Guten Morgen Traders,

kurzzeitig musste ich meinen Besuch auf der Stuttgarter-Invest auschecken, dennoch habe ich mir zwei Vorträge online mitangesehen. Guter Quark von Herrn Julius Weiß. Jetzt haben wir alle wieder die Freitag^3 (großer Verfallstag) auf unserem Radar.

kurzzeitig musste ich meinen Besuch auf der Stuttgarter-Invest auschecken, dennoch habe ich mir zwei Vorträge online mitangesehen. Guter Quark von Herrn Julius Weiß. Jetzt haben wir alle wieder die Freitag^3 (großer Verfallstag) auf unserem Radar.

Ein Vortrag mit dem Titel „Commodities 2022: Ist Gold ein sicherer Hafen in unruhigen Zeiten?“ wurde an beiden Messetagen wiedergekäut. Wieso, gibt es nicht genügend Aussteller und Themen? Jedenfalls habe ich den Samstag-Vortrag miterlebt.

Zunächst vermisste ich die beiden angekündigten Referenten der Deutschen Börse, Michael König und Mateja Maric. Ich versuche noch den Namen des tatsächlich aufgetretenen Referenten herauszufinden. Das Thema selbst wurde etwas salop behandelt und ich könnte kritisch meinen, seicht.

Große Hedge-Fonds hätten eine gewisse Menge Gold Eintragungen in ihren Portfolios, was als großes Kaufargument für das Edelmetall präsentiert wurde. Dabei wird von genannten Vermögensverwaltern nicht mehr erwartet, als mindestens genauso gut zu performen, wie die Aktienmärkte. Da die Börse nicht nur steigt, sondern auch korrigiert, wobei Gold als negative korreliert ausgewiesen wird, muss logischer-weise eine bestimmte Menge dieses „Risk-Off“ Assets beigemischt sein. Das ist an sich kein Argument für Gold, sondern eher für Leerverkäufe und echtes Long-Short Value-Picking, was sich die Milliardenschweren-Hedgies aber nie antun würden. Lieber aquirieren diese Blue-Chips eines jeden Index und kaufen exakt die Menge an Gold an, welche es statistisch ermöglichen könnte, einer Korrektur dieser Papiere, einem Under-Performen (der Märkte) beizukommen.

Kein Wort von Allzeithochs am Goldmarkt, von wichtigen Korrelationen wie S&P/Gold, Crude/Gold, Gold/Silber, ect. Dennoch sagte der Referent einen wichtigen Satz, dass nämlich Gold bei einem Börsen-Crash abverkauft werden würde, um mit dem Cash größere Aktien-Kredite aufnehmen zu können.

Genau diese Korrekturen an den Börsen nämlich gilt es zu beachten, wenn man in Gold spekulieren möchte. Dazu betrachtet man seine übrigen Indikatoren und fängt bei Erreichen seiner Preislimits immer aggressiver an, Gold digital ins Account zu transferieren.

Prinzipiell ist der Preis für Gold gleich einer imaginären Wertschöpfung. Wie etwa ein Nummer-1 Popsong oder ein Kino-Blockbuster. Der Bedarf an Gold für technische Anwendungen liegt weit unter dem Angebot. Daher kaufe ich Gold lieber viel billiger als nur einen Cent zu Teuer.

Unter $1.500 gilt der Goldmarkt als Bärenmarkt, immer unter Berücksichtigung der oben erwähnten Korrelationen.

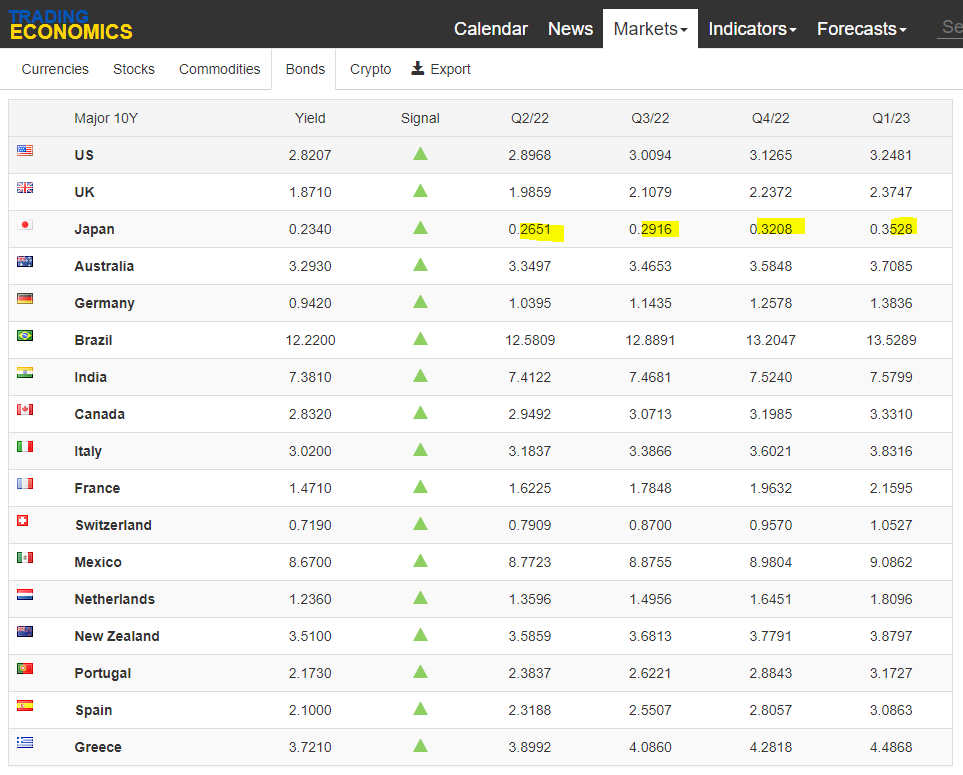

Japan wählt ab Ende Juni einen neuen Vorsitz für seine Bank of Japan. Genau der Zeitpunkt, ab da die Marktoperationen zur Kontrolle der Yield-Kurve enden sollen.

Ich habe ab Donnerstag ein verlängertes „No-Margin-Call“ Wochenende, so kann ich für meine Premium-Abonnenten wieder in das (interaktive) Webcasting einsteigen. Es erwarten Euch spannende Makro’s aber auch detaillierte Forex-Trades.

Also schaut immer mal wieder rein, und holt Euch Trades inklusive Risikomanagement.

centralbanking.com – Japan Yield Curve control

macrotrends.net – SP500 to Gold ratio

gurufocus.com – Alles rund um die Märkte

optionen-investor.de – „Hexensabbat“

extraetf.com – Norwegischer Staatsfonds ETF

htp-trockeneis.de – Trockeneis für Events und Projekte

Weitere Details und Ausblick auf den Exchange wie immer für Premium-Mitglieder.

Bünyamin

Goody Traders,

I had to punch out my visit to the German financial fair ‚Invest‘ in Stuttgart, but I still watched two presentations online. Good mustard from Mr. Julius Weiß. Now we all have the Friday^3 (Triple witching hour) on our radar again.

I had to punch out my visit to the German financial fair ‚Invest‘ in Stuttgart, but I still watched two presentations online. Good mustard from Mr. Julius Weiß. Now we all have the Friday^3 (Triple witching hour) on our radar again.

A talk entitled „Commodities 2022: Is Gold a Safe Haven in Troubled Times?“ was given on both days of the fair. Why, aren’t there enough exhibitors and topics? Anyway, I witnessed the Saturday lecture.

First of all, I missed the two announced speakers from Deutsche Börse, Michael König and Mateja Maric. I’m still trying to find out the name of the speaker who actually presented the lecture. The topic itself was treated somewhat casually and I could say critically, shallowly.

Large hedge funds would have a certain amount of gold listings in their portfolios, which was presented as a major buying argument for the precious metal. The asset managers mentioned are not expected to do more than perform at least as well as the stock markets. Since the stock market is not only rising, but also correcting, with gold being shown as negatively correlated, there must logically be a certain amount of this „risk-off“ asset mixed in. This isn’t an argument for gold per se, but rather for short selling and true long-short value picking, which the billionaire hedge-buddies are too comfortable to do. Roughly speaking, they prefer to buy the blue chips of each index and buffer these with exactly the amount of gold that statistically could enable a correction of these papers, without the risk of underperformance of their own financial products.

Not a word of all-time highs in the gold market, of important correlations such as S&P/Gold, Crude/Gold, Gold/Silver, ect.

Nevertheless, the speaker said an important sentence, namely that gold would be sold off in a stock market crash in order to avoid an underperformance of their own stock market operations.

Exactly these corrections on the stock exchanges have to be considered if you want to speculate in gold. To do this, you look at your other indicators and start to transfer gold digitally into your account more and more aggressively when you reach your buy limits.

In principle, the price of gold is equal to an imaginary value creation. Like a #1 pop song or a blockbuster movie. The demand for gold for technical applications is far below the supply.

That’s why I’d rather buy gold a lot cheaper than just a cent too expensive.

Japan will elect a new chairmanship for its Bank of Japan from the end of June. Exactly when the market operations to control the yield curve should end.

I have an extended „no margin call“ weekend starting Thursday, so I can get back into (interactive) webcasting for my premium subscribers. Expect exciting macros but also detailes for risk-premium forex trades.

So keep punching back and get my trades with it risk management calculations included.

centralbanking.com – Japan Yield Curve control

macrotrends.net – SP500 to Gold ratio

gurufocus.com – infos worth a look

optionen-investor.de – Triple witching hour

extraetf.com – Norwegischer Staatsfonds ETF

More details and my outlook on the Foreign Exchange as always for Premium Members.

Sincerely Yours, Ben