Long Story, Short

2024-09-01 16:01:48CEST (UTC+2)Goody Traders

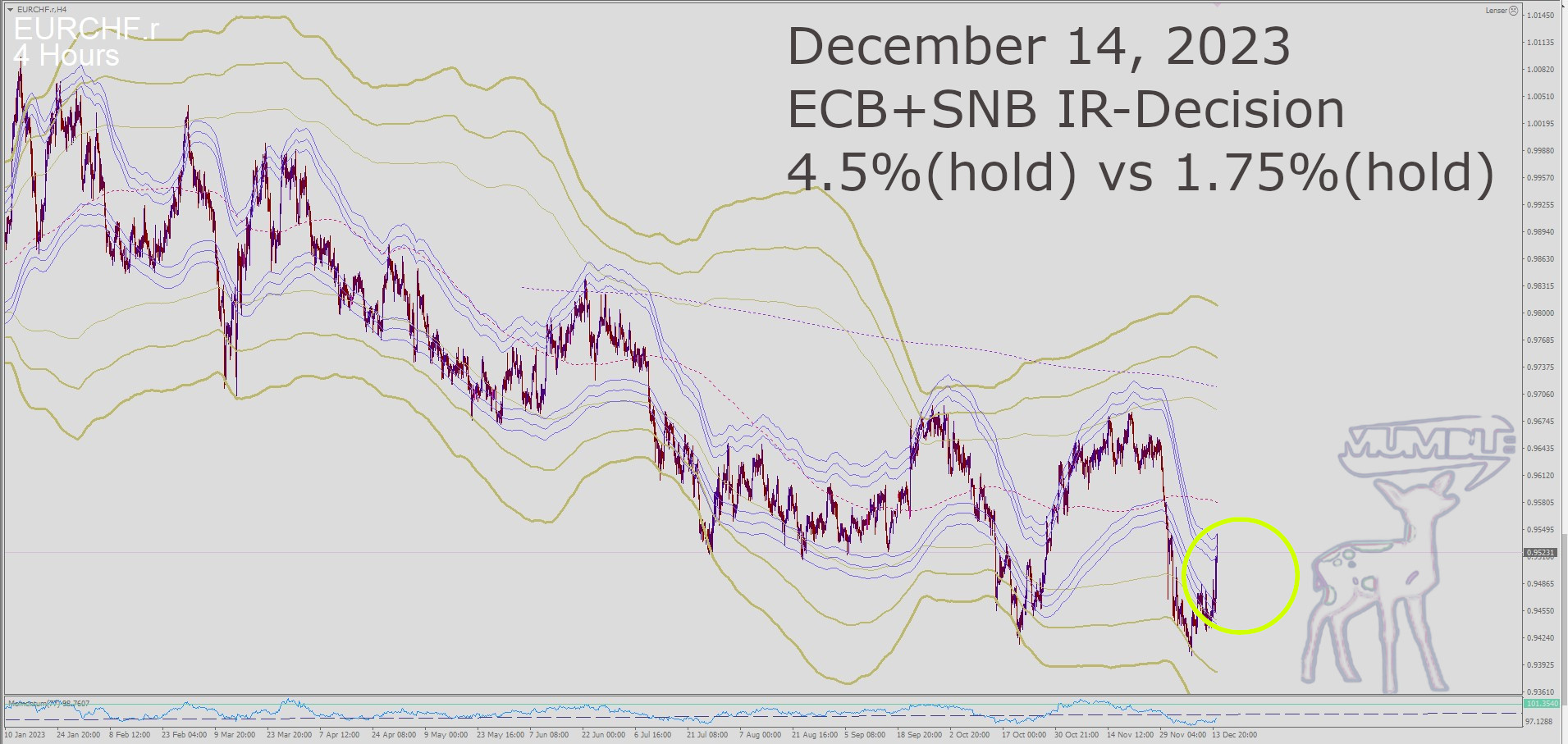

18.07.2024, Geldpolitische Entscheidung der EZB (Leitzinssatz: 4,25 % +/- 0,0)

18.07.2024, Geldpolitische Entscheidung der EZB (Leitzinssatz: 4,25 % +/- 0,0)

24.07.2024, Geldpolitische Entscheidung der BoC (Leitzinssatz: 4,50 % – 0,25)

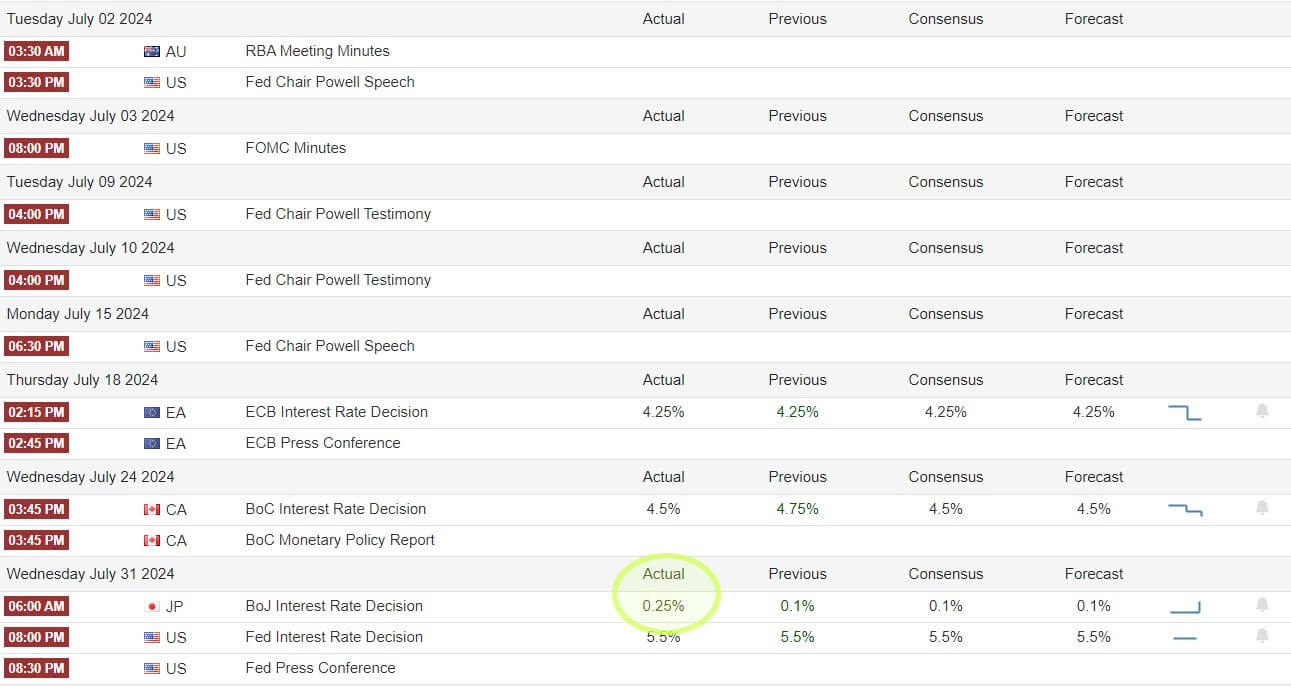

31.07.2024, Geldpolitische Entscheidung der BoJ (Leitzinssatz: 0,25 % + 0,15)

31.07.2024, Geldpolitische Entscheidung der FED (Leitzinssatz: 5,50 % +/- 0,0)

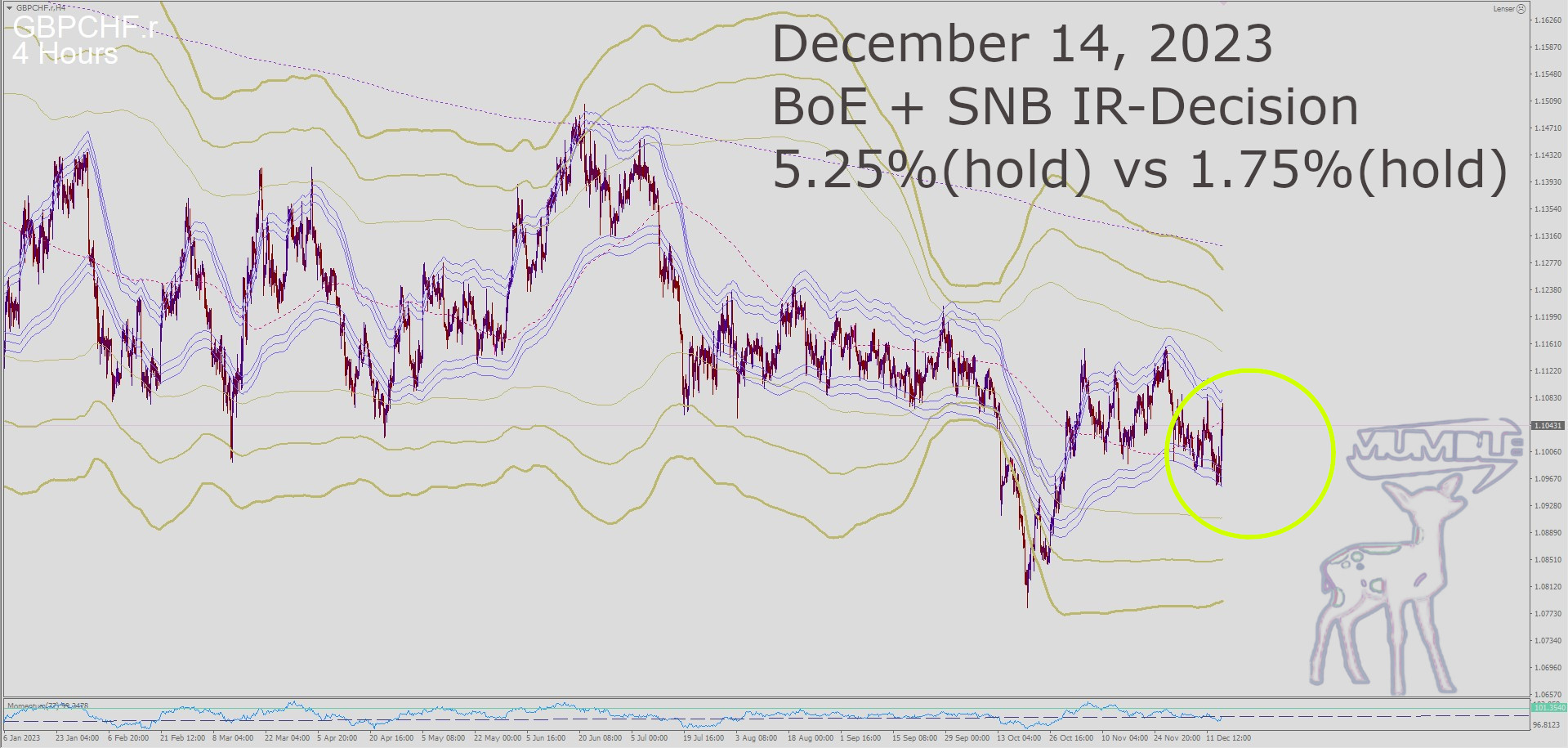

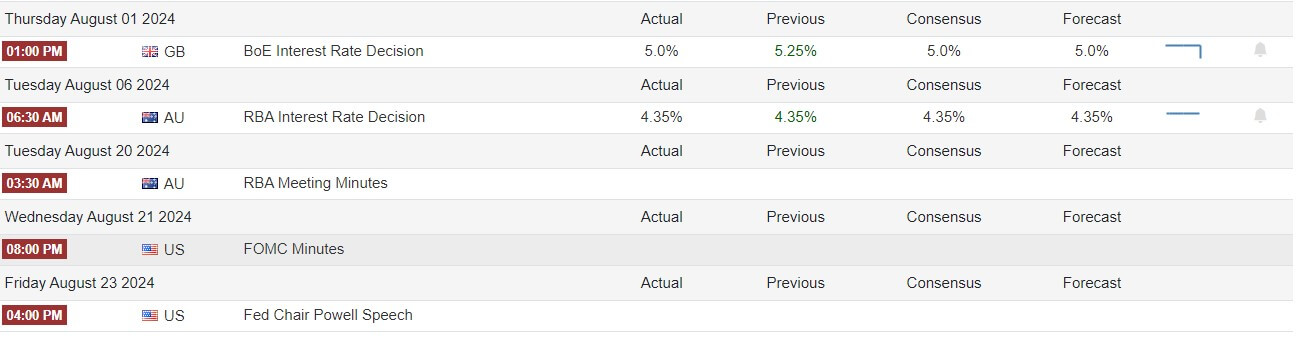

01.08.2024, Geldpolitische Entscheidung der BoE (Leitzinssatz: 5,00 % – 0,25)

06.08.2024, Geldpolitische Entscheidung der RBoA (Leitzinssatz: 4,35 % +/- 0,0)

22.08. bis 24.08. Jackson Hole Economic Symposium

1. Geldpolitische Entscheidung der EZB am 18. Juli 2024

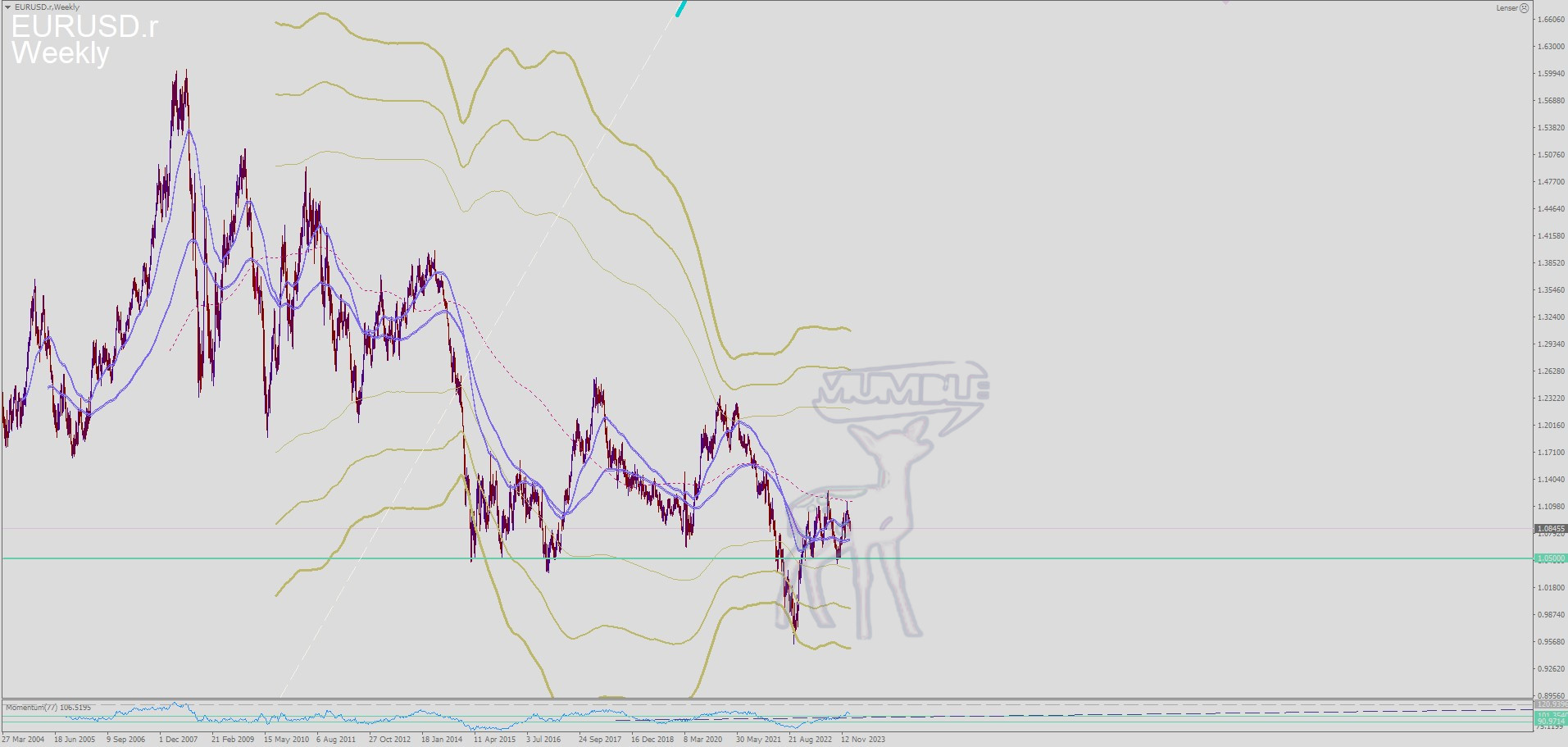

Am 18. Juli 2024 entschied sich die Europäische Zentralbank (EZB), ihre Zinssätze unverändert zu lassen, was ihren vorsichtigen Ansatz angesichts der Herausforderungen durch das verlangsamte Wirtschaftswachstum in der Eurozone widerspiegelt. Trotz des anhaltenden Inflationsdrucks wurde die Entscheidung der EZB als ein Gleichgewicht zwischen Inflationskontrolle und Unterstützung der Wirtschaft angesehen. Dieser Schritt verhalf dem Euro zu Stärke, insbesondere gegenüber dem US-Dollar, da die Märkte erwarten, dass die FED in den kommenden Monaten zu vermehrten Zinssenkungen neigen könnte.

2. Zinssenkung der Bank of Canada am 24. Juli 2024

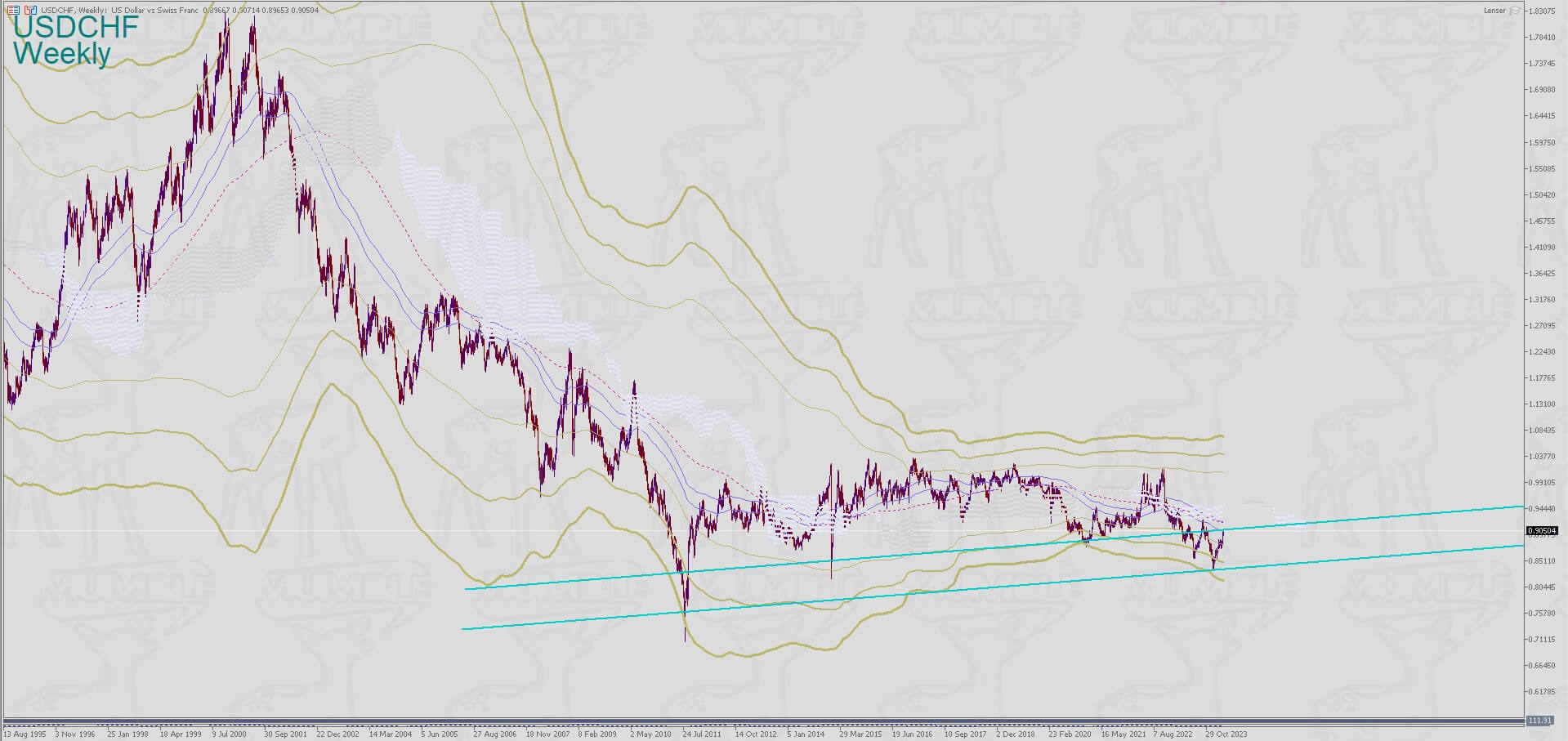

Am 24. Juli 2024 senkte die Bank of Canada (BoC) ihren Leitzins um 25 Basispunkte auf 4,50 %. Diese Entscheidung war durch Bedenken hinsichtlich der Abschwächung der kanadischen Wirtschaft und der negativen Auswirkungen eines starken kanadischen Dollars auf die Exporte motiviert. Die Zinssenkung wurde zwar allgemein erwartet, führte jedoch zu einer kurzen Schwächung des kanadischen Dollars. Die Währung konnte jedoch schnell wieder etwas Boden gutmachen, da der Markt seine Erwartungen hinsichtlich der zukünftigen geldpolitischen Ausrichtung der BoC neu kalibrierte. Das Paar USD/CAD erlebte eine erhöhte Volatilität, da die Händler auf die Zinssenkung und ihre breiteren wirtschaftlichen Auswirkungen reagierten.

3. Zinserhöhung der Bank of Japan am 31. Juli 2024

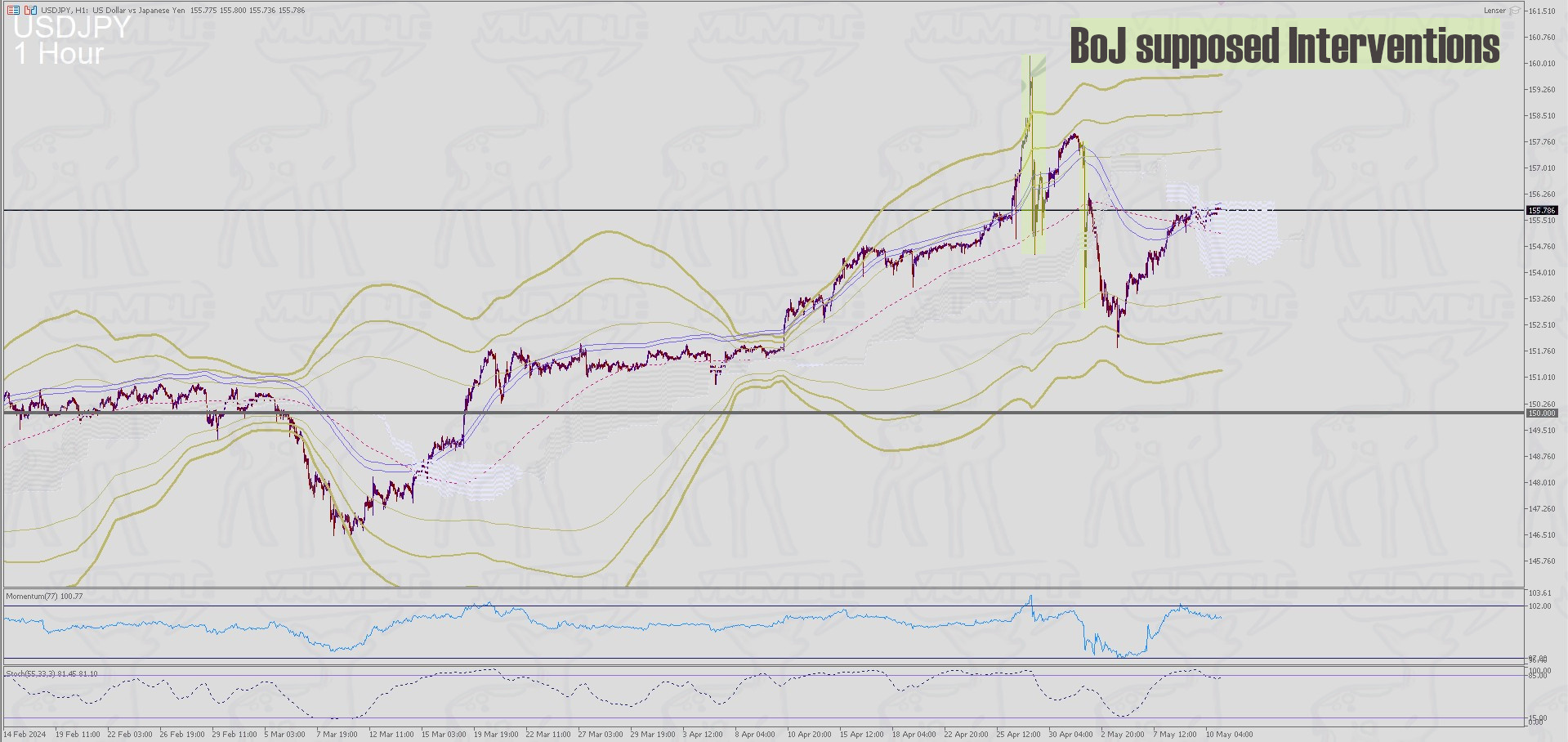

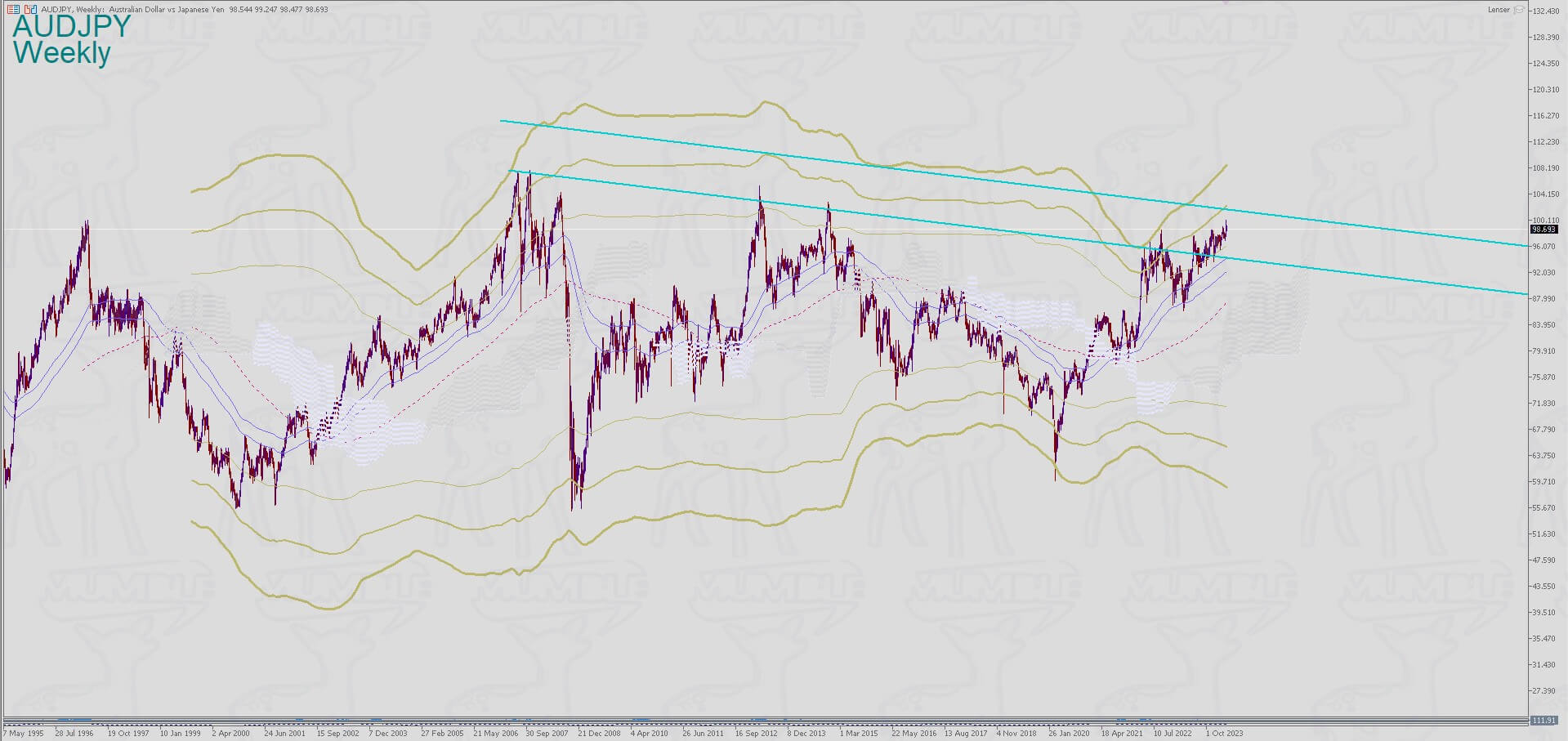

Die Bank of Japan (BoJ) erhöhte ihren Leitzins am 31. Juli 2024 von 0,10 % auf 0,25 %. Dieser Schritt markierte eine Fortsetzung der allmählichen Abkehr der BoJ von ihrer bisherigen ultralockeren Geldpolitik, die bereits damit begonnen hatte, sich von der negativen Zinsepoche zu verabschieden. Die Entscheidung war auf die steigende inländische Inflation und die Notwendigkeit zurückzuführen, den Yen zu stabilisieren, der deutlich schwächer geworden war. Diese Zinserhöhung wurde weitgehend erwartet, da die jüngsten Wirtschaftsdaten auf eine höhere Inflation hindeuteten. Nach der Ankündigung legte der japanische Yen gegenüber dem US-Dollar deutlich zu, was zu einem starken Rückgang im Exchange USD/JPY führte. Die Entscheidung führte auch zu einer Neubewertung der Carry Trades, was die Marktvolatilität erhöhte.

4. Zinssatzkonstanz der Federal Reserve am 31. Juli 2024

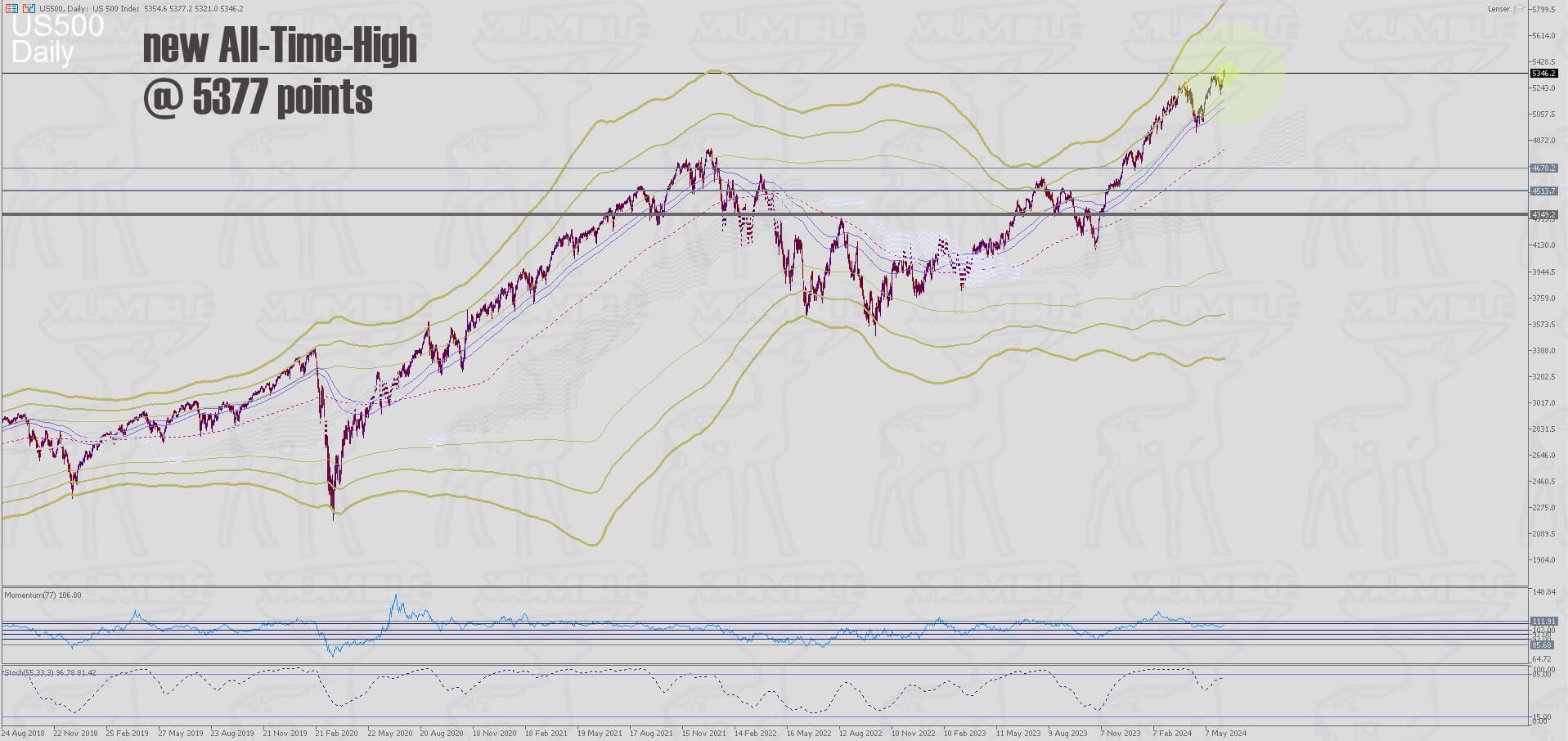

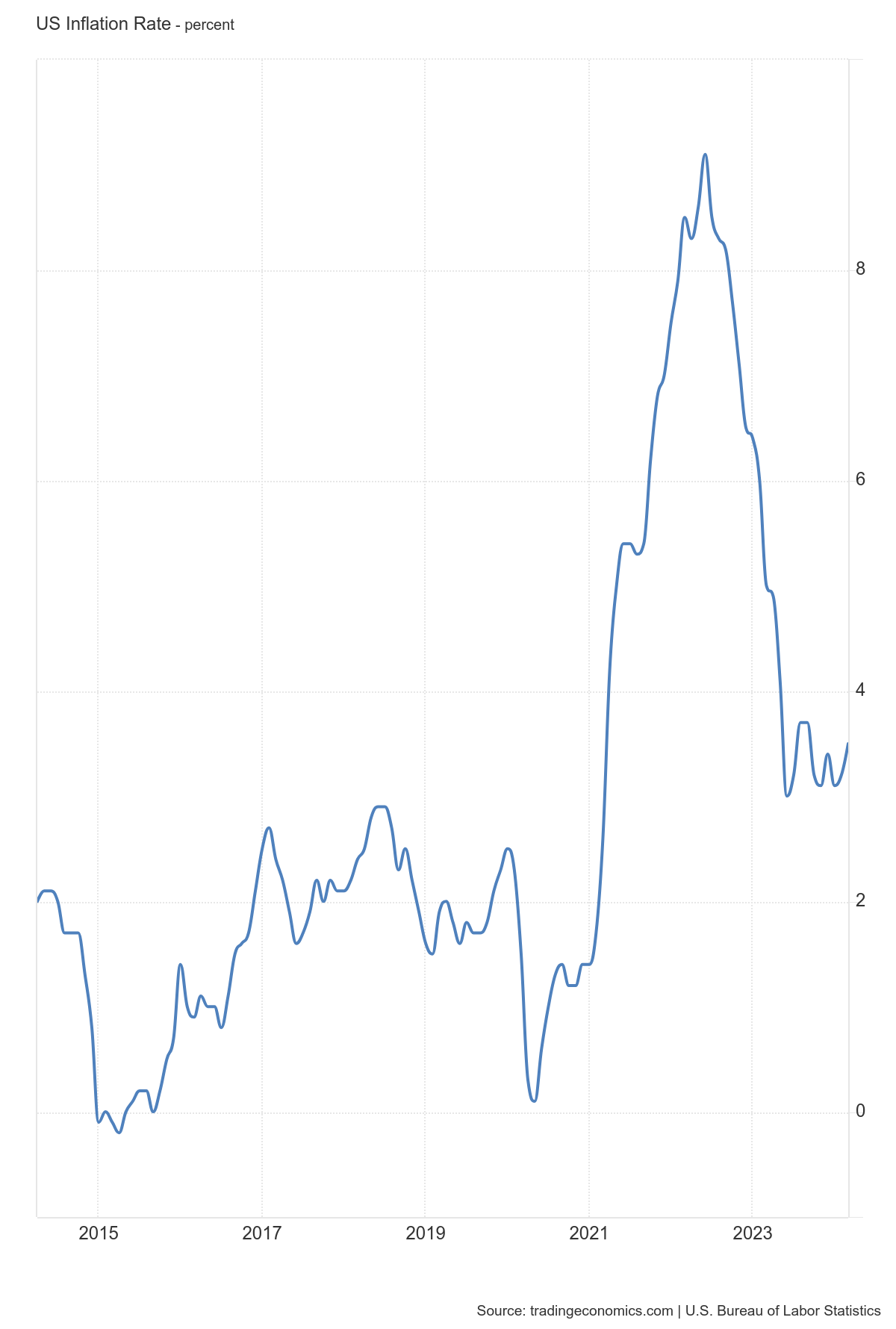

Am 31. Juli 2024 beschloss die Federal Reserve, ihren Leitzinssatz nach einer Reihe von Zinserhöhungen zur Bekämpfung der Inflation, die sich inzwischen bei etwa 2,9 % stabilisiert hat, bei 5,50 % zu belassen. Die Entscheidung, die Zinsen stabil zu halten, wurde allgemein erwartet und spiegelt die vorsichtige Haltung der Fed wider, die jedoch bei Bedarf für künftige Anpassungen offen bleibt. Der US-Dollar schwächte sich nach der Ankündigung weiter ab, da die Spekulationen über mögliche Zinssenkungen in der Zukunft zunahmen. Diese gemäßigte Prognose trug zu einem allgemeinen Rückgang des USD bei, insbesondere gegenüber dem Yen und dem Euro.

5. Zinssenkung der Bank of England am 1. August 2024

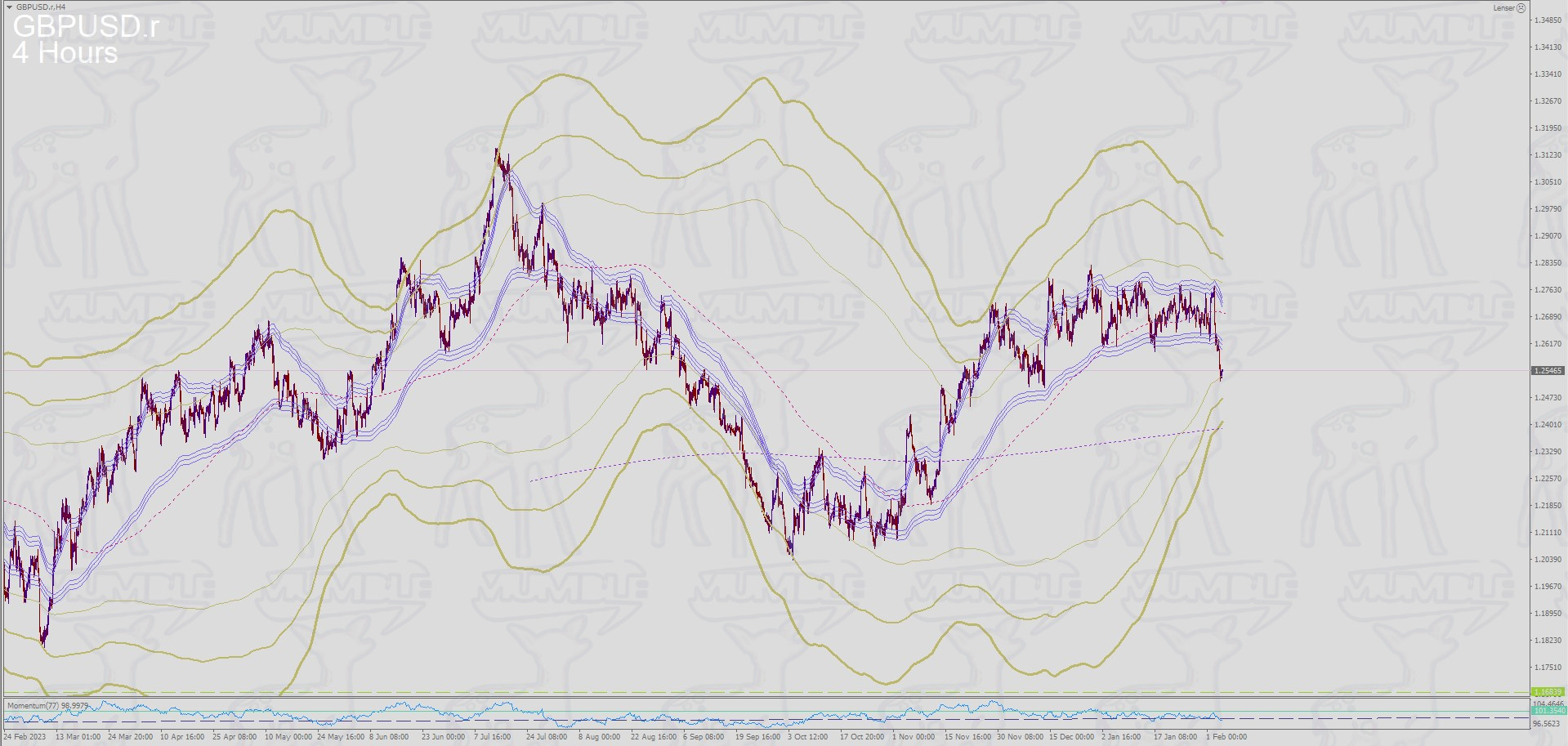

Die Bank of England (BoE) senkte ihren Leitzins am 1. August 2024 von 5,25 % auf 5,00 % und begründete dies mit Bedenken hinsichtlich eines verlangsamten Wirtschaftswachstums und eines schwächelnden Arbeitsmarktes. Obwohl die Inflation über dem Zielwert blieb, wurde die Zinssenkung als notwendig erachtet, um die britische Wirtschaft angesichts zunehmender globaler Unsicherheiten zu unterstützen. Das britische Pfund fiel nach der Ankündigung zunächst stark gegenüber dem US-Dollar und dem Euro, konnte jedoch später einige Verluste wieder aufholen, da die Märkte darüber diskutierten, ob diese Senkung ein einmaliges Ereignis sein oder den Beginn eines längeren Lockerungszyklus signalisieren würde. Das GBP/USD-Paar erlebte erhebliche Schwankungen, da die Auswirkungen der Entscheidung der BoE vom Markt verschiedenlich absorbiert wurden.

6. Zinsfestlegung der Reserve Bank of Australia am 6. August 2024

Am 6. August 2024 beschloss die Reserve Bank of Australia (RBA), ihren Leitzins bei 4,35 % zu belassen. Die Entscheidung der RBA spiegelte trotz anhaltender Inflationssorgen einen vorsichtigen Ansatz angesichts gemischter Konjunktursignale wider, insbesondere schwacher Verbraucherausgaben und eines fragilen Immobilienmarkts. Der australische Dollar erlebte nach der Ankündigung nur begrenzte Bewegungen, erholte sich jedoch später aufgrund steigender Rohstoffpreise und einer verbesserten Marktstimmung. Der Exchange AUD/USD blieb relativ stabil, mit kurzen Phasen der Volatilität, während Händler die geldpolitischen Entscheidungen der RBA beurteilten.

Währungspaar

Neuster Trend (ab dem 18. July 2024)

USD/JPY

Signifikante Abwärtsbewegung, hohe Volatilität

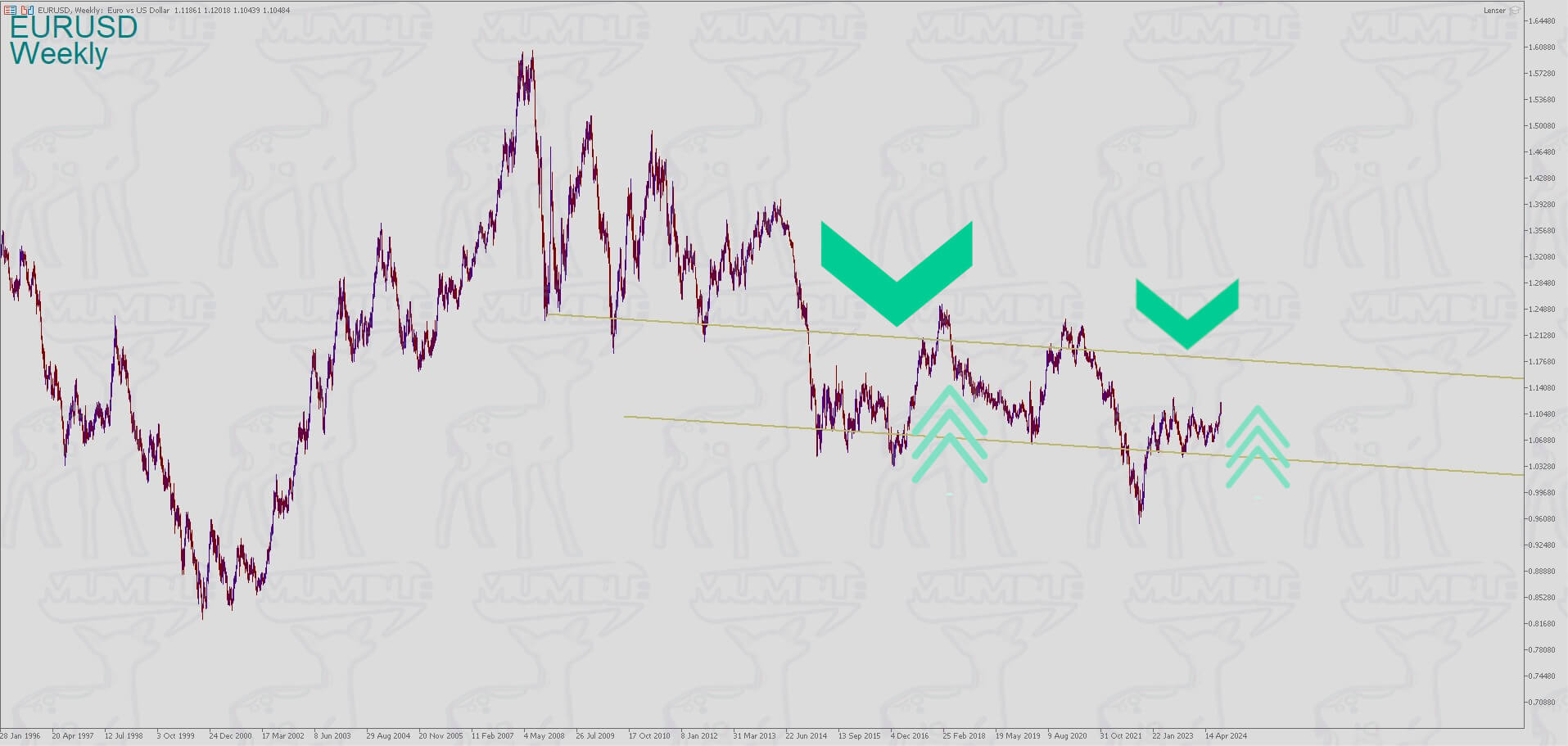

EUR/USD

Euro mit Zugewinnen, schwächelder USD

GBP/USD

Die Erwartungen wurden übertroffen; allerdings wird von einem rigiden Wachstum ausgegangen

USD/CAD

Bullen und Bären gleichauf; warten auf nachlassenden Inflationdruck

AUD/USD

An den Inflationserwartungen ausgerichtete Kursbewegungen

World Economic Forum @Jackson Hole, Wyoming

Der Vorsitzende der US-Notenbank, Jerome Powell, erklärte in seiner mit Spannung erwarteten Rede, dass  die Zeit für eine Anpassung der Geldpolitik gekommen ist, was auf ein wachsendes Vertrauen in die Entwicklung der Inflation schließen lässt. Dieser gemäßigte Kurswechsel des Fed-Vorsitzenden wurde von anderen großen Zentralbanken wie der Bank of England und der Europäischen Zentralbank wiederholt.

die Zeit für eine Anpassung der Geldpolitik gekommen ist, was auf ein wachsendes Vertrauen in die Entwicklung der Inflation schließen lässt. Dieser gemäßigte Kurswechsel des Fed-Vorsitzenden wurde von anderen großen Zentralbanken wie der Bank of England und der Europäischen Zentralbank wiederholt.

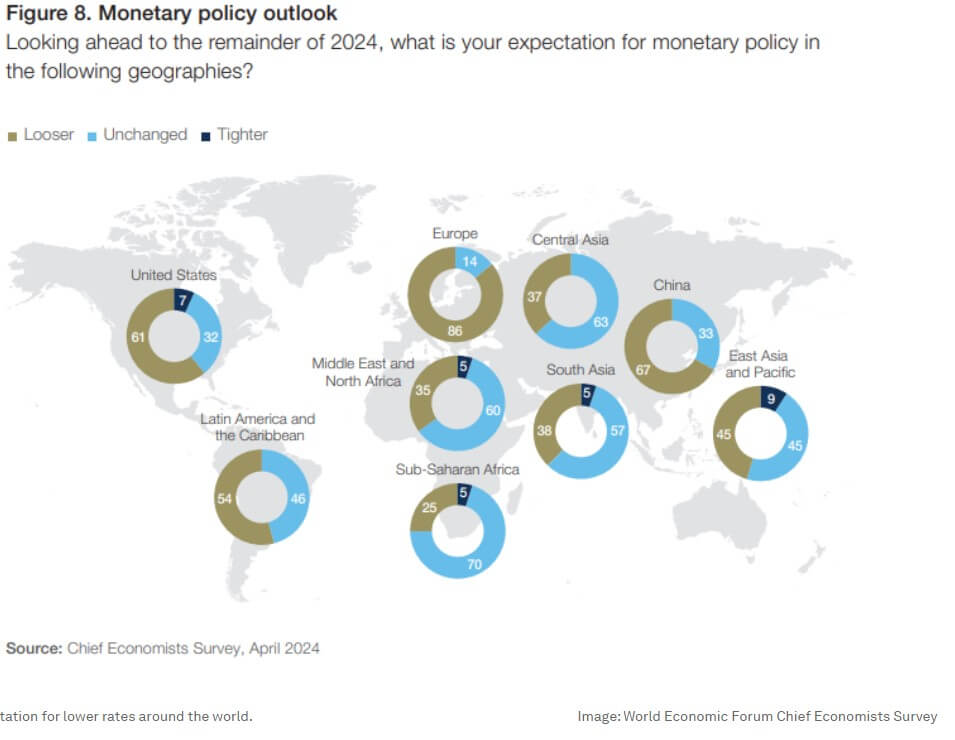

Während der genaue Zeitpunkt und das Tempo künftiger Zinsanpassungen von den kommenden Wirtschaftsdaten abhängen, besteht unter den politischen Entscheidungsträgern Einigkeit darüber, dass eine schrittweise Lockerung der Geldpolitik jetzt angebracht ist. Dieser Kurswechsel dürfte das Wirtschaftswachstum ankurbeln und den Druck auf Unternehmen und Verbraucher etwas verringern.

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

LG Ben&Deniz

Shabbat Shalom

07/18/2024, Monetary Policy Decision of the ECB (Key Interest Rate: 4.25% +/- 0.0)

07/18/2024, Monetary Policy Decision of the ECB (Key Interest Rate: 4.25% +/- 0.0)

07/24/2024, Monetary Policy Decision of the BoC (Key Interest Rate: 4.50% – 0.25)

07/31/2024, Monetary Policy Decision of the BoJ (Key Interest Rate: 0.25% + 0.15)

07/31/2024, Monetary Policy Decision of the FED (Key Interest Rate: 5.50% +/- 0.0)

08/01/2024, Monetary Policy Decision of the BoE (Key Interest Rate: 5.00% – 0.25)

08/06/2024, Monetary Policy Decision of the RBoA (Key Interest Rate: 4.35% +/- 0.0)

08/22nd to 08/24th Jackson Hole Economic Symposium

1. ECB Monetary Policy Decision on 18 July 2024

On 18 July 2024, the European Central Bank (ECB) opted to keep its interest rates unchanged, reflecting its cautious approach amid the challenges posed by slowing economic growth in the Eurozone. Despite persistent inflationary pressures, the ECB’s decision was seen as a balance between controlling inflation and supporting the economy. This move helped the Euro gain strength, particularly against the US Dollar, as markets anticipated that the FED might lean towards a more dovish stance in the coming months.

2. Bank of Canada Rate Cut on 24 July 2024

On 24 July 2024, the Bank of Canada (BoC) reduced its key interest rate by 25 basis points to 4.50%. This decision was motivated by concerns about the Canadian economy’s slowdown and the negative impact of a strong Canadian Dollar on exports. The rate cut, while widely anticipated, resulted in a brief weakening of the Canadian Dollar. However, the currency quickly regained some ground as the market recalibrated its expectations for the BoC’s future monetary policy direction. The USD/CAD pair experienced heightened volatility as traders responded to the rate cut and its broader economic implications.

3. Bank of Japan’s Rate Hike on 31 July 2024

The Bank of Japan (BoJ) increased its benchmark interest rate from 0.10% to 0.25% on 31 July 2024. This move marked a continuation of the BoJ’s gradual shift away from its previous ultra-loose monetary policy, which had already begun with earlier rate hikes moving out of negative territory. The decision was driven by rising domestic inflation and the need to stabilize the Yen, which had been weakening significantly. This rate hike was largely anticipated, given the recent economic data pointing to higher inflation. Following the announcement, the Japanese Yen strengthened considerably against the US Dollar, causing the USD/JPY pair to decline sharply. The decision also led to a reevaluation of carry trades, increasing market volatility.

4. Federal Reserve’s Rate Hold on 31 July 2024

On 31 July 2024, the Federal Reserve decided to maintain its key interest rate at 5.50%, following a series of rate hikes aimed at combating inflation, which has now stabilized around 2.9%. The decision to hold rates steady was widely expected, reflecting the Fed’s cautious stance while remaining open to future adjustments if necessary. The US Dollar continued to weaken after the announcement, as speculation grew over potential rate cuts in the future. This dovish outlook contributed to a broad decline in the USD, particularly against the Yen and the Euro.

5. Bank of England’s Rate Cut on 1 August 2024

The Bank of England (BoE) cut its benchmark interest rate from 5.25% to 5.00% on 1 August 2024, citing concerns about slowing economic growth and a softening labor market. Despite inflation remaining above target, the rate cut was deemed necessary to support the UK economy amid rising global uncertainties. The British Pound initially fell sharply against the US Dollar and the Euro following the announcement but later recovered some losses as markets debated whether this cut would be a one-off event or signal the beginning of a more prolonged easing cycle. The GBP/USD pair experienced significant fluctuations as the implications of the BoE’s decision were absorbed by the market.

6. Reserve Bank of Australia’s Rate Hold on 6 August 2024

On 6 August 2024, the Reserve Bank of Australia (RBA) decided to keep its cash rate at 4.35%. The RBA’s decision reflected a cautious approach amid mixed economic signals, particularly weak consumer spending and a fragile housing market, despite ongoing inflation concerns. The Australian Dollar saw limited immediate movement following the announcement, but it later strengthened due to rising commodity prices and improved market sentiment. The AUD/USD pair remained relatively stable, with brief periods of volatility as traders assessed the RBA’s policy outlook.

Currency Pair

Latest Trends (Post-18 July 2024)

USD/JPY

Significant decline, high volatility

EUR/USD

Strengthened Euro, weak USD

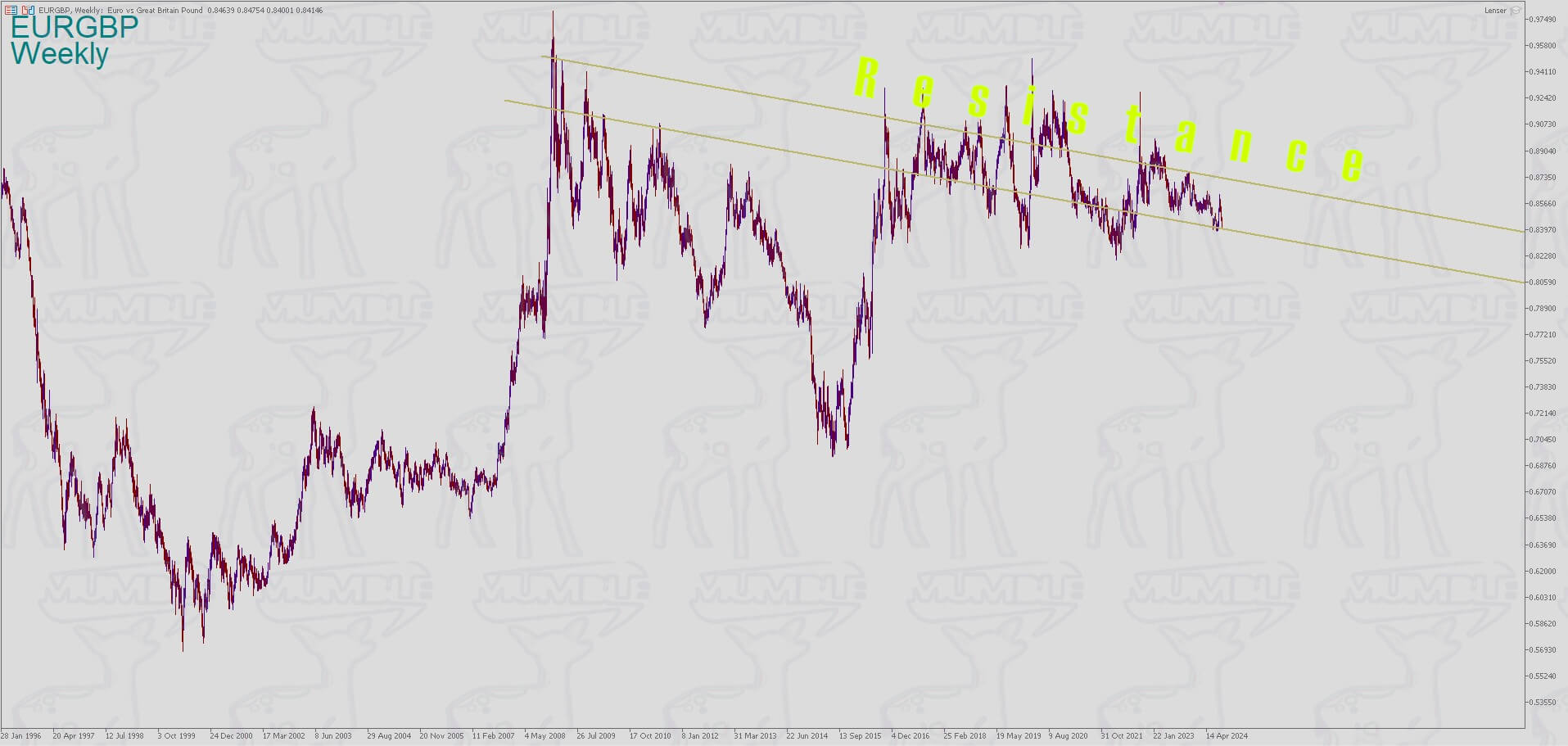

GBP/USD

Exceeded expectations; underlying surveys suggest slower economic momentum

USD/CAD

Remains restrictive until inflation risks diminish; MPC monitoring closely

AUD/USD

Prepared to adjust policy based on upcoming economic data and forecasts

World Economic Forum @Jackson Hole, Wyoming

Federal Reserve Chair Jerome Powell, in his highly anticipated speech, declared that the time has come for policy to adjust, indicating a growing confidence in the trajectory of inflation. This dovish pivot from the Fed chair was echoed by other major central banks, such as the Bank of England and the European Central Bank.

While the exact timing and pace of future rate adjustments will depend on incoming economic data, the consensus among policymakers is that a gradual easing of monetary policy is now appropriate. This shift is expected to provide a boost to economic growth and alleviate some of the pressures on businesses and consumers.

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben&Deniz

Economic Calendar July

Economic Calendar August

World Economic Forum Rates Outlook

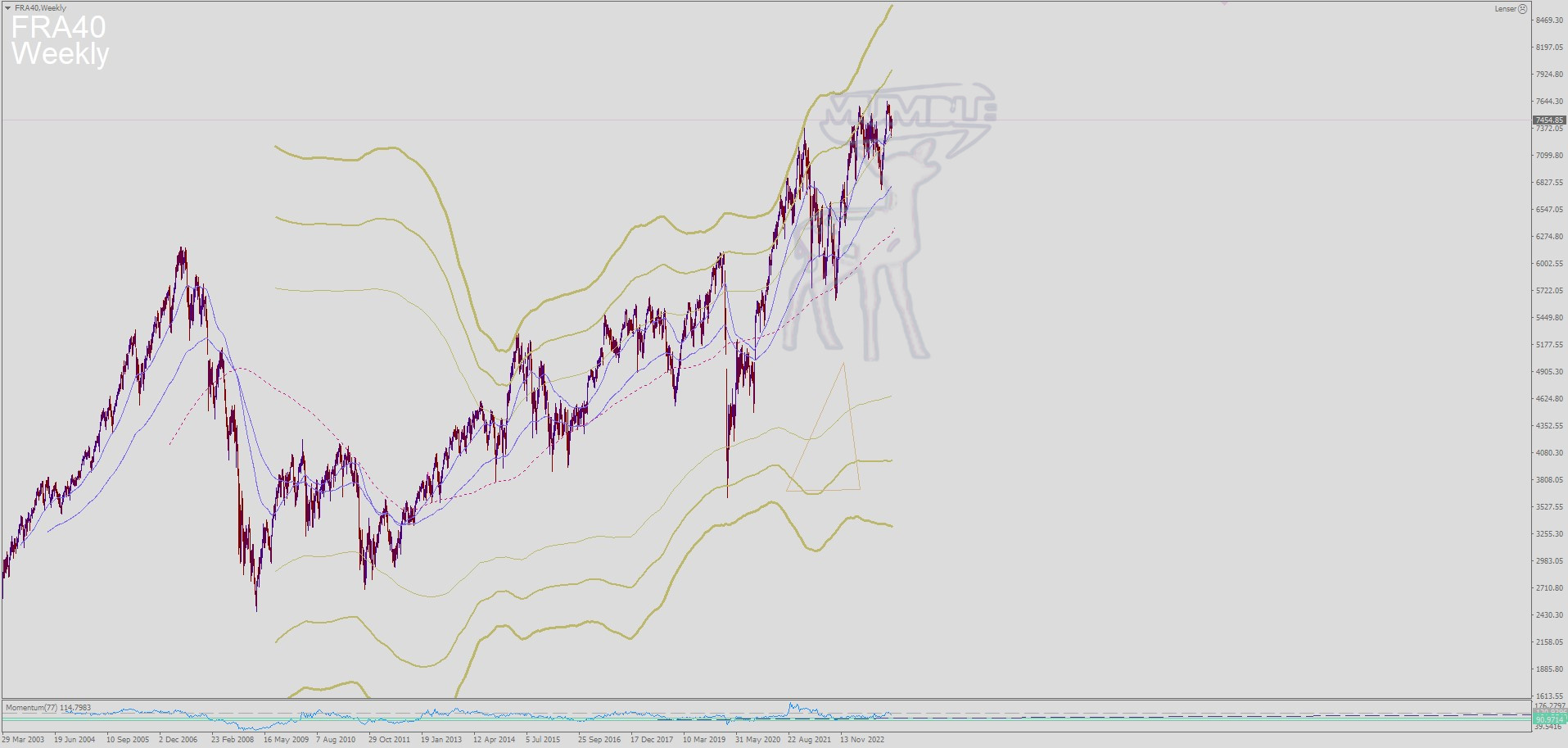

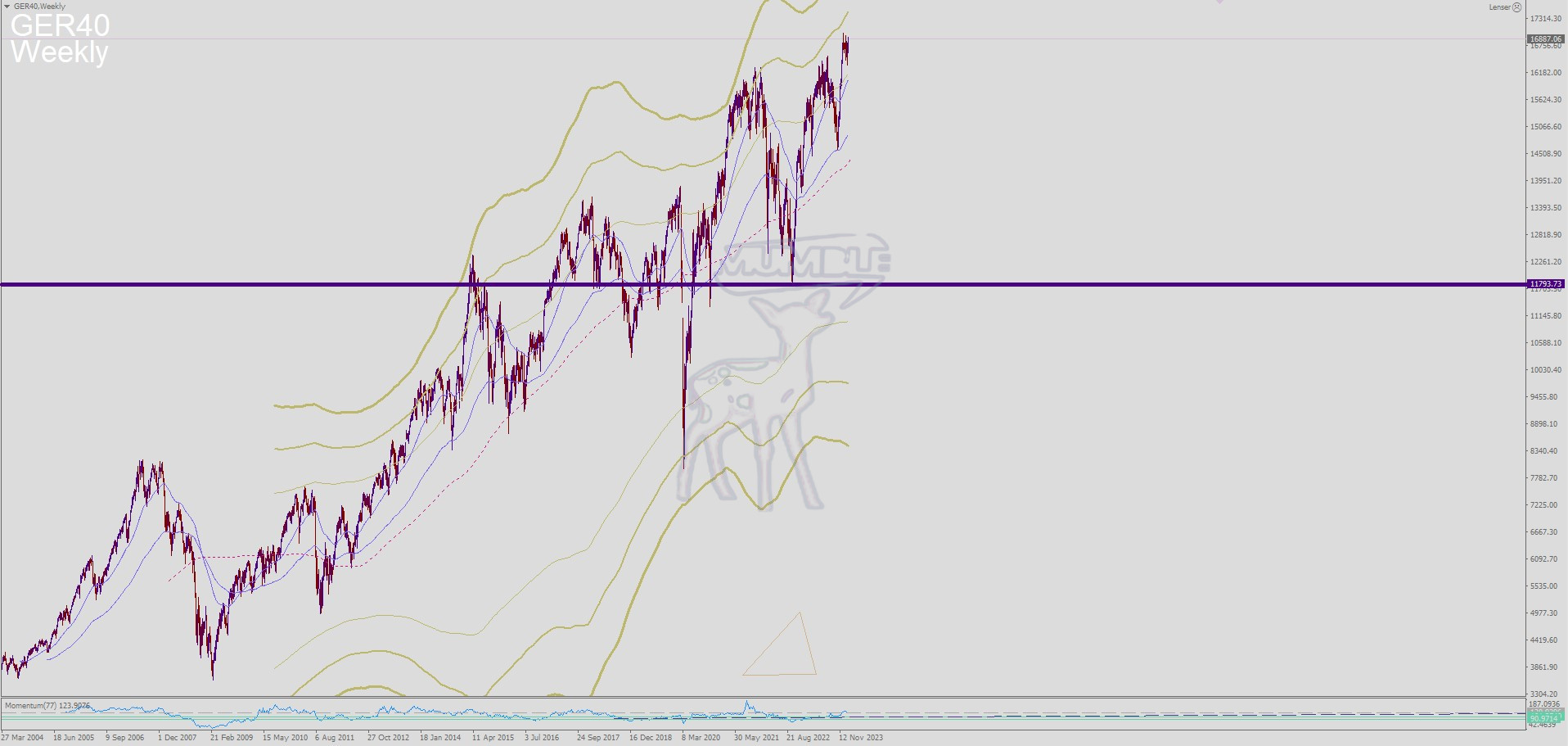

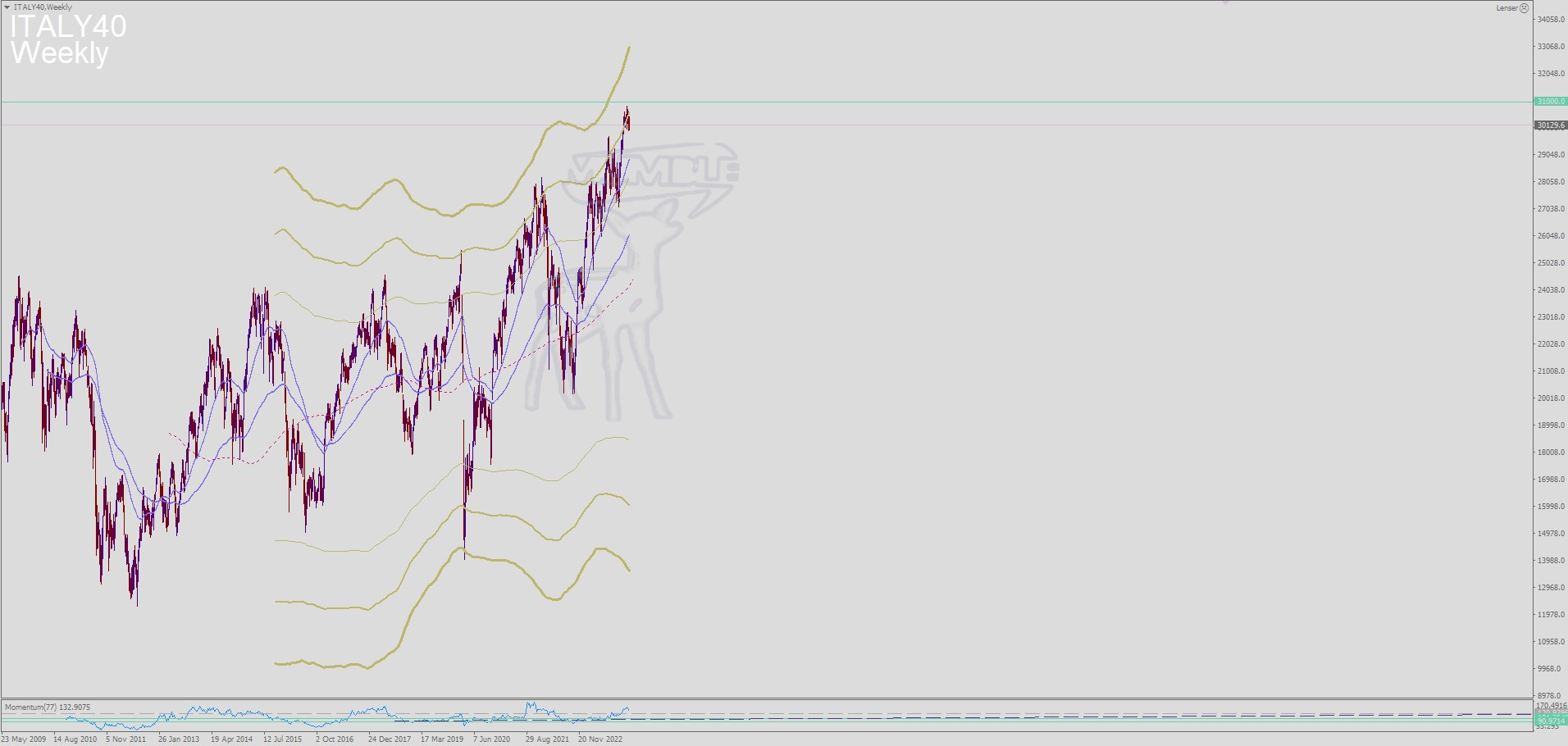

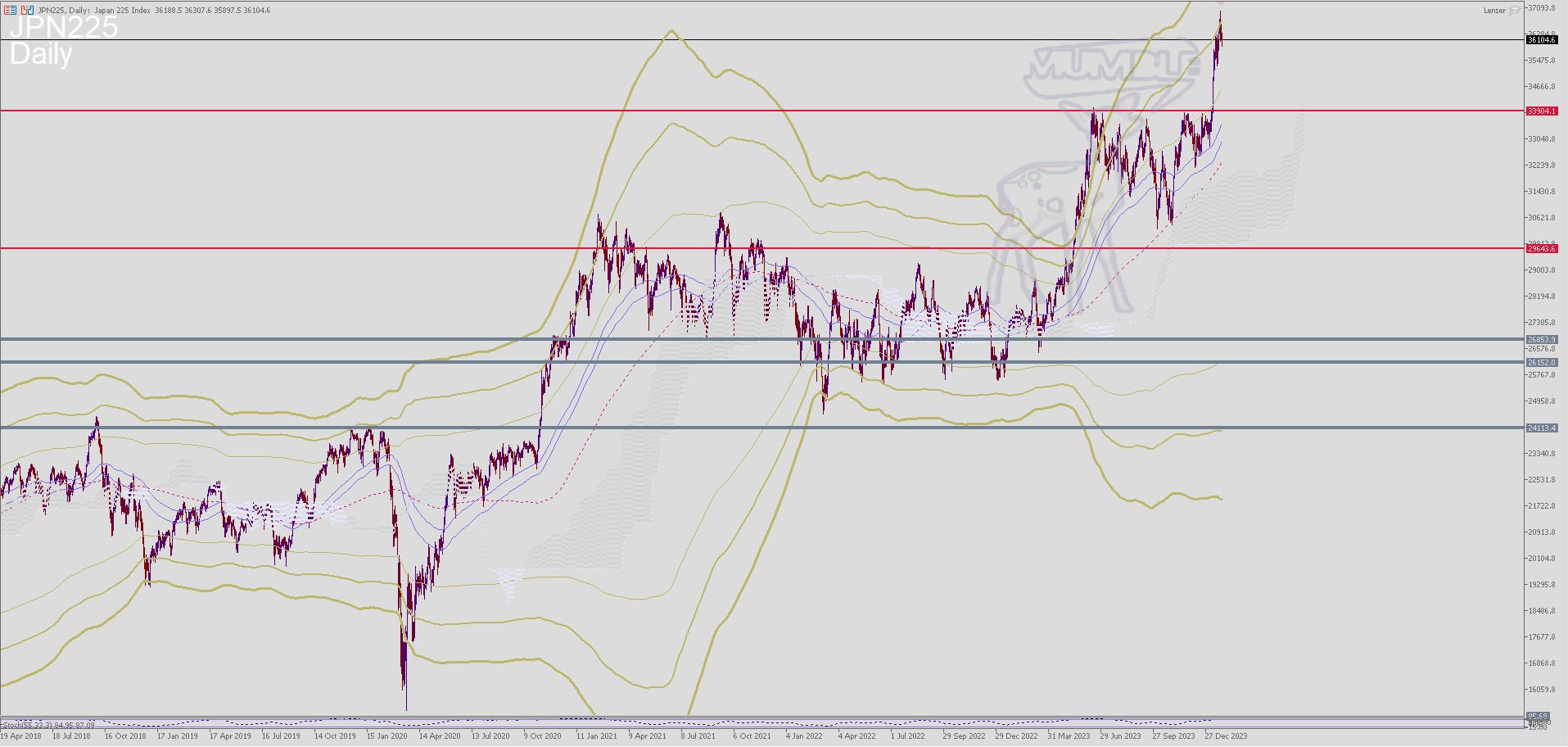

EURUSD Weekly Chart

EURGBP Weekly Chart

Gold Weekly Chart

Broadcasted by: ClearValue Tax

Externe Quellen/Links