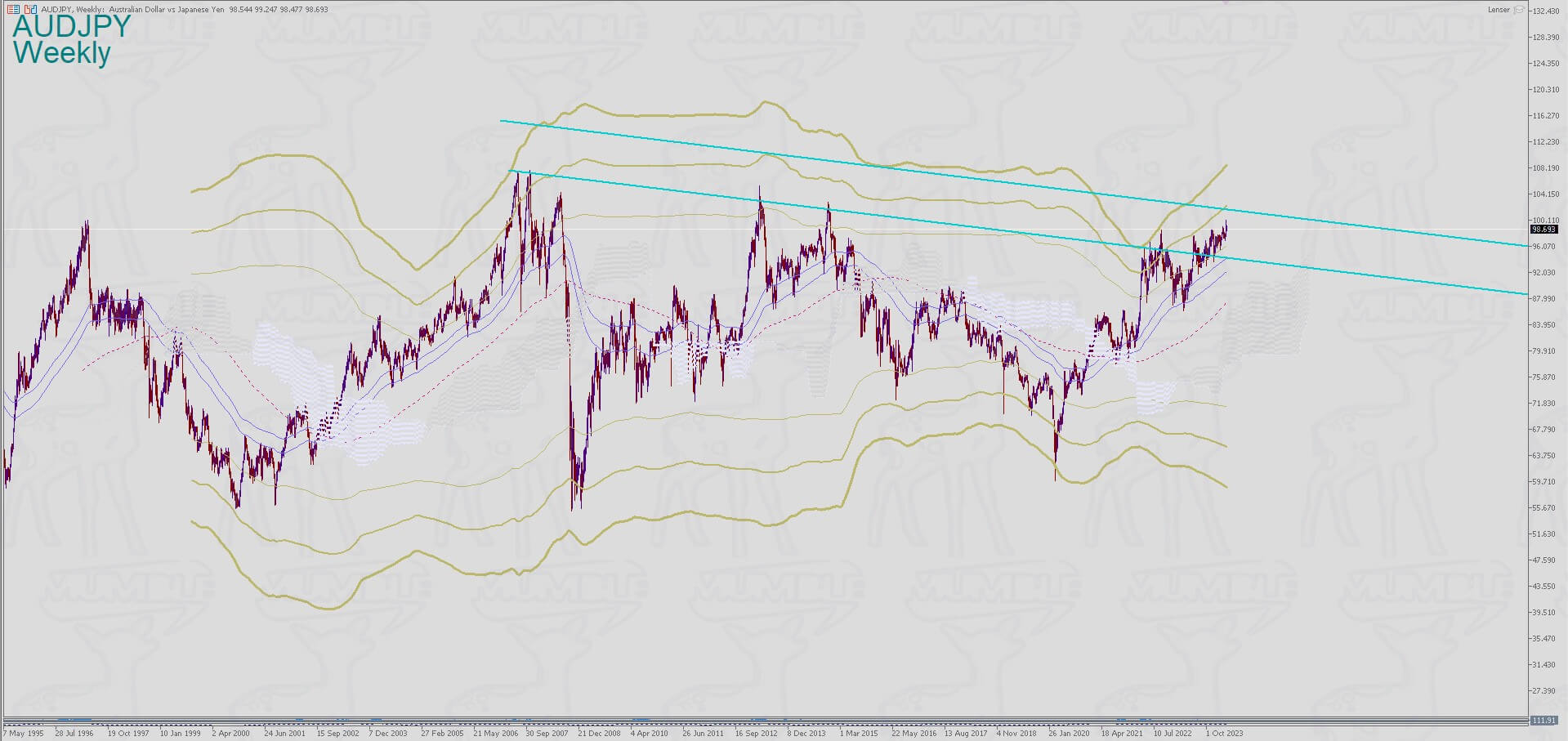

Line in sand for USDJPY

2024-05-11 15:35:39 UTC+1Guten Tag

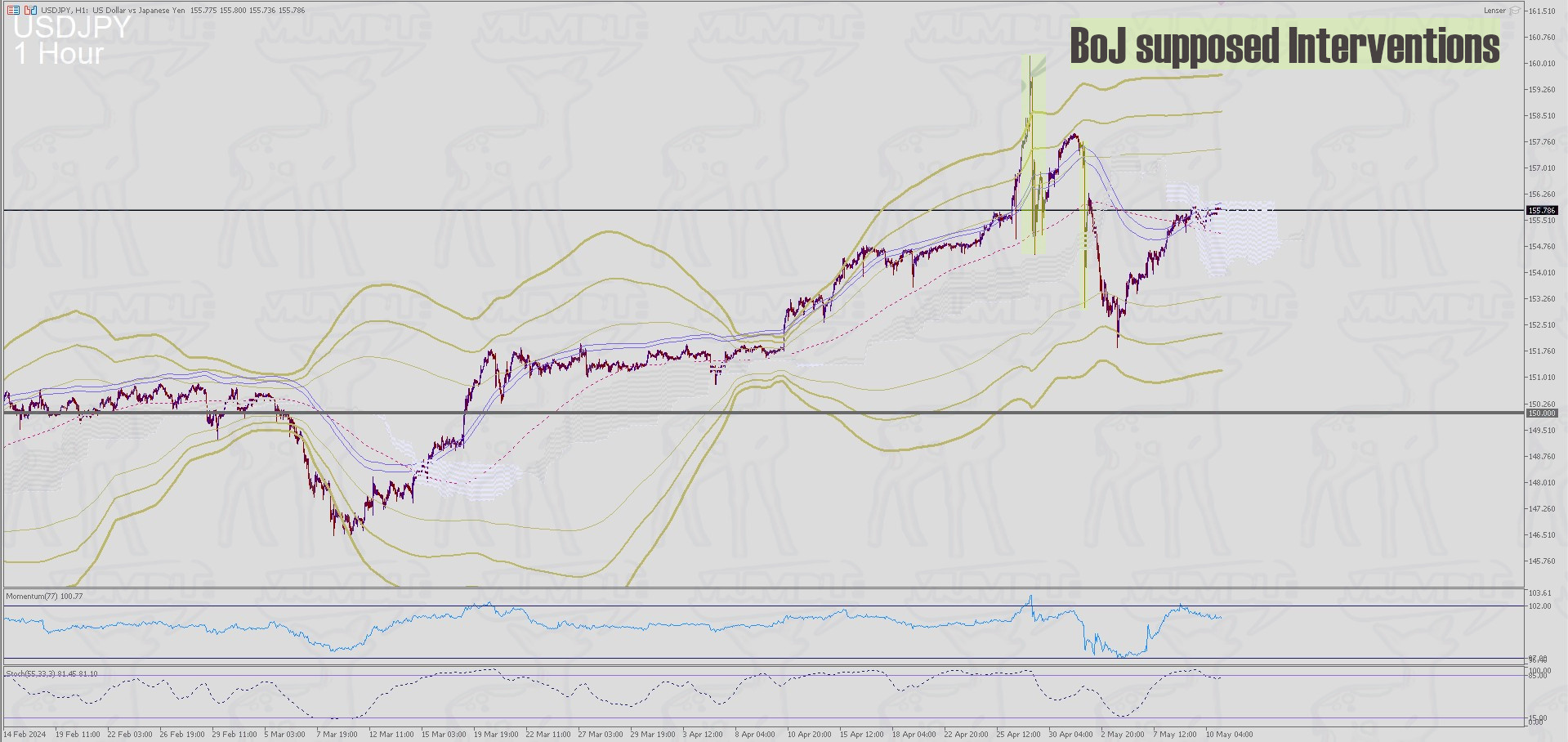

29.04.2024, BoJ FX-Intervention 1/2 (4-5AM UTC).

29.04.2024, BoJ FX-Intervention 1/2 (4-5AM UTC).

01.05.2024, Geldpolitischer Beschluss der FED (Leitzinssatz: 5.50% +/- 0.0).

01.05.2024, BoJ FX-Intervention 2/2 (20-21PM UTC).

07.05.2024, Geldpolitischer Beschluss der RBA (Leitzinssatz: 4.35% +/- 0.0).

09.05.2024, Geldpolitischer Beschluss der BoE (Leitzinssatz: 5.25% +/- 0.0).

Die von der Bank of Japan veröffentlichten Geldmarktdaten deuten darauf hin, dass die Regierung am Devisenmarkt interveniert hat, als der Yen gegenüber dem US-Dollar eine deutliche Kehrtwende erlebte. Die Bank of Japan schätzt, dass am 1. Mai aufgrund von Transaktionen mit dem Regierungssektor ein Liquiditätsabfluss von 7,56 Billionen Yen zu verzeichnen sein wird. Marktteilnehmer vermuten Devisenmarktinterventionen, wie durch unerwartete Transaktionen in Höhe von etwa 5,5 Billionen Yen angezeigt. Das Finanzministerium hat Interventionen zwar nicht bestätigt, äußerte jedoch Bedenken hinsichtlich scharfer Schwankungen der Wechselkurse. Der jüngste Rückgang des Yen löste Spekulationen über weitere Interventionen und deren Auswirkungen auf die japanische Wirtschaft und Geldpolitik aus.

Bank of Japan-Direktoriumsmitglieder wurden in ihrer April-Sitzung überwiegend hawkish, wobei viele eine schrittweise Zinserhöhung forderten, um einer möglichen Inflation vorzubeugen. Einige Mitglieder sahen die Möglichkeit einer schnelleren als erwarteten Zinserhöhung aufgrund der Aussichten, dass die Inflation nachhaltig bei oder sogar über dem BOJ-Ziel von 2% bleiben könnte. Die Diskussion unterstreicht die jüngsten Äußerungen von BOJ-Gouverneur Kazuo Ueda, die die Möglichkeit mehrerer Zinserhöhungen signalisieren. Die hawkishen Signale der BOJ haben jedoch den Yen nicht gestützt, da die Märkte weiterhin auf zurückgehende Aussichten für kurzfristige Zinssenkungen in den USA konzentriert sind. Viele Marktteilnehmer erwarten, dass die BOJ später in diesem Jahr die Zinsen erhöhen wird, obwohl sie uneins darüber sind, wie schnell die Kosten danach steigen könnten. Andere Meinungen forderten auch, dass die BOJ irgendwann ihre Absicht bekunden sollte, ihre riesigen Anleihekäufe zu reduzieren und ihre Bilanz zu verkleinern.

Überblick über die Erklärung des Federal Reserve FOMC:

Die jüngste Erklärung des Federal Open Market Committee (FOMC) zeigt eine robuste wirtschaftliche Landschaft, gekennzeichnet durch starke Beschäftigungszuwächse und eine anhaltend niedrige Arbeitslosenquote. Trotz einiger Entspannung bleibt die Inflation erhöht, was eine bedeutende Sorge darstellt. Die Kernziele des Ausschusses sind die Erreichung der maximalen Beschäftigung und die Stabilisierung der Inflation auf einem langfristigen Niveau von 2 Prozent, wobei in letzter Zeit eine bessere Balance bei den Risiken festzustellen ist. Die Aufrechterhaltung des Zielbereichs für den Federal-Leitzinssatz von 5-1/4 bis 5-1/2 Prozent unterstreicht das Engagement des Ausschusses zur Unterstützung dieser Ziele. In Zukunft wird der Ausschuss eingehend die eingehenden Daten überwachen und vorläufig auf eine Reduzierung des Zielbereichs verzichten, bis nachhaltige Fortschritte in Richtung seines Inflationsziels gewährleistet sind. Zusätzlich plant er, seine Bestände an Schatzpapieren und Agenturschulden weiter zu reduzieren, während er gleichzeitig auf aufkommende Risiken achtet, die seine geldpolitischen Entscheidungen beeinflussen könnten.

Reserve Bank of Australia:

Bei seinem Treffen beschloss das Reserve Bank Board, den Zielwert für den Leitzins und den Zinssatz unverändert zu lassen. Die Inflation bleibt hoch und nimmt langsamer ab als erwartet, insbesondere bei Dienstleistungen. Trotz höherer Zinssätze besteht weiterhin eine Übernachfrage, wobei die Arbeitsmarktbedingungen eng bleiben und das Lohnwachstum über einem nachhaltigen Niveau liegt. Der wirtschaftliche Ausblick bleibt unsicher, und die Rückkehr der Inflation zum Zielwert wird nur allmählich erwartet. Die Beharrlichkeit der Dienstleistungspreisinflation ist eine zentrale Unsicherheit, die stärkere Arbeitsmarktbedingungen widerspiegelt. Das Board bleibt entschlossen, die Inflation auf den Zielwert zurückzuführen, erkennt jedoch die Unsicherheit hinsichtlich der Wirksamkeit der Geldpolitik an.

Bank of England, Monetary Policy Summary, Mai 2024:

Das Geldpolitische Komitee der Bank of England beschloss, den Bankenzinssatz auf 5,25% zu belassen, wobei sich 7 Mitglieder dafür und zwei dagegen aussprachen. Das Komitee überprüfte die globalen wirtschaftlichen Bedingungen und diskutierte divergierende Trends bei Inflation und Geldpolitik in verschiedenen Regionen. Das Wachstum des britischen BIP wird voraussichtlich moderat ausfallen, wobei die Inflationsprognosen mittelfristig eine Rückkehr zum Ziel von 2% nahelegen. Trotz Bedenken hinsichtlich der Inflationspersistenz bleibt das MPC dem Ziel der Preisstabilität gemäß seinem Mandat verpflichtet.

Minutes der Sitzung des Geldpolitischen Komitees vom 8. Mai 2024:

Das MPC beriet über globale Wirtschaftstrends, insbesondere die Inflationsdynamik in den USA und im Euroraum. Veränderungen der Markterwartungen hinsichtlich der US-Geldpolitik beeinflussten die Zinsprognosen weltweit. In Großbritannien erwarten Marktteilnehmer eine Abwärtskorrektur des Bankenzinssatzes. Inländische Wirtschaftsindikatoren deuten auf eine gemischte Aussicht für den privaten Verbrauch und das Lohnwachstum hin, wobei Unsicherheiten hinsichtlich der Daten aus der Arbeitskräfteerhebung bestehen. Das Komitee betonte die Bedeutung der Berücksichtigung verschiedener Indikatoren für die Inflationspersistenz angesichts sich ändernder wirtschaftlicher Bedingungen.

Das Geldpolitische Komitee (MPC) hielt den Bankenzinssatz auf 5,25%, um das Inflationsziel von 2% zu erreichen. Die Indikatoren für die Inflationspersistenz entwickelten sich im Wesentlichen wie erwartet, wenn auch etwas stärker als angenommen. Die Dienstleistungsverbraucherpreisinflation ging zurück, blieb aber mit 6,0% im März hoch. Der Arbeitsmarkt lockerte sich weiter, blieb aber relativ eng, wobei das jährliche Lohnwachstum im privaten Sektor im Februar auf 6,0% zurückging. Trotz unterschiedlicher Ansichten unter den Mitgliedern bevorzugte die Mehrheit die Beibehaltung des Bankenzinssatzes, während zwei Mitglieder eine Senkung auf 5% bevorzugten. Das MPC ist bereit, die Politik basierend auf wirtschaftlichen Daten anzupassen, um die Inflation nachhaltig auf das Ziel von 2% zurückzuführen.

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

LG Ben&Deniz

Goody Traders

04/29/2024, BoJ FX intervention 1/2 (4-5AM UTC).

04/29/2024, BoJ FX intervention 1/2 (4-5AM UTC).

05/01/2024, monetary policy decision of the FED (key interest rate: 5.50% +/- 0.0).

05/01/2024, BoJ FX intervention 2/2 (8-9PM UTC).

05/07/2024, RBA monetary policy decision (key interest rate: 4.35% +/- 0.0).

05/09/2024, BoE monetary policy decision (key interest rate: 5.25% +/- 0.0).

Money market data released by the Bank of Japan indicates government intervention in the currency market, as the yen experienced a significant turnaround against the U.S. dollar. The Bank of Japan estimates a liquidity drain of 7.56 trillion yen on May 1, attributed to transactions with the government sector. Market players suspect currency market intervention, as indicated by unanticipated transactions totaling approximately 5.5 trillion yen. The Ministry of Finance has not confirmed intervention but expressed concerns about sharp swings in exchange rates. The yen’s recent decline prompted speculation about further intervention and its impact on Japan’s economy and monetary policy.

Bank of Japan board members leaned heavily hawkish at their April meeting, advocating for a gradual increase in interest rates to mitigate the risks of an inflation overshoot. Some members suggested the possibility of a quicker pace of rate hikes if inflation continues to exceed the 2% target, especially with a weakening yen. Despite these signals, the yen failed to strengthen as markets remained focused on diminishing prospects of U.S. interest rate cuts. The summary also highlighted calls for the eventual reduction of the BOJ’s bond purchases and the shrinking of its balance sheet.

Federal Reserve FOMC Statement Overview:

The latest statement from the Federal Open Market Committee (FOMC) reveals a robust economic landscape, characterized by strong job gains and a sustained low unemployment rate. Despite some easing, inflation remains elevated, posing a significant concern. The Committee’s core objectives are to achieve maximum employment and stabilize inflation at a 2 percent rate over the long term, with risks towards better balance in recent times. Maintaining the federal funds rate at 5-1/4 to 5-1/2 percent underscores the Committee’s commitment to supporting these goals. Looking ahead, the Committee will closely monitor incoming data, refraining from reducing the target range until sustainable progress towards its inflation target is ensured. Additionally, it plans to continue reducing its holdings of Treasury securities and agency debt while remaining vigilant for any emerging risks that could influence its policy decisions.

Reserve Bank of Australia:

At its meeting, the Reserve Bank Board decided to keep the cash rate target and interest rate unchanged. Inflation remains high and is declining slower than expected, particularly in services. Despite higher interest rates, excess demand persists, with tight labor market conditions and wage growth still above sustainable levels. The economic outlook remains uncertain, with inflation expected to return to target only gradually. The persistence of services inflation is a key uncertainty, reflecting stronger labor market conditions. The Board remains committed to returning inflation to target but acknowledges the uncertainty surrounding monetary policy’s effectiveness.

Bank of England Monetary Policy Summary, May 2024:

The Bank of England’s Monetary Policy Committee (MPC) opted to maintain Bank Rate at 5.25%, with 7 members voting for and 2 against. The Committee reviewed global economic conditions, discussing divergent trends in inflation and monetary policies across regions. UK GDP growth is expected to be modest, with inflation projections suggesting a return to the 2% target in the medium term. Despite concerns about inflation persistence, the MPC remains committed to ensuring price stability in line with its mandate.

Minutes of the Monetary Policy Committee meeting ending on 8 May 2024:

The MPC deliberated on global economic trends, particularly inflation dynamics in the US and euro area. Shifts in market expectations for US monetary policy influenced interest rate forecasts globally. In the UK, market participants anticipate a downward adjustment in Bank Rate. Domestic economic indicators suggest a mixed outlook for consumer spending and wage growth, with uncertainties surrounding the Labour Force Survey data. The Committee emphasized the importance of considering various indicators of inflation persistence amid evolving economic conditions.

The Monetary Policy Committee (MPC) maintained Bank Rate at 5.25% to meet the 2% inflation target. Inflation indicators evolved broadly as expected, though slightly stronger than anticipated. Services consumer price inflation decreased but remained elevated at 6.0% in March. The labour market continued to loosen but remained relatively tight, with annual private sector wage growth declining to 6.0% in February. Despite differing views among members, the majority favored maintaining Bank Rate, while two members preferred a reduction to 5%. The MPC remains prepared to adjust policy based on economic data to sustainably return inflation to the 2% target.

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben&Deniz

USDJPY H1-Chart

Externe Quellen/Links

Nothing is more magnificent then the intensities of colors that dominate this garden for two weeks in spring and perhaps three weeks in autumn. The colors seem to radiant above the trees, almost as if generated by the God I do not believe in. [Michael Steinhardt, No Bull]

Nothing is more magnificent then the intensities of colors that dominate this garden for two weeks in spring and perhaps three weeks in autumn. The colors seem to radiant above the trees, almost as if generated by the God I do not believe in. [Michael Steinhardt, No Bull]