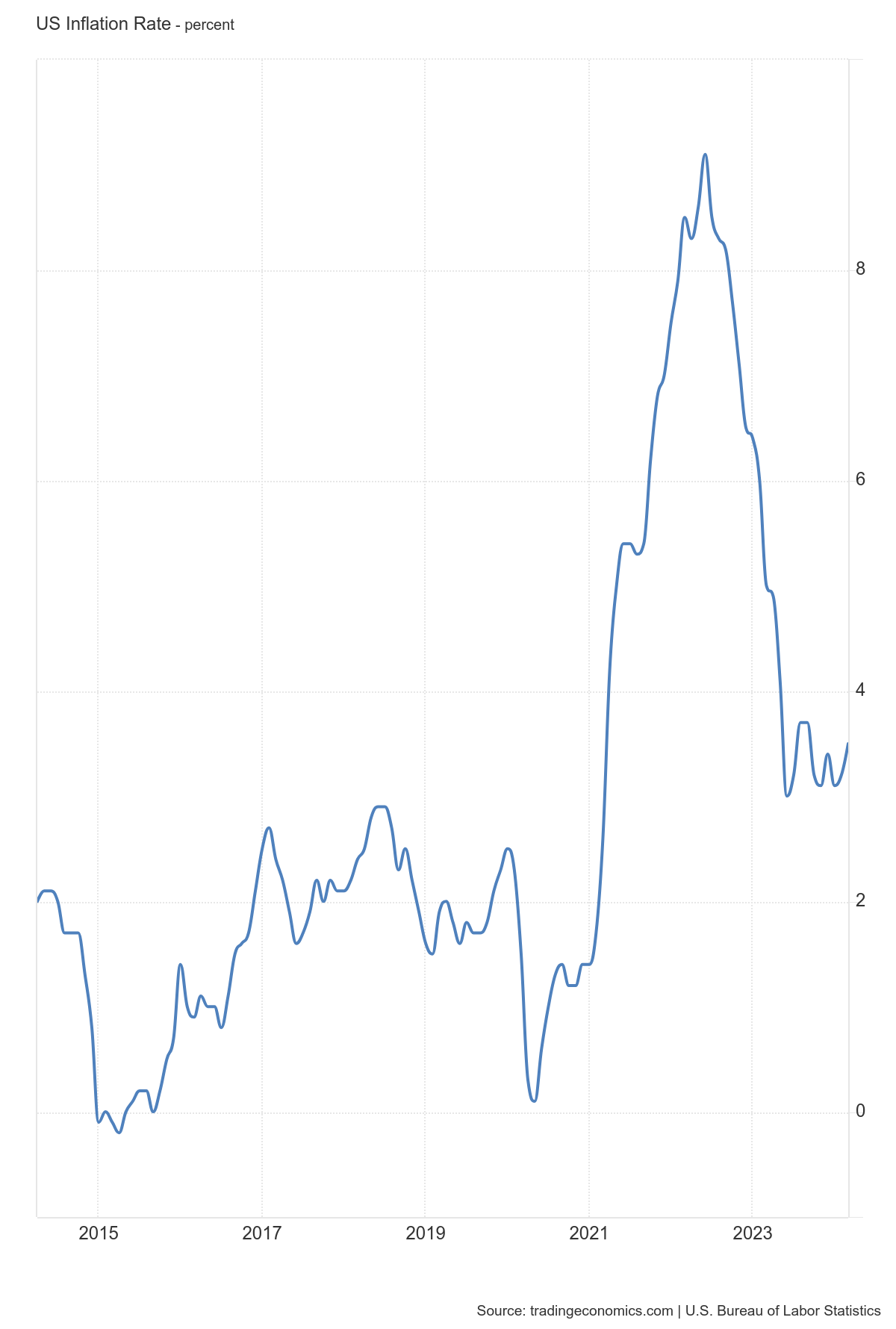

10.04.2024, US Konsumenten Preisindex (CPI, s.a.) (1982-1984=100, 312.23 points).

10.04.2024, Geldpolitischer Beschluss der Bank of Canada (Leitzinssatz: 5.00% +/- 0.0).

10.04.2024, US FED Protokoll des Federal Open Market Committee (19.-20. März 2024).

11.04.2024, Geldpolitischer Beschluss der Europäischen Zentralbank (Leitzinssatz: 4.5% +/- 0.0).

16.04.2024, Rede zwischen BoC Tiff Macklem und FED Jerome Powell (Wilson Center’s Washington Forum).

18.04.2024, BoJ Exekutivdirektor SHIMIZU Seiichi, Grundsatzrede (ISDA).

26.04.2024, Geldpolitischer Beschluss der Bank of Japan (Leitzinssatz: 0.10% +/- 0.0).

Halbjährlicher Bericht der Bank von Japan durch den Vorsitzenden UEDA Kazuo am 9. April, 2024:

Der halbjährliche Bericht der Bank von Japan bietet Einblicke in die jüngsten wirtschaftlichen und finanziellen Entwicklungen in Japan und skizziert den Ansatz der Bank in Bezug auf die Geldpolitik. Die japanische Wirtschaft befindet sich auf einem moderaten Erholungspfad, wobei die Unternehmensgewinne und Investitionen im Geschäftsumfeld positiv tendieren. Allerdings gibt es noch einige Schwächen, wie etwa stagnierende Exporte und sporadische Störungen im privaten Konsum. Der Verbraucherpreisindex (CPI) verzeichnet einen jährlichen Anstieg von 2,5 bis 3,0 Prozent, der durch die anhaltenden Effekte früherer Kostensteigerungen getrieben wird. Die Bank erwartet, dass sich die zugrunde liegende CPI-Inflation allmählich dem Preisstabilitätsziel von 2 Prozent bis zum Ende des Haushaltsjahres 2024 annähert. Das Finanzsystem bleibt robust, wobei japanische Finanzinstitute eine starke Kapitalbasis beibehalten. Die Bank hat ihren geldpolitischen Rahmen geändert, wobei der Fokus auf dem kurzfristigen Zinssatz liegt, mit einem Zielbereich von 0 bis 0,1 Prozent. Dies zeigt, dass die bisherige quantitative und qualitative Lockerung (QQE) und die Steuerung der Zinskurve ihren Zweck erfüllt haben. Angesichts des aktuellen wirtschaftlichen Ausblicks plant die Bank, die lockeren Finanzbedingungen für die absehbare Zukunft beizubehalten und ihre Politik bei Bedarf anzupassen, um eine nachhaltige und stabile Preisstabilität zu gewährleisten.

Etwas später, am 18. April hielt der BoJ Exekutivdirektor, SHIMIZU Seiichi, eine Grundsatzrede auf der 38. Jahreshauptversammlung der ‚International Swaps and Derivatives Association‘ (ISDA). Er referierte hier über die LIBOR Reformen. Eine Zusammenfassung soll an dieser Stelle angebracht sein, um die Wichtigkeit dieser Finanzmarkt-Reform zu unterstreichen:

Der Übergang vom LIBOR, dem einst dominierenden Zinsreferenzsatz, ist eine wichtige Initiative zur Verbesserung der Integrität und Robustheit der Finanzmärkte. Nach weit verbreiteten Bedenken hinsichtlich der Glaubwürdigkeit des LIBOR aufgrund von Manipulationsversuchen unternahmen internationale Gremien umfassende Anstrengungen, um alternative Referenzsätze zu identifizieren und die Umstellung zu ermöglichen. 2013 veröffentlichte die International Organization of Securities Commissions (IOSCO) einen Bericht, der die gewünschten Eigenschaften von Zinsreferenzsätzen darlegte und eine glaubwürdige Governance sowie eine transaktionsbasierte Berechnung gegenüber Expertenschätzungen empfahl. Der Financial Stability Board (FSB) folgte mit einem Bericht von 2014, der die Reform bestehender IBORs und die Einführung von risikofreien Zinsen befürwortete und einen Mehrfachansatz empfahl, um Flexibilität für verschiedene Gerichtsbarkeiten und Transaktionstypen zu ermöglichen.

Japans LIBOR-Reform entspricht diesen internationalen Empfehlungen und umfasst die Umstellung auf Referenzsätze wie den Tokyo Overnight Average Rate (TONA), den reformierten Tokyo Interbank Offered Rate (TIBOR) und den Tokyo Term Risk Free Rate (TORF). Diese Veränderung hat erhebliche Auswirkungen auf Zinsswaps, da die meisten bestehenden Verträge nun TONA als Referenz verwenden. Der reibungslose Übergang vom LIBOR, der weitgehend mit der Einstellung der Veröffentlichung des USD-LIBOR im Juni abgeschlossen war, wurde durch die Zusammenarbeit zwischen Finanzinstituten, Marktteilnehmern und nationalen Arbeitsgruppen erleichtert. Diese Gruppen, unterstützt von der Bank of Japan und internationalen Organisationen wie der ISDA, spielten eine entscheidende Rolle bei der Koordinierung der Umstellungsstrategien und der Gewährleistung der Einhaltung der IOSCO-Prinzipien. Trotz des Erfolgs bei der Umstellung vom LIBOR bleiben einige Herausforderungen bestehen, insbesondere die nachhaltige Nutzung alternativer Referenzsätze und die fortlaufende Umstellung vom Euroyen TIBOR, dessen Veröffentlichung am Ende des Jahres eingestellt wird.

Zum 5. April wurde der Abstand zwischen Lohnwachstum und Arbeitslosenzahlen deutlich negativer. Der Wert liegt jetzt bei 1,08, verglichen mit 1,31 im Vorjahr, was eine Verschlechterung des Arbeitsmarktes um 23% bedeutet. Das bedeutet, wenn die Löhne sinken, während die Arbeitslosigkeit steigt, bewegt sich der Arbeitsmarkt in die falsche Richtung.

Am 10. April lag die US-Kerninflation, saisonal angepasst, bei 312,23 Punkten. Wenn man das Lohnwachstum mit der Inflation vergleicht, erhält man ein Gefühl dafür, was „reale“ Inflation für die Verbraucher bedeutet. Um zu berechnen, wie sich Ihre Löhne seit 1982-1984 verändert haben, wird diese Periode auf 100 Punkte festgelegt. Wenn Ihr Einkommen damals €17.500 war und es jetzt €35.000 beträgt, würden Sie (100 x 35.000) / 17.500 = 200 rechnen. Vergleicht man Ihr Lohnwachstum mit der Inflation, bedeutet das jedoch, dass Ihr Einkommen in realen Zahlen um 36% gesunken ist.

Die Protokolle der Sitzung des Federal Open Market Committee vom 19.-20. März gaben Aufschluss darüber, warum der Leitzins am 10. April festgelegt wurde. Die Rede des Vorsitzenden der Federal Reserve, Jerome Powell, am Wilson Center am 16. April war besonders interessant, weil erwartet wurde, dass er sich zu den jüngsten US-Kerninflationsdaten äußern würde.

Insgesamt erwartet der Markt nun keine schnelle Zinssenkung mehr, und eine längere Phase hoher Zinssätze scheint wahrscheinlicher zu sein. Zusammen mit der Entscheidung der japanischen Zentralbank, den Leitzins bei 0,1% zu belassen, fiel der Yen am 26. April um -1,72% gegenüber dem US-Dollar auf 158,3.

Auch die Europäische Zentralbank veröffentlichte am 11. April, ihren Leitzins bei 4,5% zu belassen.

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

LG Ben

Goody Traders

04/05/2024, US unemployment figures (March 2024 m/m: 3.8% -0.1%).

04/05/2024, US unemployment figures (March 2024 m/m: 3.8% -0.1%).

04/05/2024, US wage development (hourly wage average y/y: 4.1% -0.2%).

04/09/2024, BoJ Chairman Ueda, statement to the Finance Committee of the ‚House of Councilors‘.

04/10/2024, US Consumer Price Index (CPI, s.a.) (1982-1984=100, 312.23 points).

04/10/2024, Monetary policy decision of the Bank of Canada (key interest rate: 5.00% +/- 0.0).

04/10/2024, US FED Minutes of the Federal Open Market Committee (March 19-20, 2024).

04/11/2024, Monetary policy decision of the European Central Bank (key interest rate: 4.5% +/- 0.0).

04/16/2024, Speech between BoC Tiff Macklem and FED Jerome Powell (Wilson Center’s Washington Forum).

04/18/2024, BoJ Executive Director SHIMIZU Seiichi, keynote speech (ISDA).

04/26/2024, Monetary policy decision of the Bank of Japan (key interest rate: 0.10% +/- 0.0).

Bank of Japan Semi-Annual Report by Chairman UEDA Kazuo on April 9, 2024:

The Bank of Japan’s semiannual report provides insights into recent economic and financial developments in Japan and outlines the Bank’s monetary policy approach. The Japanese economy is on a moderate recovery path, with corporate profits and business investment trending positively. However, some weaknesses remain, such as flat exports and sporadic disruptions in private consumption. The consumer price index (CPI) has seen a year-on-year increase of 2.5-3.0 percent, driven by the lasting effects of previous cost increases. The Bank anticipates that the underlying CPI inflation will gradually approach the 2 percent price stability target by the end of the fiscal 2024 projection period. The financial system remains robust, with Japanese financial institutions maintaining strong capital bases. The Bank has shifted its monetary policy framework, focusing on the short-term interest rate with a target range of 0 to 0.1 percent, indicating that the previous Quantitative and Qualitative Monetary Easing (QQE) and Yield Curve Control have served their purpose. Given the current economic outlook, the Bank plans to maintain accommodative financial conditions for the foreseeable future, adapting its policy as required to ensure sustainable and stable price stability.

Later, on April 18, BoJ Executive Director, SHIMIZU Seiichi, delivered a keynote address at the 38th Annual General Meeting of the International Swaps and Derivatives Association (ISDA). He spoke here about the LIBOR reforms. A summary is appropriate at this point to underline the importance of this financial market reform:

The transition from LIBOR, the once-dominant interest rate benchmark, is a key initiative in improving the integrity and robustness of financial markets. After widespread concerns regarding LIBOR’s credibility due to attempted manipulation, international bodies undertook a comprehensive effort to identify and transition to alternative benchmarks. In 2013, the International Organization of Securities Commissions (IOSCO) released a report outlining the desired features of interest rate benchmarks, recommending credible governance and a transaction-based calculation approach over expert judgment. The Financial Stability Board (FSB) followed with a 2014 report advocating for the reform of existing IBORs and the adoption of risk-free rates, suggesting a multiple-rate approach to allow flexibility across different jurisdictions and transaction types.

Japan’s LIBOR reform aligns with these international recommendations, transitioning to benchmarks such as the Tokyo Overnight Average Rate (TONA), the reformed Tokyo Interbank Offered Rate (TIBOR), and the Tokyo Term Risk Free Rate (TORF). This shift has significantly impacted interest rate swaps, with most existing contracts now referencing TONA. The smooth transition from LIBOR, largely completed with the cessation of USD LIBOR publication in June, was facilitated by collaborative efforts among financial institutions, market participants, and national working groups. These groups, supported by the Bank of Japan and international bodies like ISDA, played a pivotal role in coordinating transition strategies and ensuring compliance with IOSCO’s principles. Despite the success in transitioning away from LIBOR, outstanding challenges remain, particularly the sustainable usage of alternative benchmarks and the ongoing transition from Euroyen TIBOR, which is set to cease publication at the end of the year.

As of April 5th, the gap between wage growth and unemployment figures became much more negative. Right now, it’s at 1.08, compared to 1.31 a year ago, indicating a 23% decline in the labor market’s health. This means that if wages drop while unemployment rises, the job market is heading in the wrong direction.

On April 10th, the US core inflation, adjusted for seasonal changes, was at 312.23 points. When you compare wage growth to inflation, you get a sense of what „real“ inflation means for consumers. To calculate how much your wages have changed since 1982-1984, you set that period to 100 points. If your income back then was €17,500 and it’s now €35,000, then you’d do (100 x 35,000) / 17,500 = 200. However, if you compare your wage increase to inflation, it means your income has dropped by 36% in real terms.

The minutes from the Federal Open Market Committee’s meeting on March 19-20 revealed why the key interest rate was set on April 10th. Federal Reserve Chair Jerome Powell’s talk at the Wilson Center on April 16th was especially interesting because it was expected he would comment on the recent US core inflation data.

Overall, the market is no longer expecting a quick interest rate cut, and a longer period of high-interest rates seems more likely. Along with Japan’s central bank keeping its key interest rate at 0.1%, the yen dropped 1.72% against the US dollar on April 26th, reaching 158.3.

Finally, the European Central Bank also announced on April 11th that it would keep its key interest rate at 4.5%.

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben

US Unemployment Rate

US Average Hourly Earnings YoY

US Core Inflation Rate

USDJPY Daily

Press conference with Governor Tiff Macklem and Senior Deputy Governor Carolyn Rogers on April 10, 2024

International Monetary Fund and World Bank Meeting

Externe Quellen/Links