I call her „Deniz“

2024-03-08 18:17:38 UTC+1Guten Abend

20.02.2024, RBA-Sitzungsprotokoll (Zinsentscheidung 5.-6. Februar 2024).

20.02.2024, RBA-Sitzungsprotokoll (Zinsentscheidung 5.-6. Februar 2024).

21.02.2024, FOMC-Protokoll (Zinsentscheidung 30.–31. Januar 2024).

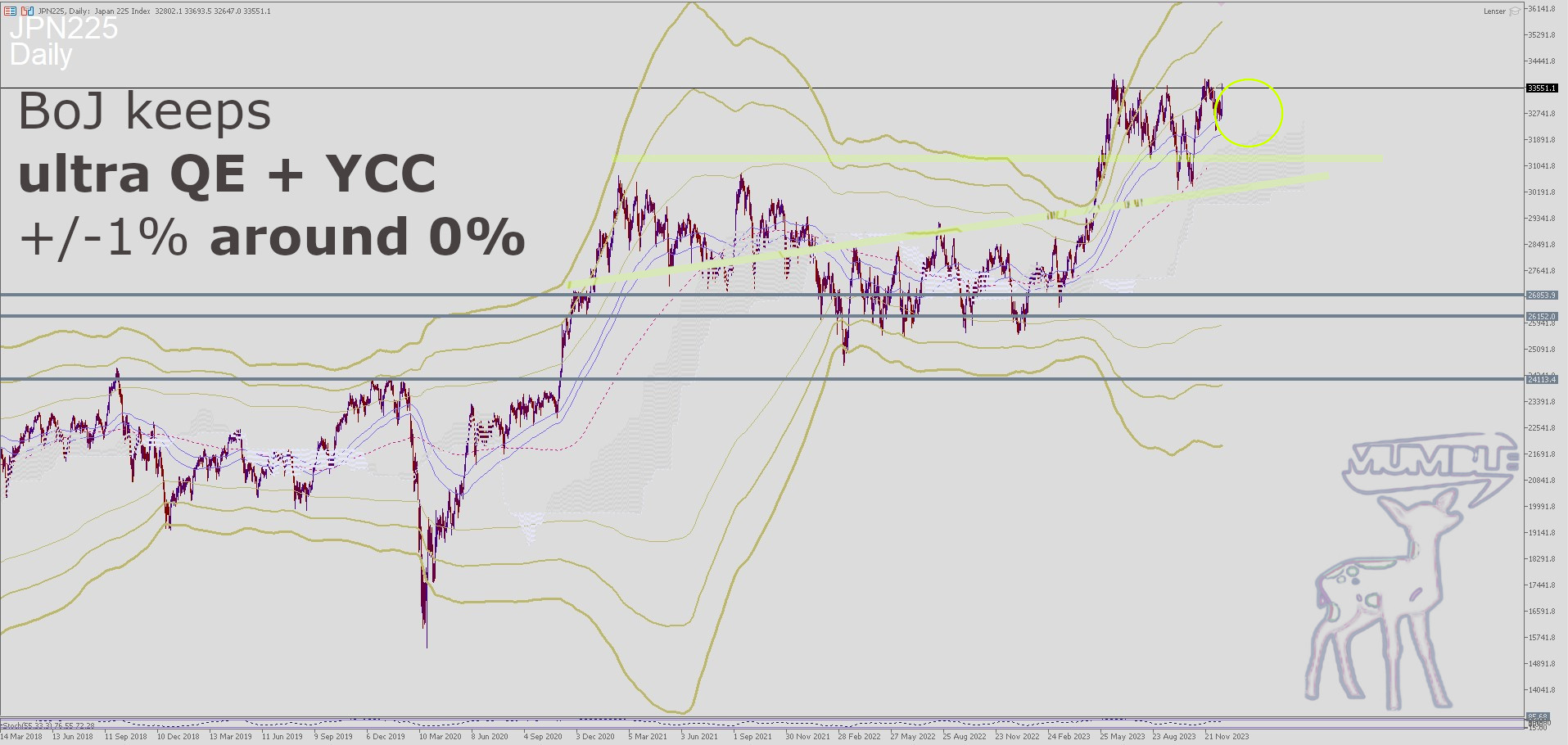

05.03.2024, Ueda Kazuo, Gouverneur der Bank of Japan, Rede.

06.03.2024, Geldpolitischer Beschluss der BoC (Leitzinssatz: 5.0% +/- 0.0).

06.03.2024, Anhörung des Fed-Vorsitzenden Powell vor dem Bankenausschuss des Senats 1/2.

06.03.2024, BoC-Pressekonferenz.

07.03.2024, Geldpolitischer Beschluss der EZB (Leitzinssatz: 4.5% +/- 0.0).

07.03.2024, EZB-Pressekonferenz.

07.03.2024, Anhörung des Fed-Vorsitzenden Powell vor dem Bankenausschuss des Senats 2/2.

Am 20. Februar erhielten wir von der Reserve Bank of Australia die Zusammenfassung des Sitzungsprotokolls vom 5.-6. Februar, mit der Schlussfolgerung, den Leitzins unverändert bei 4,35 Prozent zu belassen.

Mitglieder der RBA stellten globale Inflationstrends, sowie eine gemäßigte Inflation in Australien fest und diskutierten die Auswirkungen verschiedener Faktoren auf das Wirtschaftswachstum, einschließlich der Verschärfung der finanziellen Bedingungen. Die RBA betont die Unsicherheit in den Wirtschaftsaussichten und die Notwendigkeit einer kontinuierlichen Überwachung relevanter Daten.

Die Sitzung der Federal Reserve im Januar 2024 ergab einen etwas besseren Wirtschaftsausblick als im Dezember und korrigierte nachträglich das BIP für 2023 (aufwärts). Der Stab ging aufgrund früherer geldpolitischer Maßnahmen von einem angespannten finanziellen Umfeld in den Jahren 2024 und 2025 aus. Die Arbeitslosenprognosen wurden leicht nach unten korrigiert, und es wurde erwartet, dass sich die Inflation bis 2026 der 2-Prozent-Marke nähert. Die Teilnehmer stellten ein solides Wirtschaftswachstum fest, die Risiken für Inflation und Beschäftigungsziele würden jedoch weiterhin beobachtet werden müssen. Der Ausschuss beließ den Federal Funds Rate bei 5¼ bis 5½ Prozent und signalisierte damit einen vorsichtigen Ansatz bei künftigen Anpassungen. Der Gouverneursrat stimmte einstimmig dafür, die Zinssätze für Reserveguthaben bei 5,4 Prozent zu belassen. Das nächste Treffen ist für den 19.–20. März 2024 geplant.

Gouverneur Ueda Kazuo der Bank of Japan spricht auf dem 18. Asien-Pazifik-Treffen zur Bankenaufsicht und betont die Stabilität des APAC-Finanzsystems im letzten Vierteljahrhundert. Er hebt die asiatische Währungskrise, die darauf folgenden Reformen und Gemeinschaftsinitiativen hervor, die zur Widerstandsfähigkeit beitrugen. Die Rede befasst sich mit den Herausforderungen in einem sich verändernden Umfeld und konzentriert sich dabei auf den globalen Übergang zu einem Hochzinszeitalter, Fortschritte im digitalen Finanzwesen und die Notwendigkeit, die finanziellen Aspekte des Klimawandels anzugehen.

Der Gouverneur der Bank of Canada, Tiff Macklem, gibt zusammen mit der stellvertretenden Gouverneurin Carolyn Rogers am 6. März 2024 die geldpolitische Entscheidung bekannt. Trotz des schwachen Wirtschaftswachstums und der nachlassenden Inflation wird der Leitzins bei 5 % gehalten. Im Einklang mit der Verpflichtung, die Preisstabilität wiederherzustellen, spiegelt die Entscheidung die Notwendigkeit höherer Zinssätze wider, um ihre Wirkung auf die Inflation fortzusetzen. Macklem erörtert die globale und inländische Wirtschaftslage und betont den langsamen und ungleichen Weg zum Inflationsziel von 2 %. Zu den Risiken zählen die globalen Energiepreise, die Transportkosten und die anhaltende Inflation. Der Rat bleibt wachsam und sucht nach Beweisen für ein moderates Lohnwachstum und eine Normalisierung der Preiserhöhungen, bevor er im April über politische Anpassungen nachdenkt. Das Engagement für die Wiederherstellung der Preisstabilität hat im Kampf gegen die hohe Inflation weiterhin höchste Priorität.

Der EZB-Rat der Europäischen Zentralbank gab die Entscheidung zur Beibehaltung der Leitzinsen am 7. März 2024 bekannt. Die Entscheidung wird durch einen weiteren Rückgang der Inflation und eine auf 0,6% revidierte Wirtschaftswachstumsprognose für 2024 beeinflusst. Trotz der Lockerung der zugrunde liegenden Inflationsmaßnahmen bleibt der inländische Preisdruck aufgrund des starken Lohnwachstums bestehen. Der EZB-Rat betont sein Engagement für die Erreichung des Inflationsziels von 2 % und signalisiert seine Entschlossenheit, über einen längeren Zeitraum ausreichend restriktive Zinssätze beizubehalten. Die Bewertung umfasst Überlegungen zu Inflation, Wirtschaftsaktivität und Risiken unter Berücksichtigung geopolitischer Spannungen. Als Reaktion auf die Wirtschaftslage signalisiert die EZB ihre Bereitschaft, im Rahmen ihres Mandats notwendige Anpassungen vorzunehmen. Ziel ist es, die Inflation wieder auf das 2-Prozent-Ziel zu lenken und die wirksame Funktion der geldpolitischen Transmission aufrechtzuerhalten. Diese proaktive Haltung zeigt das Engagement der EZB, Herausforderungen anzugehen und die Stabilität in der breiteren Finanzlandschaft aufrechtzuerhalten.

Insgesamt erwarte ich, dass die Stärke des USD aufgrund der bevorstehenden Zinswende beschränkt bleiben wird. Der Aktienmarkt Peaked und erreichte Höchststände. Ich würde es vorziehen, Goldanlagen zu liquidieren, um bei Kursrückgängen im Technologiesektor (KI) zu kaufen. Seien Sie sich bewusst, dass wir die Wirtschaft erst noch sanft landen müssen, nachdem sich die Renditekurven invertiert haben und der Spread zwischen 10- und 2-jährigen US-Staatsanleihen negativ ausgefallen ist.

Jetzt konservativer, da wahrscheinlich in den kommenden Quartalen eine Preisnormalisierung anrollt.

Jetzt konservativer, da wahrscheinlich in den kommenden Quartalen eine Preisnormalisierung anrollt.

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

LG Ben

Goody Traders

2024-02-20, RBA Meeting Minutes (Interest Rate decision 5-6 February 2024).

2024-02-20, RBA Meeting Minutes (Interest Rate decision 5-6 February 2024).

2024-02-21, FOMC Minutes (January 30–31, 2024).

2024-03-05, Ueda Kazuo Governor of the Bank of Japan.

2024-03-06, BoC Monetary Policy Decision 5% (+/- 0.0%).

2024-03-06, Fed Chair Powell Testimony to the Senate Banking Committee 1/2.

2024-03-06, BoC Press Conference..

2024-03-07, ECB Monetary Policy Decision 4.5% (+/- 0.0%).

2024-03-07, ECB Press Conference.

2024-03-07, Fed Chair Powell Testimony to the Senate Banking Committee 2/2.

On 20th February we got the abstarct form the Reserve Bank of Australia of the 5-6 February meeting minutes, with the conclusion being to leave the cash rate unchanged at 4.35 percent.

Members of the RBA noted global inflationary trends, moderated inflation in Australia, and discussed the impact of various factors on economic growth, including tightening financial conditions. The RBA emphasizes the uncertainty in the economic outlook and the need for ongoing monitoring of relevant data.

The January 2024 Federal Reserve meeting revealed a slightly stronger economic outlook than December’s, with an upward revision in 2023 GDP growth. The staff anticipated a tight financial environment in 2024 and 2025 due to past monetary policy actions. Unemployment projections were revised slightly down, and inflation was expected to approach 2 percent by 2026. Participants noted solid economic expansion, but risks to inflation and employment goals were still monitored. The Committee maintained the federal funds rate at 5¼ to 5½ percent, signaling a cautious approach to future adjustments. The Board of Governors unanimously voted to keep interest rates on reserve balances at 5.4 percent. The next meeting was scheduled for March 19–20, 2024.

Governor Ueda Kazuo of the Bank of Japan addresses the 18th Asia-Pacific High-Level Meeting on Banking Supervision, emphasizing the stability of the APAC financial system over the past quarter-century. He highlights the pivotal Asian currency crisis, subsequent reforms, and collaborative initiatives contributing to resilience. The speech explores challenges amid a changing environment, focusing on the global shift to a high-interest rate era, progress in digital finance, and the imperative to address climate change’s financial aspects.

Bank of Canada Governor Tiff Macklem, along with Senior Deputy Governor Carolyn Rogers, announces the monetary policy decision on March 6, 2024. Despite weak economic growth and easing inflation, the policy interest rate is maintained at 5%, aligning with the commitment to restore price stability. The decision reflects the need for higher rates to continue their impact on inflation. Macklem discusses global and domestic economic conditions, emphasizing the slow and uneven path towards the 2% inflation target. Risks include global energy prices, transportation costs, and the persistence of inflation. The council remains vigilant, seeking evidence of moderating wage growth and normalizing price increases before considering policy adjustments in April. The commitment to restoring price stability remains a top priority in the fight against high inflation.

The European Central Bank’s Governing Council announces the decision to maintain unchanged key interest rates on March 7, 2024. The decision is influenced by a further decline in inflation and a revised economic growth projection for 2024 to 0.6%. Despite easing underlying inflation measures, domestic price pressures persist due to strong wage growth. The Governing Council emphasizes its commitment to achieving the 2% inflation target and signals a determination to maintain sufficiently restrictive interest rates for an extended period. The assessment includes considerations of inflation, economic activity, and risks, with attention to geopolitical tensions. In response to economic conditions, the ECB signals its readiness to make necessary adjustments within its mandate. The aim is to steer inflation back to the 2% target and uphold the effective functioning of monetary policy transmission. This proactive stance demonstrates the ECB’s commitment to addressing challenges and maintaining stability in the broader financial landscape.

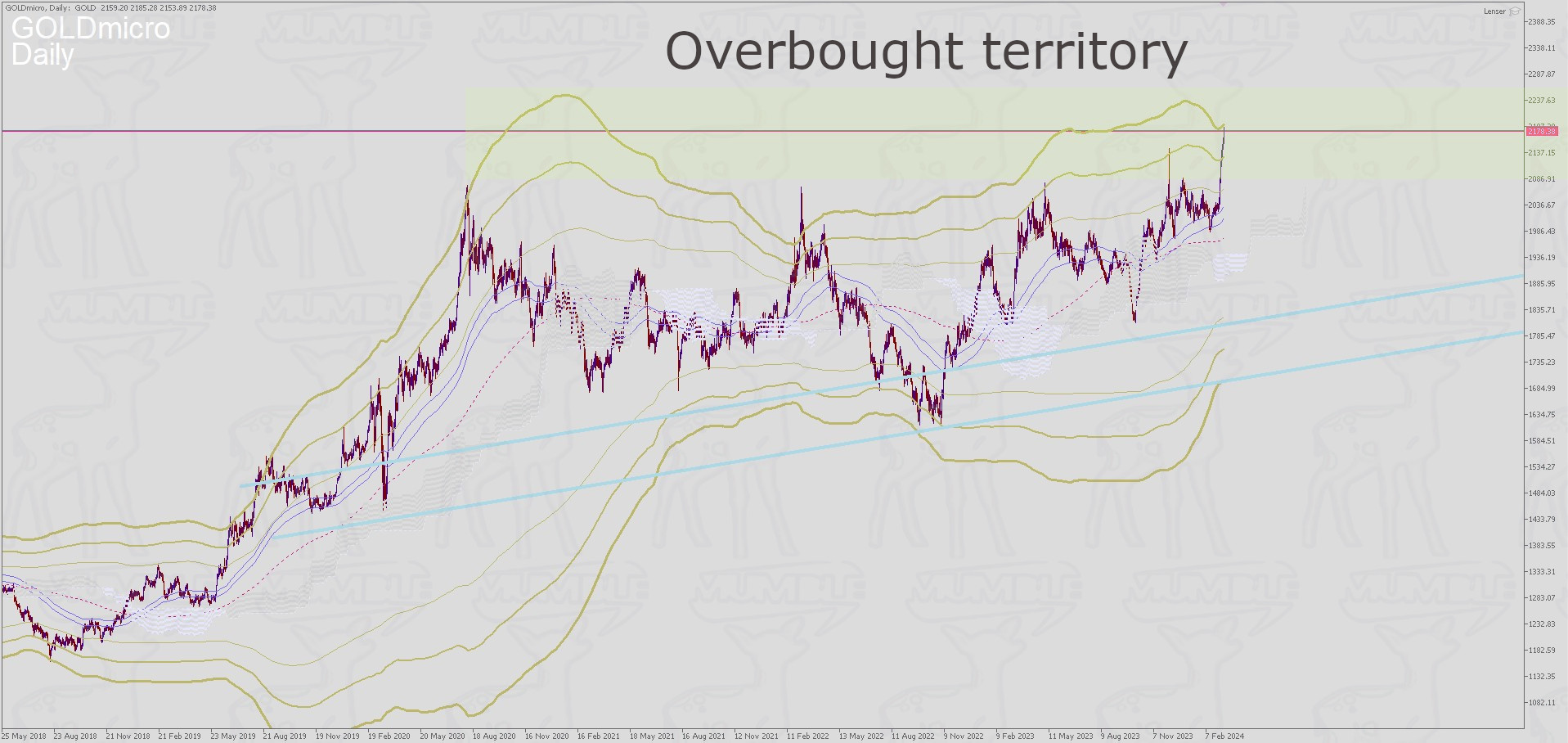

Overall, I expect the USD being limited to the upside, due the shift in interest rates ahead. The stock market peaked out levels in mind, i’d prefer to liquidate Gold assets in order to buy dips in Tech (AI). Be aware, we’ll yet have to land the economy, after the yield curves being inverted and 10yr-2yr US-Gov-Bond spread seen negative.

At some point in the coming quarters, we’ll see a price normalization.

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben

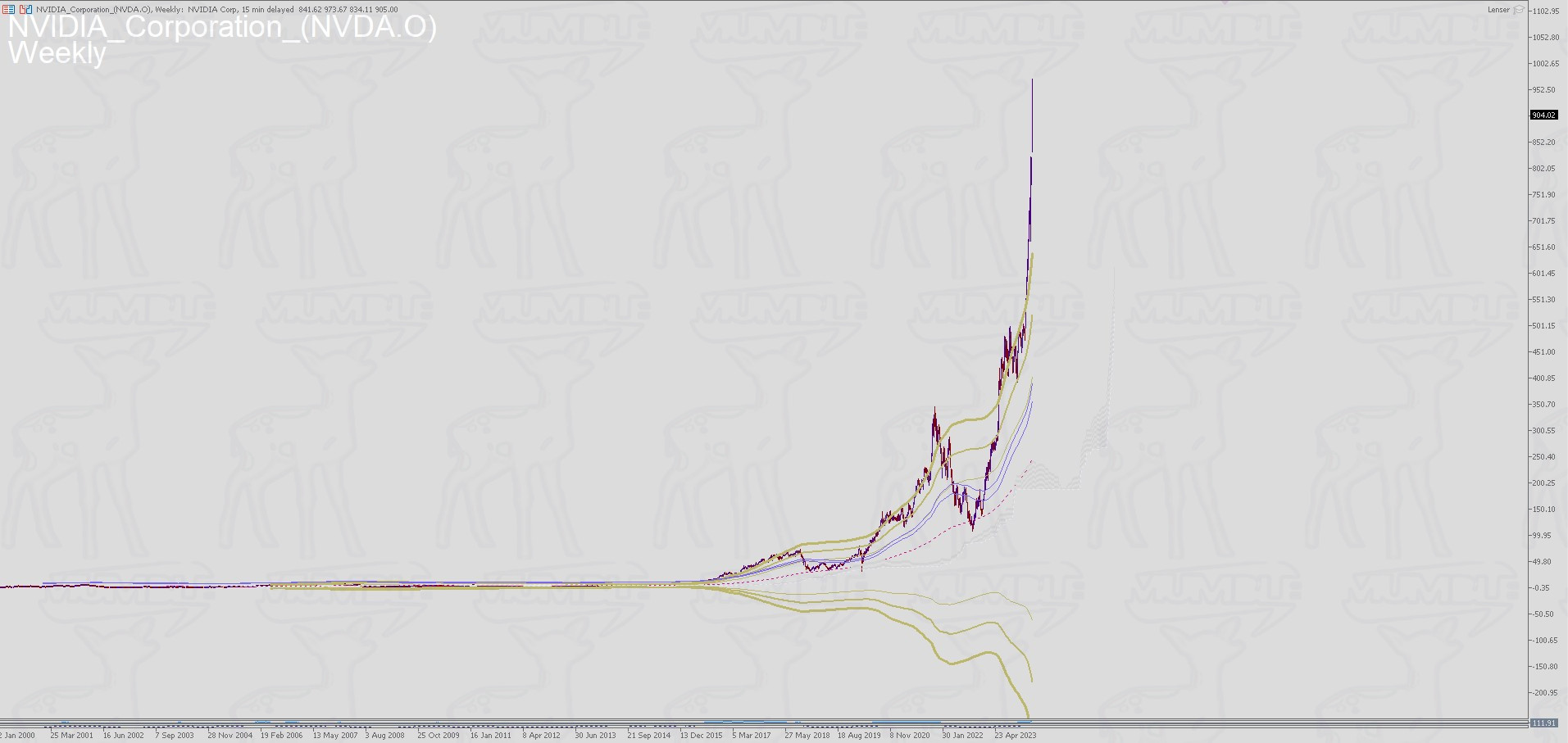

NVIDIA Weekly| so far,…

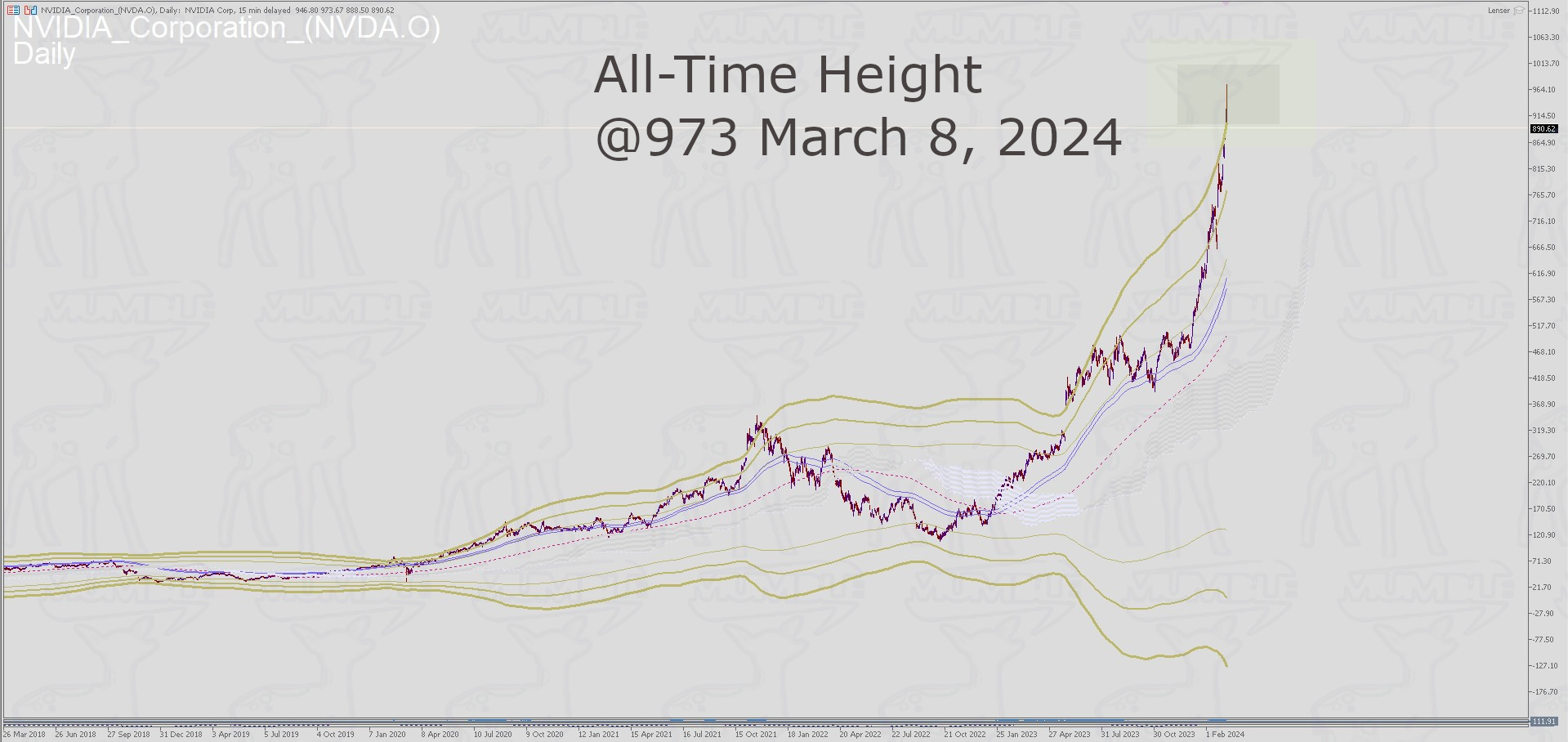

NVIDIA Daily| …, so good!

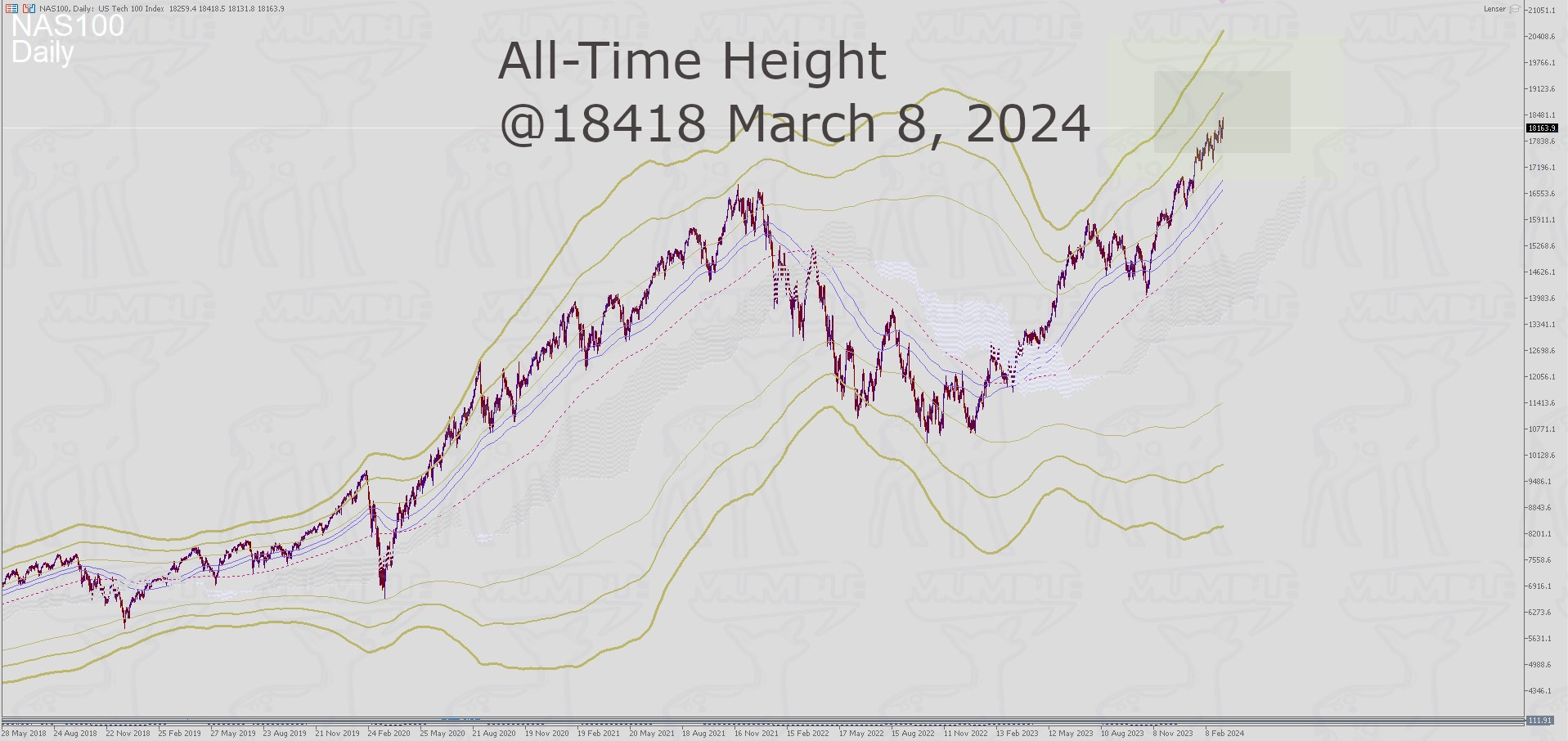

NASDAQ Daily| Sky is a Limit

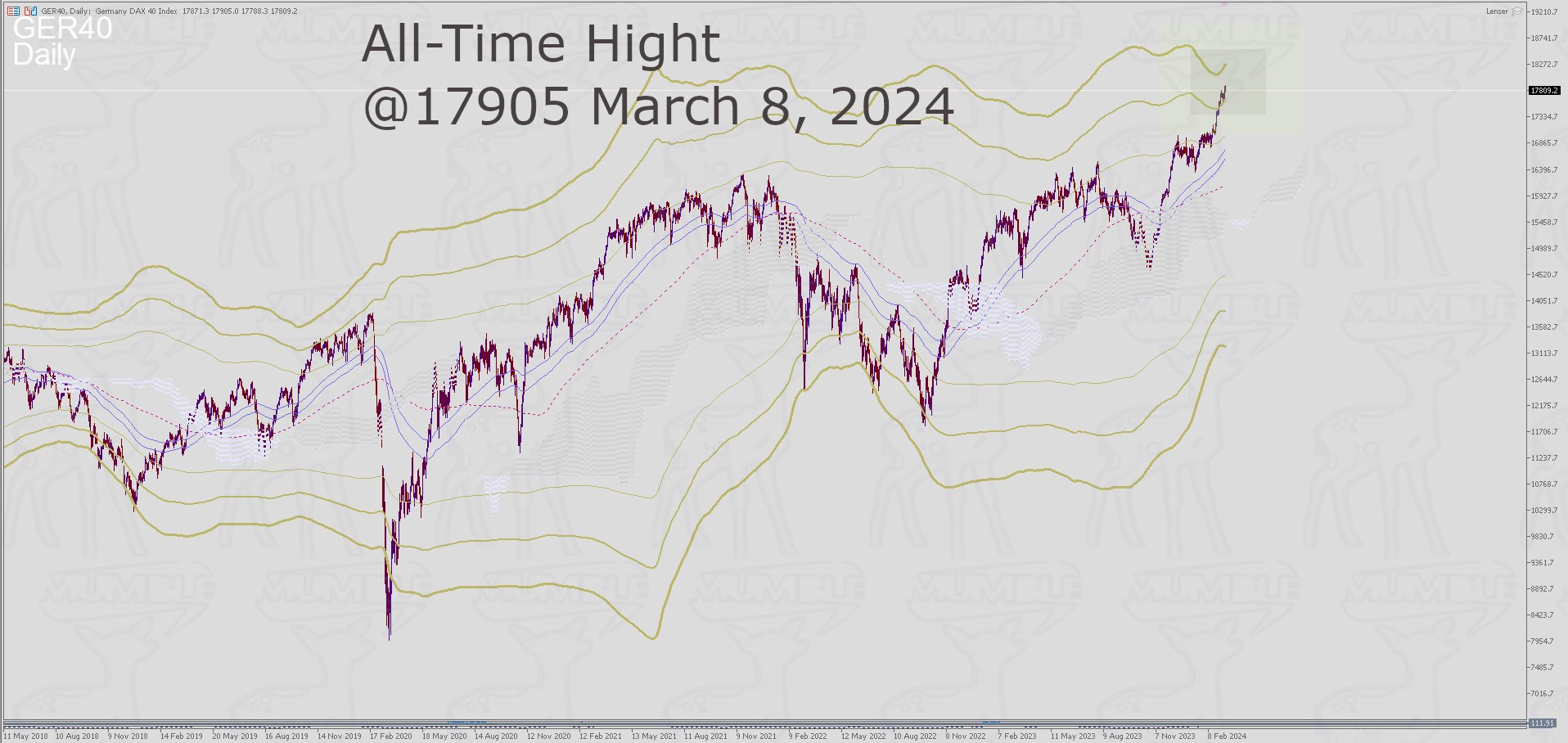

DAX40 Daily | German Wunderkind

GOLD Daily | Best since 4500BC

USDX Daily | Upper Limited ~ IR swingpoint

Externe Quellen/Links