Ueda, building blocks for the concrete base

2024-03-27 19:52:01 UTC+1Guten Abend

19.03.2024, Geldpolitischer Beschluss der Bank of Japan (Leitzinssatz: 0.0% +0.1%).

19.03.2024, Geldpolitischer Beschluss der Bank of Japan (Leitzinssatz: 0.0% +0.1%).

19.03.2024, Geldpolitischer Beschluss der Reserve Bank of Australia (Leitzinssatz: 4.35% +/- 0.0).

20.03.2024, Geldpolitischer Beschluss der Federal Reserve Bank (Leitzinssatz: 5.5% +/- 0.0).

21.03.2024, Geldpolitischer Beschluss der Schweizer Nationalbank (Leitzinssatz: 1.5% -0.25).

21.03.2024, Geldpolitischer Beschluss der Bank of England (Leitzinssatz: 5.25% +/- 0.0).

Die Bank of Japan geht davon aus, dass das 2%-Preisstabilitätsziel bis Ende Januar 2024 nachhaltig erreicht wird. Die quantitative und qualitative geldpolitische Lockerung der Bank mit der Renditekurvenkontrolle und der Negativzinspolitik haben sich als wirksam erwiesen. Der kurzfristige Zinssatz bleibt das wichtigste Instrument der Geldpolitik, da er darauf abzielt, das 2 %-Ziel stabil zu erreichen.

Zu den Marktoperationsentscheidungen gehört es, den unbesicherten Tagesgeldsatz bis zum 21. März 2024 bei etwa 0 bis 0,1 Prozent zu halten und weiterhin japanische Staatsanleihen zu kaufen. Die Bank plant, den Kauf von ETFs, J-REITs, CP und Unternehmensanleihen schrittweise innerhalb eines Jahres einzustellen und Kredite zu 0,1 % anzubieten, gebunden an Kreditsalden der Kreditgeber.

Die moderate wirtschaftliche Erholung Japans wird durch bessere Unternehmensgewinne, einen angespannten Arbeitsmarkt und potenzielle Lohnsteigerungen determiniert. Steigende Löhne führten zu einem moderaten Preisanstieg, was auf eine Verstärkung des Lohn-Preis-Zyklus schließen lässt. Im Vorstand gibt es eine abweichende Minderheitsmeinung, die die Beibehaltung negativer Zinssätze zur Unterstützung kleinerer Unternehmen befürwortet.

Unsicherheiten in der Weltwirtschaft, bei den Rohstoffpreisen und im inländischen Lohn-Preis-Verhalten stellen hohe Risiken dar, und eine aufmerksame Überwachung der Finanz- und Devisenmärkte, weder deren Auswirkungen auf die japanische Wirtschaft, ist erforderlich. Dennoch wird erwartet, dass Japans Wirtschaft moderat wächst, mit positiven Ergebnissen aus sich beschleunigenden Einkommens- und Ausgabenzyklen und einem erwarteten CPI-Anstieg über 2 %.

Die Reserve Bank of Australia (RBA) hat das Ziel für den Bargeldzinssatz unverändert bei 4,35 Prozent und den Zinssatz für Guthaben aus Abwicklungsgeschäften bei 4,25 Prozent belassen. Die Inflation verlangsamt sich, bleibt aber weiterhin hoch, mit einer gleichbleibenden jährlichen Teuerungsrate beim Verbraucherpreisindex (CPI) von 3,4 Prozent. Während die Inflation bei Waren nachlässt, moderiert sich jene bei Dienstleistungen, obwohl sie hoch bleibt, langsamer.

Hohe Zinssätze zielen darauf ab, Nachfrage und Angebot in der Wirtschaft auszugleichen, was zu einer allmählichen Lockerung der angespannten Arbeitsmarktlage führt. Es wird erwartet, dass das Lohnwachstum nachlässt und die aktuellen Niveaus im Einklang mit den Inflationszielen stehen, sofern die Produktivität ihr langfristiges Mittel erreicht. Die Auswirkungen der Inflation auf das reale Einkommen tragen zu einer schwachen Haushaltskonsumtion und Wohninvestitionen bei, und die wirtschaftliche Aussicht ist sehr unsicher.

Trotz langsamen Wachstums im Haushaltsverbrauch, das auf steigende Kosten und Zinssätze zurückzuführen ist, könnten sich stabilisierende reale Einkommen später im Jahr positiv auf den Verbrauch auswirken. Die Wachstumsrate der Lohnstückkosten bleibt hoch, trotz Anzeichen einer Mäßigung. Die RBA prognostiziert, dass die Inflation im Jahr 2025 in die Zielspanne von 2-3 Prozent zurückkehren und 2026 das Pivot-Mittel erreichen wird.

Es wird erwartet, dass die Preisinflation bei Dienstleistungen nachlässt, da Nachfrage und Kostenwachstum sinken, während die Beschäftigung mäßig steigt. Unsicherheiten über globale Einflüsse, Chinas Wirtschaft und „regionale Konflikte“, sowie die Auswirkungen von Verzögerungen in der Geldpolitik, Preisentscheidungen von Unternehmen und ein enger Arbeitsmarkt auf inländische Löhne und Inflation, bestehen weiterhin.

Die höchste Priorität der RBA ist es, die Inflation in den Zielbereich zurückzuführen, wobei der Weg der Zinssätze, um dies zu erreichen, ungewiss bleibt. Der Vorstand wird sich auf Daten und Risikobewertungen verlassen und die globale Wirtschaft, die inländische Nachfrage und die Aussichten für Inflation und Arbeitsmarkt genau beobachten. Die RBA ist entschlossen, die Inflation auf das Ziel zurückzuführen.

Die Federal Reserve veröffentlichte ihre FOMC-Erklärung, die darauf hinweist, dass jüngste Indikatoren zeigen, dass die wirtschaftliche Aktivität mit anhaltend starken Arbeitsplatzgewinnen und niedriger Arbeitslosigkeit solide expandiert. Trotz einer Abschwächung bleibt die Inflation erhöht.

Das Komitee strebt langfristig maximale Beschäftigung und eine Inflation von 2 Prozent an und sieht nun eine bessere Balance der Risiken für diese Ziele. Die Unsicherheit der wirtschaftlichen Aussichten erfordert eine genaue Beobachtung der Inflationsrisiken.

Zur Unterstützung seiner Ziele beschloss das Komitee, den Zielbereich für den Federal Funds Rate unverändert bei 5,25 bis 5,5 Prozent zu halten. Zukünftige Anpassungen werden auf Basis eingehender Daten, der sich entwickelnden Aussichten und der Risikobilanz erfolgen. Eine Senkung der Zielspanne wird nicht erwartet, bis es größeres Vertrauen gibt, dass sich die Inflation nachhaltig auf 2 Prozent zubewegt. Die Reduzierung des Bestandes an Staatspapieren und Schulden von Agenturen wird wie geplant fortgesetzt.

Das Komitee bleibt fest entschlossen, die Inflation wieder auf sein Ziel von 2 Prozent zu bringen. Es wird die Auswirkungen eingehender Informationen auf die Wirtschaft beobachten und die Geldpolitik bei Bedarf anpassen, um Risiken für seine Ziele entgegenzuwirken. Dies wird die Berücksichtigung von Arbeitsmarktbedingungen, Inflationsdruck und -erwartungen sowie finanzielle und internationale Entwicklungen beinhalten.

Am 21. März 2024 gab die Nationalbank bekannt, dass sie die Geldpolitik lockert und den SNB-Leitzins auf 1,5% senkt. Diese Änderung trat zum 22. März 2024 in Kraft. Bis zu einer gewissen Limite werden Sichtguthaben der Banken zum Leitzins verzinst, darüber hinaus zu 1,0%. Die Nationalbank steht weiterhin bereit, bei Bedarf am Devisenmarkt aktiv zu werden.

Die Lockerung erfolgte, da die Inflation in den letzten Monaten unter 2% gefallen ist, was der von der Nationalbank angestrebten Preisstabilität entspricht. Die neue Prognose geht davon aus, dass die Inflation auch in den kommenden Jahren in diesem Bereich bleiben wird. Der Entscheid berücksichtigt den verminderten Inflationsdruck und trägt zur Unterstützung der wirtschaftlichen Entwicklung bei.

Die Inflationsentwicklung wird weiterhin genau beobachtet, um sicherzustellen, dass sie mittelfristig im Bereich der Preisstabilität bleibt. Die Inflation lag im Februar bei 1,2% und wird hauptsächlich von der Teuerung inländischer Dienstleistungen bestimmt. Eine Abwärtsrevision wird auf kürzere Effekte und geringere Zweitrundeneffekte zurückgeführt.

Das weltwirtschaftliche Wachstum blieb moderat, wobei die Inflation in vielen Ländern über den Zielwerten liegt und die Zentralbanken meist eine restriktive Geldpolitik beibehalten. Die Schweizer Wirtschaft verzeichnete ein moderates Wachstum, wobei der Dienstleistungssektor wuchs und die Industrie stagnierte. Die Arbeitslosigkeit stieg leicht an und für dieses Jahr wird ein BIP-Wachstum von etwa 1% erwartet.

In seiner jüngsten Sitzung hat das Komitee der Bank of England beschlossen, den Leitzins bei 5,25% zu belassen. Die maßgebliche CPI-Inflation sinkt, bleibt jedoch aufgrund von Basis- und externen Effekten aus Energie- und Warenpreisen hoch. Die restriktive Ausrichtung der Geldpolitik wirkt sich auf die reale Wirtschaft aus, was zu einem lockereren Arbeitsmarkt führt und den Inflationsdruck verringert. Dennoch bleiben die Indikatoren für die Inflationspersistenz erhöht.

Die Geldpolitik muss restriktiv bleiben, um das Inflationsziel von 2% mittelfristig nachhaltig zu erreichen. Seit langem ist sich das Komitee einig, dass die Politik restriktiv bleiben muss, um das Risiko zu mindern, dass die Inflation über dem Ziel bleibt. Das Geldpolitische Komitee (MPC) ist bereit, die Geldpolitik nach wirtschaftlichen Daten anzupassen, um sicherzustellen, dass die Inflation zum 2%-Ziel zurückkehrt, und wird anhaltenden Inflationsdruck und die Widerstandsfähigkeit der Wirtschaft genau beobachten, einschließlich des Arbeitsmarktes, des Lohnwachstums und der Inflation bei Dienstleistungen.

Weltweit spiegeln das von Großbritannien gewichtete BIP-Wachstum gemischte Ergebnisse wider, wobei die USA schneller als erwartet wuchsen. Chinas Wachstum erreichte die Regierungsziele und in anderen Schwellenländern wurden gemischte Ergebnisse beobachtet. Die Arbeitsmärkte blieben angespannt und das Lohnwachstum verlangsamte sich sowohl im Euroraum als auch in den USA, blieb aber in Großbritannien höher. Während die Inflation bei Dienstleistungen anhält, wird das Komitee Einflüsse wie die chinesische Wirtschaft und „Konflikte“, die die wirtschaftliche Aussicht beeinflussen, genau beobachten.

Das Hauptziel des Komitees besteht darin, die Inflation wieder auf das Zielniveau zu bringen, wobei die Erwartungen für die mittlere Frist mit diesem Ziel übereinstimmen. Obwohl aktuelle Daten zeigen, dass sich die Inflation entspannt, wird keine kurzfristige Senkung des Zielbereichs für den Federal Funds Rate erwartet. Geldpolitische Anpassungen werden von den Daten abhängig sein, dabei wird auf Trends in der Weltwirtschaft, der inländischen Nachfrage und der Arbeitsmarktaussichten geachtet.

Zu erwähnen sind die neuen Allzeit-hochs an den Aktienmärkten, dem Goldmarkt, sowie eine besondere Heraushebung für die neue Geldpolitik der Bank of Japan. Eine positives Agglomerat, die Schilde der Finanzplätze weltweit sind intakt und können sich über historische Notierungen freuen.

Nothing is more magnificent then the intensities of colors that dominate this garden for two weeks in spring and perhaps three weeks in autumn. The colors seem to radiant above the trees, almost as if generated by the God I do not believe in. [Michael Steinhardt, No Bull]

Nothing is more magnificent then the intensities of colors that dominate this garden for two weeks in spring and perhaps three weeks in autumn. The colors seem to radiant above the trees, almost as if generated by the God I do not believe in. [Michael Steinhardt, No Bull]

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

LG Ben

Goody Traders

03/19/2024, Monetary policy decision of the Bank of Japan (key interest rate: 0.0% +0.1%).

03/19/2024, Monetary policy decision of the Bank of Japan (key interest rate: 0.0% +0.1%).

03/19/2024, Monetary policy decision of the Reserve Bank of Australia (key interest rate: 4.35% +/- 0.0).

03/20/2024, Monetary policy decision of the Federal Reserve Bank (key interest rate: 5.5% +/- 0.0).

03/21/2024, Monetary policy decision of the Swiss National Bank (key interest rate: 1.5% -0.25).

03/21/2024, Monetary policy decision of the Bank of England (key interest rate: 5.25% +/- 0.0).

The Bank of Japan projects that the 2% price stability target will be reached sustainably by the end of January 2024. The bank’s Quantitative and Qualitative Monetary Easing with Yield Curve Control and negative interest rate policies have been effective. The short-term interest rate remains the primary tool for monetary policy, as it aims to achieve the 2% target stably.

Market operations decisions include maintaining the uncollateralized overnight call rate around 0 to 0.1 percent until March 21, 2024, and continuing to buy Japanese government bonds. The bank plans to halt the purchase of ETFs, J-REITs, CP, and corporate bonds gradually within a year and offer loans at a 0.1 percent interest rate, tied to the increase in the lender’s loan balance.

Japan’s moderate economic recovery is fueled by better corporate profits, a tight labor market, and potential wage growth. Rising wages have driven a moderate increase in prices, suggesting a strengthening of the wage-price cycle. The Board has minority dissenting opinions favoring the continuation of negative interest rates to support smaller firms.

Uncertainties in global economics, commodity prices, and domestic wage-price behaviors pose high risks, and vigilant monitoring of financial and foreign exchange market impacts on Japan’s economy is necessary. Despite this, Japan’s economy is expected to grow moderately, with positive outcomes from accelerating cycles of income and spending and an anticipated CPI increase above 2%.

The Reserve Bank of Australia (RBA) kept the cash rate target unchanged at 4.35 percent and the interest rate on Exchange Settlement balances at 4.25 percent. Inflation moderates but remains high, with headline CPI steady at 3.4 percent over the past year. Goods inflation is slowing while services inflation, though high, is moderating more gradually.

High interest rates aim to balance demand and supply in the economy, resulting in a gradual easing of tight labor market conditions. Wages growth is expected to moderate, and current levels align with inflation targets if productivity reaches its long-term average. Inflation’s impact on real incomes contributes to weak household consumption and dwelling investment, and the economic outlook is highly uncertain.

While slow growth in household consumption persists amid rising costs and interest rates, stabilizing real incomes may support consumption later in the year. Unit labor costs‘ growth remains high despite signs of moderation. The RBA forecasts inflation to return to the 2-3 percent target range in 2025 and to the midpoint in 2026.

Services price inflation is expected to decline as demand and cost growth ease, while employment grows moderately. Uncertainties around global influences, China’s economy, and regional conflicts, as well as the effects of monetary policy lags, business pricing, and tight labor market on domestic wages and inflation, persist.

The RBA’s highest priority is to return inflation to the target range, with the path of interest rates to achieve this remaining uncertain. The Board will depend on data and risk assessments, closely watching the global economy, domestic demand, and inflation and labor market outlooks. It is determined to return inflation to target.

The Federal Reserve released its FOMC statement, indicating that recent indicators show economic activity expanding at a solid pace, with continued strong job gains and low unemployment. Despite easing, inflation remains elevated.

The Committee aims for maximum employment and 2 percent inflation over the long term and now sees risks to these goals as better balanced. The economic outlook’s uncertainty requires close attention to inflation risks.

To support its objectives, the Committee decided to maintain the federal funds rate at 5-1/4 to 5-1/2 percent. Future adjustments will be based on incoming data, outlook, and risk balance. A reduction in the target range is not anticipated until there’s greater confidence that inflation is moving sustainably toward 2 percent. The reduction of Treasury security and agency debt holdings will continue as previously planned.

The Committee remains strongly committed to returning inflation to its 2 percent goal. It will monitor incoming information implications for the economy and adjust monetary policy if necessary to address risks to its objectives. This will involve considering labor market conditions, inflation pressures, expectations, and financial and international developments.

On March 21, 2024, the National Bank announced that it is easing its monetary policy and lowering the SNB key interest rate to 1.5%. This change will take effect from March 22, 2024. Sight deposits at the bank will be remunerated at the key interest rate up to a certain threshold, and above this threshold at 1.0%. The National Bank remains ready to intervene in the foreign exchange market if necessary.

The relaxation was made possible as inflation has fallen below 2% in recent months, aligned with the National Bank’s goal of price stability. The new forecast anticipates that inflation will stay within this range over the coming years. The decision takes into account the diminished inflationary pressure and contributes to supporting economic development.

Inflation development will continue to be closely monitored to ensure it stays in the range of price stability over the medium term. In February, inflation was at 1.2%, mainly driven by higher prices for domestic services. A downward revision is attributed to shorter effects and smaller second-round effects.

Global economic growth remained moderate, while inflation in many countries is still above central bank targets, leading to predominantly restrictive monetary policies. The Swiss economy saw moderate growth, with the service sector expanding and industrial production stagnating. Unemployment has risen slightly, and an economic growth of around 1% is expected for this year.

In its recent meeting, the Bank of England’s Committee voted to maintain the Bank Rate at 5.25%. Headline CPI inflation is falling but remains high due to base and external effects from energy and goods prices. The restrictive stance of monetary policy is impacting the real economy, leading to a looser labour market and reducing inflationary pressures. However, inflation persistence indicators remain elevated.

Monetary policy must stay restrictive to sustainably achieve the 2% inflation target in the medium term. The Committee has long viewed that policy needs to remain restrictive to mitigate the risk of inflation remaining above the target. The MPC is prepared to adjust policy following economic data to ensure inflation returns to the 2% target and will monitor persistent inflationary pressures and the economy’s resilience, including the labour market, wage growth, and services price inflation.

Globally, the UK-weighted GDP growth reflected mixed outcomes, with the US growing faster than expected. China’s growth met government targets, and mixed results were observed in other emerging markets. Labor markets showed continued tightness, and wage growth slowed in both the euro area and the US, while remaining higher in the UK. While services inflation persists, the Committee will closely watch influences like the Chinese economy and conflicts affecting the economic outlook.

The Committee’s primary objective is to bring inflation back to target, detailing that medium-term expectations align with this goal. Although recent data shows inflation easing, there is no expectation of a near-term reduction in the target range for the federal funds rate. Monetary policy adjustments will be data-dependent, and attention will be paid to trends in the global economy, domestic demand, and labour market outlook.

Worth mentioning are the new all-time highs on the stock markets, the gold market, and a special mention for the new monetary policy of the Bank of Japan. A positive agglomerate, the shields of financial centers worldwide are intact and can look forward to even higher historic quotations.

Nothing is more magnificent then the intensities of colors that dominate this garden for two weeks in spring and perhaps three weeks in autumn. The colors seem to radiant above the trees, almost as if generated by the God I do not believe in. [Michael Steinhardt, No Bull]

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben

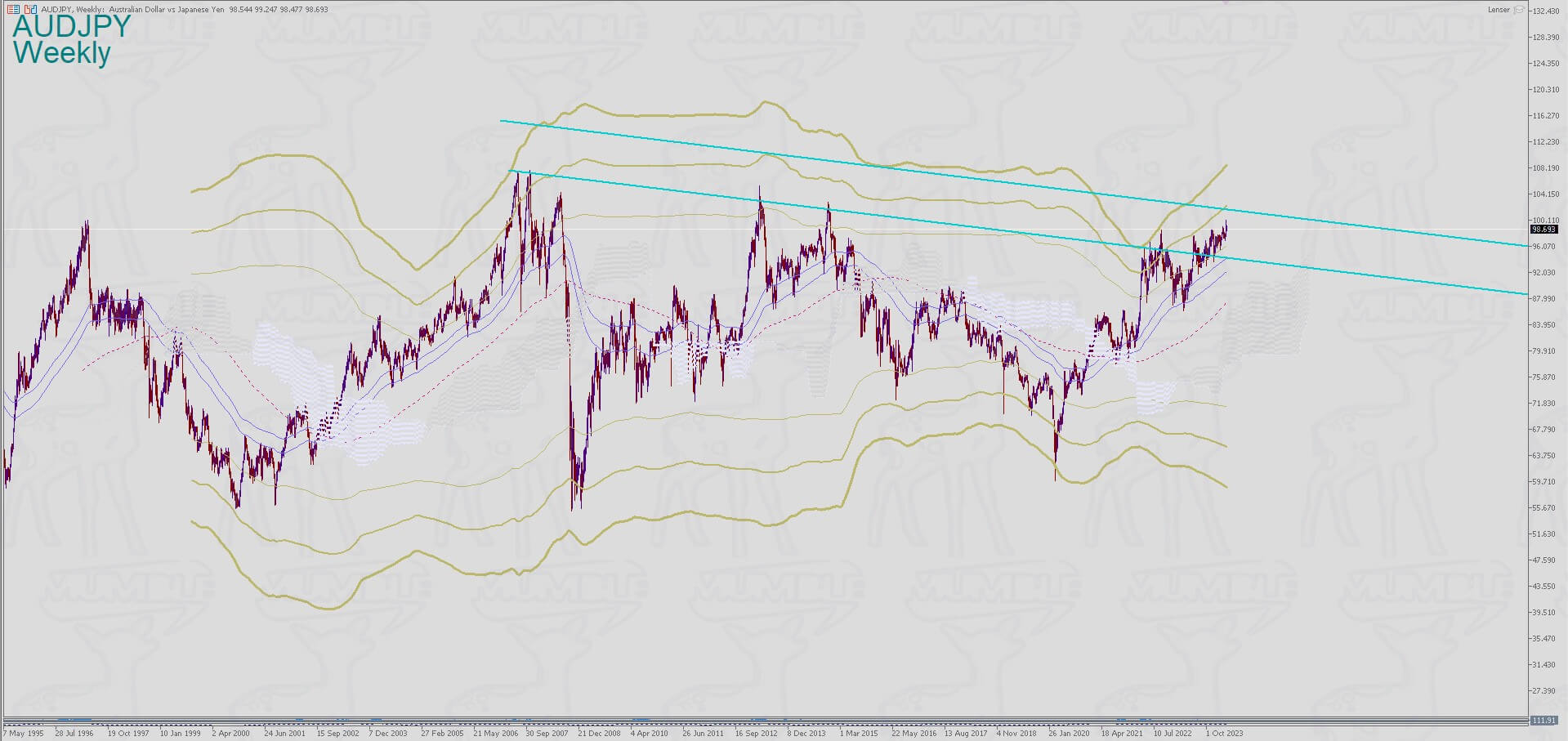

AUDJPY Weekly

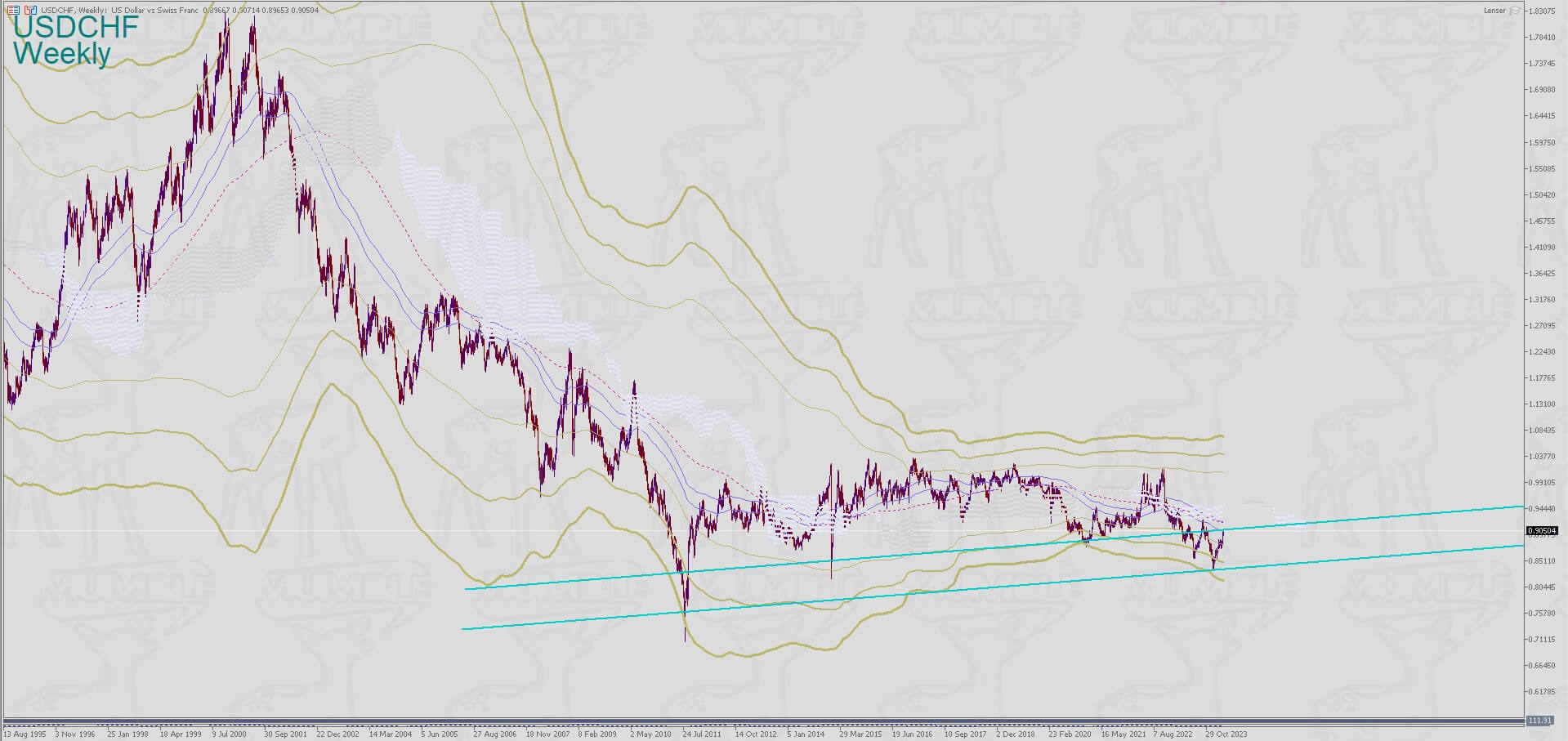

USDCHF Weekly

GBPJPY Weekly

Central Bank Policy | IN18L 19.03.2024 JAPAN | www.youtube.com/@CNBC-TV18

Governor Michele Bullock spoke at the Reserve Bank of Australia Media Conference following the March monetary policy decision

YouTube-Player

While the BoE refuses to give the public a press conference, the Prime Minister is the man.

Externe Quellen/Links