2023-05-27: „Ich werde bis Ende Mai einige Updates auf MumbleFX einspielen. Die Seite wird vorübergehend auf „Maintainance“ gesetzt und damit nicht erreichbar sein.“

Super sorry, weil es einige weitere technische Hürden zu meistern galt… Der Server musste komplett neu aufgesetzt und alle Daten aufgespielt werden.

Zur Marktsituation schreibe ich erst ab Wochenende wieder, dann ausführlicher. Top-Themen sind der Nikkei, Rate-Hike-Cycle Pause (wahrscheinlich ab heute Abend!), ultra-Low VIX-Daily und der freie Fall der türkischen Lira.

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

Ben

Goody Traders

2023-05-27: „I’ll be rolling out some updates to MumbleFX by the end of May. The page will be temporarily set to „Maintenance“ and will therefore not be accessible.“

Super sorry, because there were a few more technical hurdles to overcome… The server had to be set up from scratch and all data uploaded.

I won’t write about the market situation until the weekend, but then in more detail. Top themes are the Nikkei, rate-hike-cycle pause (probably this evening!), VIX ultra low reading and the free fall of the Turkish lira.

More details and my outlook on the FX Exchange as always for Premium Members.

Guten Morgen,

03-Mai-2023, die Federal Reserve erhöht ihren Leitzinssatz um 25 Basispunkte auf 5.25%.

Eine prekäre Situation für die Weltwirtschaft, erstens? Einerseits treiben Inflation und inverte Yieldkurven das Schreckgespenst namens „Rezession“ um die Hochhausblöcke, andererseits war doch gerade ein gigantisches Quantitative Easing der Garant für die „financial market resilience“. Geht nebenher eine US-Bank den Bach runter, die kalifornische Silicon Valley Bank, so sieht man die FED mit dem Rücken zur Wand.

Was aber ist der Grund für den Kollaps der hiesigen Tech-Family, deren Einlagen im Zuge der Covid-Abwehrmaßnahmen von $60 Milliarden in 2020 auf $200 Milliarden in 2022 angesprungen waren? Start-Ups, und besonders Crypto und Marihuana Unternehmen, wurden mittels SPACs (Special Purpose Acquisition Company) ins Leben gerufen, noch bevor diese überhaupt existierten. Ja! Genau richtig gelesen! Zuerst wird Geld gesammelt – fund raising – um sich im Anschluss daran Gedanken zu machen, welch ein Unternehmen man damit gründen könnte. Glaubst Du wirklich, die hippen Kalifornier kaufen mit ihren Milliarden einfach nur US-Treasuries und Mortgage-Backed Securities? Crypto, Crypto, Tech-SS und Jungspund-Crypto sind der Grund für ein maßloses Risiko in ein Asset, mittels die Tech-Familie den US-Dollar und alle übrigen Währungen der Welt aushebeln wollen. Dieses Risiko hat sich nun selbst herausgekürzt, nebst der Crypto-Bank „Silvergate“. Anmerkung: Kursverluste können über ein geeignetes Unternehmen steuerlich abgesetzt werden :Anmerkung Ende.

Aus Sicht der kapitalistischen Eliten rund um die Zentralbanken, hat sich der Schimmel am Kuchen selbst abgeschnitten. Ein doppelter Beleg für die gesunde Funktionalität der Finanzmärkte.

04-Mai-2023, die ECB erhöht ihren Leitzins um 25 Basispunkte auf 3.75%. Ein historischer Anstieg des Leitzinssatz, was auf die andauernd hohen Inflationswerte zurückzuführen ist.

Eine Gefahr für die Märkte, zweitens?

Das Geld ist zwar aus den Büchern der Zentralbanken, die gigantischen QE-Programme aber haben derart viel Kapital in Umlauf gebracht, was in dem Zeitraum zuvor 1/4 Jahrhundert gedauert hatte. Dieses Geld steht bereit, im Kontrast zu Situationen mit Inverten-Yieldkurven vorangegangener Marktsituationen, um jedweden Börsen-Dip aufzukaufen. Die reale Aufhängung lautet: Unternehmen sind die Speerspitze des kapitalistischen Paradigmas, ermöglichen Arbeitsplätze, Konsum und Umsatz. Diese Unternehmen werden mit Geldern aus Hedge-Fonds umspült, welche Klienten Regierungen von Hammerfest bis Kapstadt unterhalten. Regierungen erhalten ihre Mittel über Anleihen, welche die Zentralbanken nun aufgekauft haben. Darüber hinaus, selbstverständlich von der bürgerlichen Wählerschaft, welche ihre Arbeitsplätze gesichert sehen möchten.

Wo den nun exakt eine Gefahr für die Märkte bestehen soll, wenn nicht für die Vermögensmacht der unangefochtenen Kolonialstaaten, kann niemand numerisch genau bestimmen. Die Wurzeln der Macht reichen tief und die smartesten Leute schützen eben genau diese Valuta. Zwei Weltkriege sind von den Börsen der Welt absorbiert worden. Es wäre wenn denn gesetzten Falles, eine Transformation in Nullzeit hin zu einer Gift- und Green-Culture, eine hübsche Vision, deren Realität nur Schritt für Schritt erreicht werden kann.

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

Bünny

Goody Traders,

03-May-2023, the Federal Reserve raises its key interest rate by 25 basis points to 5.25%.

A precarious situation for the world economy? On the one hand, inflation and inverted yield curves are driving the specter of „recession“ around the skyscrapers, on the other hand, gigantic quantitative easing was the guarantor of „financial market resilience“. If a US bank goes down the drain at the same time, the Californian Silicon Valley Bank, you see the FED with its back to the wall.

But what is the reason for the collapse of the „Kali“ tech family, whose deposits had jumped from $60 billion in 2020 to $200 billion in 2022 in the course of the Covid defense measures? Start-ups, and especially crypto and marijuana companies, were created by SPACs (Special Purpose Acquisition Company) before they even existed. Yes! You read that right! First, money is collected – fund raising – in order to then think about what kind of company one could create with it. Do you really think hip Californians just buy US Treasuries and Mortgage-Backed Securities with their billions? Crypto, Crypto, Tech-SS (Waffen-SS, SA) and Nazi-Youth-Crypto are the reason for excessive risk in an asset, with which the tech family want to superseed the US dollar and all other currencies in the world. This risk has now reduced itself, along with the crypto bank „Silvergate“. Note: Exchange rate losses can be deducted for tax purposes via an appropriate company : end of note.

From the point of view of the capitalist elites surrounding the central banks, the mold has cut itself off teh cake. A double proof of the healthy functioning of the financial markets.

04-May-2023, the ECB increases its key interest rate by 25 basis points to 3.75%.

A historic increase in the key interest rate, which is due to persistently high levels of inflation.

A threat to the markets? The money is off the central banks‘ books, but the gigantic QE programs have pumped in so much capital that previously took 1/4 century to create. This money stands ready, in contrast to inverted yield curve situations of previous market situations, to buy any stock market dip. The real suspension is: companies are the spearhead of the capitalist paradigm, enabling jobs, consumption and turnover. These companies are being showered with money from hedge funds whose clients are governments from Hammerfest to Cape Town. Governments get their funds from their own bonds issued, which central banks have now bought up. In addition, of course, by the bourgeois electorate, who want to see their jobs secured.

Exactly where there is a danger for the markets, if not for the wealth power of the undisputed colonial states, nobody can precisely determine numerically. The roots of power run deep and the smartest people protect that very realm. Two world wars have been absorbed by the stock markets of the international community. If any revolution, it would be a zero-time transformation towards a gift and green culture, a pretty vision whose reality can only be achieved step by step.

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben&Nic

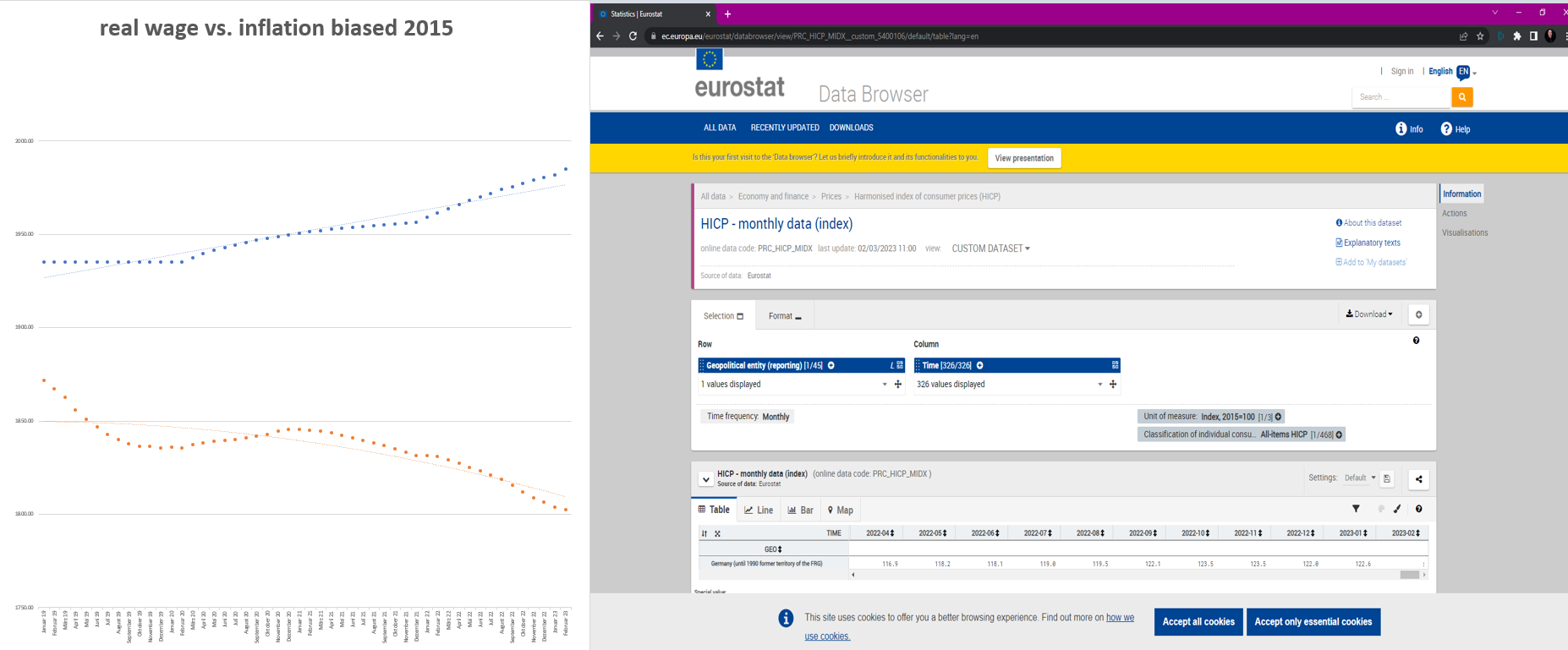

Schweizer Franken IndexInflation Biased 2015 – Beispielrechnung

Guten Abend,

22-März-2023 die FED erhöht ihren Leitzinssatz um weitere 25 Basispunkte auf nunmehr 6.00%.

Ein sehr starkes, souveränes Signal des Federal Reserve Board, rund um den Vorsitz von Jay Powell, man differenziert und überschaut die Gesamtsituation. Die Silicon Valley war prozentual eine äußerst schwach aufgestellte Bank, in Hinblick auf die Eigenkapitalquote.(transcript)

Das zweitvorangige Ziel der maximalen Beschäftigung bleibt weiter im grünen Bereich. So gibt es derzeit in den USA einen Arbeitskräftemangel und chronische Vakanzen. Die Inflation bleibt weiter erhöht, welche nun mehr und mehr eine eigene Dynamik aufzeigt. Es ist „chic“, den Kaffee mit 3,70 zu berappen, da bei 2,80 das Prestige des Gehobenen nicht gegeben ist. Eine Art Abschottungsspirale jener Anteile in unserer Wirtschaft, deren Klientel gerne exklusive Preise bezahlt. So wird es auf ansehbare Zeit keine wirkliche Inflationsabschwächung geben, wenn nicht auch die Löhne steigen oder was seltener vorkommt, die Preise sinken.

Wir sehen die Löhne stagnieren, wärend die Inflation weiter ihre Kreise zieht. Erst wenn der Konsum anfängt zu stagnieren, müssen die Löhne steigen um den Konsum wieder an zu kurbeln. Oder es kommt zu sogenannten Boni-Programmen – Verschrottungsprämien, Zulagen und Förderprogramme -, welche letzlich von jenen mitbezahlt werden müssen, die Steuern abführen.

Bei der Betrachtung der Inflation hat ein einfacher Vergleich mit dem Vormonat oder dem Vorjahr ausgedient. Was wir sehen müssen, ist die Lohnentwicklung relativ zur Inflation ab einem bestimmten Jahr, z.B. 2015 (Bias). Ich habe den Harmonized Index of Consumer Prices der ECB als Grundlage genommen, um zu verdeutlichen, dass Inflation nicht stehen bleibt, wenn sich die Jahr zu Jahr Vergleichsrechnung um die 2% Inflation einzupendeln wüsste. Tatasächlich sinkt die Kaufkraft der Haushalte stetig, wenn die Löhne nicht angepasst werden.

Der sFr. hat über das FX-Board gesehen einen etwas durchwachsenen Eindruck hinterlassen. Gegen die Majors USD, EUR, GBP, JPY hatte im Zuge des Bailouts der Credit Suisse der Franken zunächst Federn lassen müssen. Nur ein Blick auf den Index zeigt uns, dass sich die Währung insgesamt berappen konnte.

Die magische „amble liquidity“ scheint auch dieses mal jeden Zweifel an den Finanzeliten ausmerzen zu können. Aber bedeutet das nicht auch, das mit einer Bankenlizenz – ab 5 Millionen – praktisch jeder machen kann was er will, denn ja eine Zentralbank würde die Zeche zahlen müssen, damit keine Bankkunden abfliessen?

Weitere Details und Ausblick auf den Exchange wie immer für Premium-Mitglieder.

Bünyamin

Goody Traders,

22-March-2023 the FED raises its key interest rate by another 25 basis points to 6.00%.

A very strong, sovereign signal from the Federal Reserve Board, around the chairmanship of Jay Powell, one differentiates and oversees the overall situation. Silicon Valley was an extremely underperforming bank in percentage terms of equity ratio.(transcript)

The second upper most priority target of maximum employment remains in the green. There is currently a labor shortage and chronic vacancies in the USA. Inflation remains elevated, which is now more and more showing its own dynamic. It’s „chic“ to shell out 3.70 for the coffee, since 2.80 doesn’t have the prestige of being upscale. A kind of isolation spiral for those parts of our economy whose clientele likes to pay exclusive prices. So there will be no real slowdown in inflation for the foreseeable future unless wages also rise or, more rarely, prices would fall.

We see wages stagnate while inflation continues to nudge the shelf. Only when consumption begins to stagnate do wages have to rise in order to stimulate consumption again. Or there are so-called bonus programs – scrapping premiums, allowances and support programs – which ultimately have to be paid by the taxpayer.

When looking at inflation, a simple comparison with the previous month or the previous year has had its day. What we need to see is the wage development relative to inflation from a certain year, e.g. 2015 (bias). I used the ECB’s Harmonized Index of Consumer Prices as a basis to illustrate that inflation does not stand still if the year-to-year comparison were to settle around 2% inflation. In fact, purchasing power of households falls steadily if wages are not adjusted.

The sFr. left a somewhat mixed impression over the FX board. Against the majors USD, EUR, GBP, JPY, the Swiss franc initially had to give up feathers in the course of the Credit Suisse bailout. Just looking at the index shows us that the currency as a whole managed to shell out.

The magical „amble liquidity“ seems to be able to eradicate any doubts about the financial elites this time as well. But doesn’t that also mean that with a banking license – from 5 million – practically anyone can do whatever they want, because a central bank would have to foot the bill so that no bank customers flow away?

More details and exchange outlook as always for Premium -Members.

Sincerely Yours, Ben

Guten Morgen,

01-Februar-2023, die Federal Reserve erhöht den Leitzinssatz für den US-Dollar um 0.25% auf nunmehr 4.75%. Damit reduziert Powell die Geschwindigkeit der Rate-Hikes seit dem Dezember-Meeting deutlich. Von 50 Basispunkten 14-Dezember-2023 auf aktuell 25 Basispunkte.

Das Hauptaugenmerk liegt in der Betrachtung des durchschnittlichen Konsumenten-Ausgaben-Index (Headline PCE). Dieser selektiert die zu kalkulierenden Waren und Dienstleistungen nach dem aktuellen Kaufverhalten der Konsumenten und exkludiert Nahrungsmittel sowie Energiekosten. Auch die Anzahl der Items, die zur Berechnung herangezogen werden, ist deutlich größer als bei der Kerninflation (CPI). Wenn dem Konsumenten Produkt bzw. Dienstleistung A zu teuer wird, dann wechselt er sein Kaufverhalten (Produkt bzw. Dienstleistung B). Dieses sich verändernde Kauf- bzw. Konsumverhalten spiegelt die Adaption des Konsumenten an die inflationären Bedingungen des Realmarktes.

Daher ist die Headline-PCE immer niedriger als die Kerninflation (Core Consumer Prices). Ungeachtet der Betrachtung der US-Inflation, kommt Powell zu dem Schluss, dass die Inflation trotz einer akkommodativen geldpolitischen Straffung, signifikant von seinem 2%-Ziel abweicht. Powell betonte jedoch, dass alles Nötige getan wird, um schnell das Inflationsziel von 2% zu erreichen.

Lagarde, Vorsitzende der EZB und Andrew Bailey von der Bank of England erhöhten am 02-Februar-2023, jeweils um 50 Basispunkte.

Damit bezahlt man für den Euro 3% und für den britischen Pfund nunmehr 4%.

Dashboard-EA by MumbleFX wird bereits von einem eigenen Server betrieben. Klienten haben die Möglichkeit, ihr MT4/5-Terminal auf diesem Server zu betreiben. Dashboard-EA ist ein Hybrid aus Webinterface, MetaTrader (MQL) Software und Excel. Datenbank-Schnittstellen laufen einmal direkt über MQL und zum anderen via Webinterface. MariaDB und die MQL-SQL sind voneinander unabhängig und speichern die Daten aus unterschiedlichen Bereichen. Die MQL-SQL z.B. speichert direkt kursrelevante Daten zur Berechnung der „Schwimmblase“. Mit der zweiten Datenbank werden alle peripheren Informationen erfasst, welche nur indirekt für das Trading genutzt werden, wie z.B. Broker und Makro-Finanzdaten.

Weitere Details und Ausblick auf den Exchange wie immer für Premium-Mitglieder.

Bünyamin

Goody Traders,

01-February-2023, the Federal Reserve raises the base interest rate for the US dollar by 0.25% to 4.75%. Powell has thus significantly reduced the speed of rate hikes since the December meeting. From 50 basis points 14-December-2023 to currently 25 basis points.

The main focus is on the average consumer expenditure index (Headline PCE). This selects the goods and services to be calculated according to the current purchasing behavior of the consumer and excludes food and energy. The number of items used for the calculation is also significantly larger than when looking at core inflation (core consumer prices). If product or service A becomes too expensive for the consumer, then he changes his purchasing behavior (product or service B). This changing purchasing and consumer behavior reflects the consumer’s adaptation to the inflationary conditions of the real market.

Therefore, the headline PCE is always lower than the core inflation (Core Consumer Prices). Pointing to all data available, Powell concludes that despite accommodative monetary tightening, inflation deviates significantly from his 2% target. However, Powell stressed that whatever is necessary is being done to quickly reach the 2% inflation target.

ECB Chair Christine Lagarde and Bank of England’s Andrew Bailey hiked 50 basis points each on 02-Feb-2023.

This means that you pay 3% for the euro and 4% for the British pound.

Dashboard-EA by MumbleFX is already operated by its own server. Clients have the option to run their MT4/5 terminal on this server. Dashboard EA is a hybrid of web interface, MetaTrader (MQL) software and Excel (I know, ressource hungry). Database interfaces run directly via MQL and via web interface. MariaDB and the MQL-SQL are independent of each other and store the data from different areas. The MQL-SQL e.g. directly saves price-relevant data for the calculation of the „swimming bladder“. The second database captures all peripheral information that’s only indirectly relevant to trading and market activity, such as broker-forecasts (social trading) and macro financial data.

More details and my outlook on the Foreign Exchange as always for Premium Members.

Sincerely Yours, Ben

Kaffee&Kuchen Sonntag,

die FED hiked um 50 Basispunkte auf 4.5%. Powell stellt in der folgenden Pressekonferenz klar, dass es bei den derzeitigen Debatten um die Geschwindigkeit der Leitzinsänderungen gehe und man bislang nicht die Dauer als Hauptvariable betrachte.

Das Inflationsziel läge zwei Jahre in der Zukunft, so also sähe man im Jahr 2025 den Leitzinssatz bei knapp über 5.0%. Neben der Geldpolitischen Straffung mittels des Leitzinssatzes, ist des Weiteren eine Verknappung des Geldumlaufs durch eine Reduktion des Balance-Sheet vorgesehen.

Auf der geldpolitischen Lagebeurteilung vom 15. Dezember 2022 gab der SNB-Vorstandsstab rund um Thomas Jordan, eine weitere Leitzinsanhebung um 50 Basispunkte auf nunmehr 1% bekannt.

Herr Martin Schlegel von der SNB berichtet von einer sinkenden Nachfrage nach Bargeldnoten hoher Stückelung, wie die der 200- und 1000-er sFr. Geldscheine. Diese seien in Zeiten von Krisen besonders gefragt und gerade in den zurückliegenden Jahren, bedingt durch die Finanzkrise, Covid-Pandemie und Inflationsängsten überdurchschnittliche stark nachgefragt. So führt Herr Schlegel aus, dass seit der Finanzkrise 2008 bis heute der Bargeldumlauf des Franken mehr als doppelt so stark gestiegen sei, als wie dies die zwei vorhergehenden Jahrzehnte der Fall gewesen war. Die nun sinkende Nachfrage sieht die SNB in der steigenden „Bonus“-Verzinsung von Geldeinlagen begründet.

Dahinzu führe auch der nun erhöhte Leitzinssatz in der Schweiz und andernorts zu einer merklichen Eindämmung der Inflationsspirale. Nicht nur Thomas Jordan weist ausdrücklich auf die Gefahr eine Lohn-Preisspirale hin, sondern in der Folge auch der Vorsitz der britischen Zentralbank, Andrew Bailey.

Andrew wiederum erhöht, ebenfalls am 15. Dezember, 50 Basispunkte auf nunmehr 3.50%, wobei er offenkundige Andeutungen in Hinblick der Finanz-Krise auf dem britischen Bondmarkt macht.

Die Rede ist von „pooled“-Funds, so genannte Ableger der „resilient“-Funds und Banken, welche mit zu hohem Risiko und unbesicherten Assets handeln würden. Die voran benannten Valuta betreffen weniger als 20% der in dieser Sparte gehandelten Instrumente, aber dies hatte ausgereicht, um die Turbulenzen am britischen Bondmarkt zu begründen.

Es seien laut Bailey regulatorische Maßnahmen in Arbeit, um die Finanzmarkt-Stabilität in den betreffenden Bereichen zu erhöhen. Das „Bread for Death“, ein sarkastischer Bankerjargon für äußerst hoch gehebelte Finanzprodukte, würde zunehmend zu einer Gefahr auf den globalen Finanzmärkten. Bailey notiert aber, umfassende regulatorische Maßnahmen würden von „slow moving animals“, also den langsamen gesetzgebenden Mühlen durchgesetzt. Somit werden diese (regulatorischen Maßnahmen) sich erst zeitlich verzögert bemerkbar machen. In Hinblick auf nicht regulierte Märkte außerhalb des Bankensektors bezeichnete er explizit „Crypto-Assets“ als einen Risikomarkt. Ein Investment in Crypto-Assets, würde eine hohe Bereitschaft Verluste hinzunehmen voraussetzen.

Christine Lagarde, Vorsitzende der europäischen Zentralbank wehrte sich bei der Bekanntgabe der nächsten Leitzinserhöhung um 50 Basispunkte (aktuell 2.5%) gegen ein „Pivotieren“ im Schatten der Federal Reserve. Man habe im Gegensatz zu den USA (und Japan) unverhältnismäßig mehr Spielraum, um die Preisstabilität in die gewünschte Bandbreite zu navigieren.

Christines‘ Brosche stellt kein F-Tilte dar (sonderbarer Humor), mag dagegen Zeichen einer Zivilisation auf Harok sein (Harokaner verehren das Licht als heilig).

Die Akzeptanz und Verbreitung des US-Dollars ist prinzipiell auf ein übermächtiges Militär zurückzuführen. Die hyperinflationäre Bilanz der Japaner ließe sich auf einen strikten, despotischen Banken-Keynesianismus reduzieren.

Das Credo des europäischen Staatenbundes, „Nie wieder Krieg auf europäischem Boden“, verpflichtet die derzeit stärksten und am weitesten entwickelten Demokratien der Welt, Vorbild zu sein. Europa möchte so weit, wie bei Betrachtung seiner geschichtlichen Verantwortung möglich, mithilfe von Diplomatie Frieden und die soziale Marktwirtschaft stärken.

Italien verhindert eine europäische Bankenunion. Christine fordert von der italienischen Regierung eine rasche Aufgabe ihrer Blockade entgegen der Ratifizierung einer EU-Bankenunion. Italien aber, inmitten eines politischen Irrflugs in dünner Luft (Bankenwesen, Staatsverschuldung, provisorische Regierungen), gärt gerade etwas Größeres aus. Italien bandelt mit den Chinesen und profitiert von einer Art Seidenstraße über das Mittelmeer. Ein Containerhafen bezahlt und realisiert durch chinesische Firmen auf italienischem Territorium, ist ursächlich dem erstarkenden Neofaschismus, dem italienischen Nationalismus 2.Grades. Auch die USA mittels voran dem Privatgeheimdienst „Stratfor“, sieht keinen Segen in einem geeinten Europa. Man verlässt sich doch lieber auf handhabbare Einzelstaaten im unterstellten NATO-Verbund.

Eine weitere Größe macht die Italiener zum Feind der EU-Bankenunion. Der französische Präsident Emmanuel Macron sieht zusammen mit dem ehemaligen ECB-Vorsitz und italienischen Interim-Präsidenten, Mario Draghi, die Neuverschuldungsgrenze als obsolet an.

Dieser Kakophonie nicht genug, ereignen sich wichtige Ereignisse auf südamerikanischem Boden. Der peruanische Präsident, Pedro Castillo sitzt in U-Haft. Nach seiner Amtsenthebung wegen Hochverrats fordert die Bevölkerung mit Demonstrationen und Protesten seine Freilassung und vorgezogene Neuwahlen. Es ist eine gefährliche Situation für die Demonstranten, so sieht es nach dem Protokoll aus, als würden sie nicht ihre Demokratie verteidigen, sondern im Gegenteil gar versuchen, diese zu putschen.

Ein solches Wirrwarr, ein demokratisches „False/True“, ist womöglich von der Opposition beabsichtigt, um die Bevölkerung legitimerweise mit Notstandsgesetzen unter Kontrolle bringen zu dürfen. Die Lage der peruanischen Arbeiterschaft wird womöglich nicht von der Situation in Ost-Europa zu trennen sein. Sogenannte „Kaviar-Linke“ sehen diese Entwicklungen mitunter als Rechtfertigung ihrer eigenen geostrategischen Zielbilder. Die Systemfrage wird gerade wieder salonfähig.

Entschuldige diesen Umschweif in die Welt der Politik und Parteilichkeit, aber ich denke an dieser Stelle für den ein oder die andere ein nötiger „Denkanstoß“, eine willkommene Denkpause vom Facility Deposit Rate Finanz Data Crunching.

Und nein, ein höherer Leitzins bedeutet nicht automatisch (sondern gar widersprüchlich) eine höhere Bonusverzinsung! Ein höherer Einlagenzins soll Gelder im Umlauf (auf Bankkonten) binden und somit die Inflation mittelfristig untergraben.

Weitere Details und Ausblick auf den Exchange wie immer für Premium-Mitglieder.

Bünyamin

Goody Traders,

On December 14-2022, the Fed raised interest rates by 50 basis points to 4.5%. In the subsequent press conference, Powell made it clear that the current debates are about the speed of interest rate changes and that duration is not yet seen as the main variable.

The inflation target schedule beeing two years in the future, so the policy rate could be just over 5.0% in 2025.

In addition to the tightening of monetary policy through the key interest rate, there is also a shortage of money in circulation due to a reduction in balance sheets.

At the monetary policy assessment of December 15-2022, the Board of Directors of the SNB, headed by Thomas Jordan, announced a further increase in the key interest rate by 50 basis points to 1%.

Mr Martin Schlegel from the SNB reports a falling demand for banknotes in large denominations such as 200 and 1000 sFr. banknotes. These are particularly in demand in times of crisis, especially in recent years, due to the 2008 financial crisis and the most recent Covid pandemic, there has been above-average demand. Mr. Schlegel explains that since the 2008 financial crisis, the value of cash in circulation in Swiss francs has increased more than twice as much as in the previous two decades. The SNB now sees the declining demand as a result of the rising „bonus“ interest rates on bank account deposits.

Furthermore, the now higher key interest rate in Switzerland and elsewhere is leading to a noticeable containment of the spiral of inflation. Not only Thomas Jordan expressly points out the danger of a wage-price spiral, but also the Chairman of the British Central Bank, Andrew Bailey.

Andrew, in turn, raised the interest rate by 50 basis points to 3.50%, also on December 15th, making clear references to the financial crisis in the UK bond market

We are talking about „pooled“ funds, so-called offshoots of „resilient“ funds and banks, which would trade significantly more risky with unsecured assets. The monetary value mentioned above affects less than 20% of the instruments traded in this segment, but that was still enough to explain the turmoil in the UK bond market.

According to Bailey, regulatory measures to increase financial market stability in the areas mentioned are in the works. The „bread for death“, a sarcastic banker’s jargon for extremely highly leveraged financial products, would increasingly become a danger on global financial markets. However, Bailey pointed out that regulatory action would be enforced by “slow animals,” ie, the slow legislative mills. This means that these (regulatory measures) will only take effect after a delay. Referring to unregulated markets outside of the banking sector, he specifically called “crypto assets” a very risky market. An investment in crypto assets would require a high willingness to make losses.

Christine Lagarde, Chair of the European Central Bank, highlighted not pivoting in the shadow of the Federal Reserve as she just revealed the next 50 basis point rate hike (currently 2.5%). In contrast to the USA (and Japan), there is much more leeway to navigate price stability into the desired range.

Christine’s brooch does not represent F-tilts (weird humor) but might be a sign of civilization on Harok (imaginery Harokans worship the light as sacred).

The US dollar’s acceptance and proliferation is largely due to an overpowering military. The hyperinflationary balance sheet of the Japanese could be reduced to harsh, despotic Bank Keynesianism.

The credo of the European confederation of states „Never again war on European soil“ obliges the currently strongest and most developed democracies in the world to set an example. Europe wants to use diplomacy to strengthen peace and the social market economy as far as possible in light of its own historical failures.

Italy is preventing a European banking union. Christine calls on the Italian government to quickly end its blockade against the ratification of an EU banking union. But Italy is brewing something bigger in the midst of a political odyssey in the void (banks, sovereign debt, provisional governments). Italy links up with the Chinese and benefits from a kind of Silk Road across the Mediterranean. A container port on Italian territory paid for and realized by Chinese companies is the cause of the growing self-confidence, Italian high-of-mind nationalism. Even the USA, by means of the private secret service „Stratfor“, sees no blessing in a united Europe. One prefers to rely on manageable individual states in the subordinate NATO association.

Another variable makes the Italians an enemy of the EU banking union. French President Emmanuel Macron, together with former ECB chairman and Italian long lasting interim president Mario Draghi, sees the EU new credit borrowing limit as obsolete.

Not enough of this cacophony, important events take place on South American soil. Peruvian President Pedro Castillo is in custody. After he was removed from office for high treason, the population held demonstrations and protests to demand his release and early elections. It is a dangerous situation for the demonstrators, according to the protocol it looks as if they are not defending their democracy but, on the contrary, are even trying to overthrow it.

Such a muddle, a democratic “false/true”, is possibly intended by the opposition in order to be able to legitimately bring the population under control with emergency legislation. The situation of the Peruvian working class will probably be inseparable from the situation in Eastern Europe. So-called „caviar leftists“ sometimes see these developments as justification for their own geostrategic goals. The system in question debate is becoming socially acceptable again.

Sorry for this digression into the world of politics and partisanship, but I think at this point a necessary „food for thought“ for one or the other, a welcome pause from facility deposit rate financial data crunching.

And no, a higher key interest rate does not automatically mean (rather contradictory) a higher bonus interest rate!

More details and my outlook on the Foreign Exchange as always for Premium Members.

Sincerely Yours, Ben

Guten Abend Traders,

die Federal Reserve schaut auf eine vermeintlich auslaufende Inflation, mit zuletzt 6% Kerninflation (Jahresvergleich Monat November) gegenüber 6.3% im Vormonat und 6.2% in den Vorhersagen.

In wenigen Minuten die Veröffentlichung der Leitzinsentscheidung, um 20:00Uhr (Brüssel UTC+1). Ab 20:30Uhr die spannende Pressekonferenz des Vorsitzenden Jerome Powell.

Morgen ein Tripel mit Thomas Jordan (SNB), Andrew Bailey (BoE), sowie Christine Lagarde (ECB).

Bleibt unbedingt am Markt, eine erhöhte Volatilität und womöglich ein kurzfristiger Swingpoint ist wahrscheinlich. Die Yieldkurven sind allesamt komplett invertet, eine zumindest milde Rezession nicht mehr zu vermeiden. Sollte nun die alles gefürchtete Lohn-Preisspirale beginnen zu accelerieren, so sehen wir die Inflation erst Q4-2023 in den Zielbereichen einpendeln. Nun heißt es erst einmal durch den Winter kommen und sich einfuchsen…

Weitere Details und Ausblick auf den Exchange wie immer für Premium-Mitglieder.

Bünyamin

Goody Traders,

In a few minutes the publication of the key interest rate decision, at 20:00 (Brussels UTC+1). Don’t miss the exciting press conference from 8:30 p.m. by Chairman Jerome Powell.

Tomorrow a triple with Thomas Jordan (SNB), Andrew Bailey (BoE) and Christine Lagarde (ECB).

Be sure to stay in the market, increased volatility and possibly a short-term swing point is likely. All yield curves of the major economies are completely inverted, so an at least mild recession can no longer be avoided. Any of the past seven instances of inverted yield curves has been followed by a recession. Should the feared wage-price spiral now begin to accelerate, we defenitely will not see inflation leveling off in the target ranges until Q4-2023. Now it’s time to get through the winter and to take stuff smart…

More details and my outlook on the Foreign Exchange as always for Premium Members.

Sincerely Yours, Ben

Guten Abend,

November-01 2022, die Reserve Bank of Australia erhöht erneut ihren Leitzinssatz um weitere 25 Basispunkte auf nunmehr 2.85%.

November-02 2022, die FED mit einer erneuten Mammut-Leitzinserhöhung, 75 Basispunkte, kommt somit aktuell bei 4.00% zum Liegen.

November-03 2022, die Bank of England zieht an, die größte Leitzinserhöhung seit 1989 +75 Basispunkte auf 3.00%.

Deutlicher wird die Lage, wenn man sich die Pressekonferenz von Jerome genauer anhört. Der „neutrale“ Leitzinssatz dürfte nunmehr überschritten sein, weitere Zinserhöhungen sind sehr wahrscheinlich. Dazu will man die Geldmenge, das Balance Sheet weiter reduzieren. Projektionen liegen bereits in Q1-2023 bei 4.00-7.00%. Bis 2024 dürfte es keine nennenswerte Leitzins-Verringerung mehr geben. Ein Leitzins von 4.00-6.00% scheint für Q4-2023 realistisch.

Die britische Zentralbank um Andrew Bailey reagiert mit einer historisch extremen Erhöhung und zeigt damit Nerven.

In meinem Beitrag YCC-2-10-40 vom 02. Oktober 2022 hatte sich ein Übersetzungsfehler eingeschlichen. ‚Billion‘ meint im Englischen eben Milliarde und nicht Billion. Ich bitte um Beachtung und korrigiere mich in der Folge um folgende Aussage:

Bis zum 14. Oktober hat die BoE mit £10.4 Milliarden Gilts mit langer Laufzeit (‚temporary and targeted purchases of long-dated UK government bonds‘) akquiriert. Ab dem 10. Oktober erhöhte die BoE ihr maximales Budget von täglich £5 Milliarden auf £10 Milliarden. In dem Zeitraum vom 28. September bis 14. Oktober waren somit £65 Milliarden für Ankäufe von britischen Government Bonds zugesprochen. Mit dem 01. November hat die Bank bereits wieder begonnen, Gilts (britische Staatsanleihen) auf dem Bondmarkt zu veräußern.

Diese „Notoperationen“ zeigen zusammen mit Allzeit-Tiefs der Exchange-Pairs (GBPUSD, GBPCHF) deutlich, dass das Pfund auf dem Zahnfleisch kaut. Sollte sich die Situation beruhigen, ergibt sich ein guter Swing Point Trade. Gerade gegen den Euro, hat das Pfund von der „Offshore“-Insel noch nie die Lufthoheit verloren. Im Klartext bedeutet dies, dass das Paar EURGBP nie Parität erreichen konnte, dagegen das negativ korrelierte Paar GBPCHF sich gegen eine Safe-Heaven Währung zu behaupten sucht. Die Aufwertung des sFr. wird irgendwann umkehren, im Lichte der eben erwähnten Korrelation ergibt sich ein ‚Premium‘ Carry-Trade auf GBPCHF (Interest Rate Differenz). Wenn Du Nerven und das nötige Kleingeld beiseite hast, darfst Du gerne zugreifen, achte aber dringend darauf, dass Dein Broker Dir auch die Swaps ausbezahlt und nicht gar noch Übernachthaltekosten anfallen.

Bei mir geht es nun wieder weiter mit Dash-Programmierung und dem Umbau der Website. Wie gewohnt bleibe ich 24/5 für Deer an den Märkten!

Weitere Details und Ausblick auf den Exchange wie immer für Premium-Mitglieder.

Bünyamin

Goody Traders,

November-01 2022, the Reserve Bank of Australia raises its key interest rate again by a further 25 basis points to 2.85%.

November-02 2022, the FED with another mammoth interest rate increase, 75 basis points, currently at 4.00%.

November-03 2022, Bank of England tightens, largest rate hike since 1989 +75 basis points to 3.00%.

The situation becomes clearer if you listen to Jerome’s press conference more closely. The „neutral“ key interest rate should now have been exceeded, and further interest rate hikes are very likely. In addition one wants to further reduce the money supply, the balance sheet. Projections are already at 4.00-7.00% in Q1-2023. By 2024, there should not be any significant reduction in key interest rates. A key interest rate of 4.00-6.00% seems realistic for Q4-2023.

The British central bank around Andrew Bailey reacts with an historically extreme increase which one displays the decreasing level of patience by the British central.

A translation error crept into my contribution YCC-2-10-40 on October 02, 2022. In German ‚Billion‘ means ‚Milliarde‘ (10^9) and eng. ‚Trillion‘ equals ger. ‚Billion‘ (10^12). I ask for your attention and correct myself as a result by the following statement:

As of October 14, the BoE has acquired £10.4 billion in Gilts (temporary and targeted purchases of long-dated UK government bonds). From October 10th, the BoE increased its maximum daily budget from £5bn to £10bn. Thus, in the period from September 28 to October 14, £65 billion had been committed for UK government bond purchases. As of November 1st, the bank has already started selling Gilts (British government bonds) on the bond market again.

These „emergency operations“ along with all-time lows in exchange pairs (GBPUSD, GBPCHF) clearly show that the pound is chewing on the gums. If the situation calms down, a good swing point trade results. Especially against the euro, the pound from ‚offshore island‘ has never lost its supremacy. In plain language, this means that the EURGBP pair has never been able to reach parity, while the negatively correlated GBPCHF pair is trying to hold its ground against a superb safe-heaven currency. The appreciation of the sFr. will eventually reverse, in light of afordmentioned correlation resulting in a ‚premium‘ carry trade on GBPCHF (Interest Rate Difference). If you have nerves of steel and the necessary small change, you are welcome to buy the pair, but make sure that your broker pays you the interest difference profit (sometime overlaped by overnight holding costs).

For me it’s now back to Dash programming and the redesign of the website. As usual, I’ll be at the markets 24/5 for you, my Deer!

More details and my outlook on the Foreign Exchange as always for Premium Members.

Sincerely Yours, Ben

Guten Abend Traders,

Sveriges Riksbank, 20-September 2022, +100bp (0.75% -> 1.75%)

Fed, 21-September 2022, +75bp (2.50% -> 3.25%)

United Arab Emirates, 21-September 2022, +75bp (3.75% -> 4.50%)

Central Bank of Brazil, 21-September 2022, +0bp (13.75% -> 13.75%)

Saudi Central Bank, 21-September 2022, +75bp (3.00% -> 3.75%)

Bank of Japan, 22-September 2022, +0bp (-0.1% -> -0.1%)

Bank Indonesia, 22-September 2022, +50bp (3.75% -> 4.25%)

Swiss National Bank, 22-September 2022, +75bp (-0.25% -> 0.5%)

Norges Bank, 22-September 2022, +50bp (1.75% -> 2.25%)

Central Bank of Turkey, 22-September 2022, -100bp (13.0% -> 12.0%)

Bank of England, 22-September 2022, +50bp (1.75% -> 2.25%)

South African Reserve Bank, 22-September 2022, +75bp (5.50% -> 6.25%)

Hong Kong Monetary Authority, 22-September 2022, +75bp (2.75% -> 3.50%)

Willkommen im Nachleben, die Woche des Todes liegt nun hinter uns. Die vermeintlich gute Nachricht: es wird schlimmer, bevor es besser werden kann!

Gerade das britischen Pfund vs. US-Dollar wurde bereits regelrecht abgeschlachtet, -5.00% auf die Woche, volle -3.66% am letzten Handelstag.

Fr. 23-September 2022: GBPUSD Low-of-Week/Day @1.0839 (Allzeit-Tief)

Das Empire spielt Blinde-Kuh mit den Märkten, zwei hin vier im Sinn, und kürzt hier und da ein paar Steuern. Daneben kommen die Auswirkungen des Brexits vollends zum Tragen, neben Supply-Chain und Energiekrise. Der neue König noch etwas verdattert und die frisch gebackene Premierministerin, Mrs. Mary Elizabeth Truss, naja forsch. Das ‚House of Common‘ ist die letzte Bastion des Empire, die herausragenste Institution die die römisch-griechische Hochkultur hervorgebracht hat. Die Redner-und Debatierkunst bietet höchstes Niveau, die Parlamentarier allesamt Teil des Ganzen.

Was spricht für den Pfund?

1) Das Königreich hat eine Zentralbank, deren Geschichte bis in das Jahr 1694 zurückreicht. Es ist dies eine der 10 ältesten Banken überhaupt. Die ausgewiesene Bilanz (das Balance-Sheet), zeigt sicher nicht die Gesamtheit aller Verflechtungen, die mit dem britischen Pfund zusammenhängen mögen.

2) Valuta können tatsächlich unterbewertet sein, so auch ganz speziell Währungen. Was nicht bedeuten muss, dass der zugrunde liegende Eigenwert verloren gegangen ist.

Dagegen wiederum, musste bedingt durch den Brexit, das Pfund in der Hochfinanz seine prestigeträchtige Londoner Sonderstellung gegenüber Frankfurt am Main einbüßen.

Klare Flucht- bzw. Safe-Heaven-Währungen sind nunmehr Schweizer Franken, Norwegische Krone, der US-Dollar und weniger ein Seemanns Pfund. Schreibe den britischen Pfund nicht all zu früh ab! Robustere Zentralbanken gibt es wenige, Geld wird auch weiterhin nach London und von dort hinaus in die Welt fließen. Die Wirtschaft, die Börsen waren gerade auf Allzeithochs, haben Pandemie und Krisen auf dem Buckel; nun verlangen wir mal nicht zu schnell zu viel von einem Markt, welcher Realität von Wunschdenken unterscheiden kann.

Thomas Jordan, trat vor laufende Kameras und lieferte eine sagenhafte Pressekonferenz. Menschlich und fachlich völlig überzeugend, setzte er alle Kritiker in den Zentralbank-sFr.-Kernschatten. Auch das pragmatische Podium überzeugte in seiner zweckmäßigen Schlichtheit.

Überschüsse der letzten Geschäftsjahre könnten durchaus zur Durchsetzung geldmarktpolitischer Ziele herangezogen werden, so die SNB sinngemäß.

Einziger Versprecher; diese Leitzinserhöhung (+75bp) in den positiven Bereich würde wohl genügen, um die Inflation im gewünschten Bereich zu halten. Diese Aussagemodalität wurde im Verlauf der PK nach und nach aufgeweicht, wie dann die Fragesteller wie selbstverständlich wissen wollten, ob die SNB ähnlich schnell und stark ihren Leitzinssatz anheben werde wie das hiesige Umfeld. Thomas konnte seine Eingangsformulierung nicht verteidigen und triftete etwas in Richtung „ausreichender Maßnahmenkatalog“ ab. Man wolle ordungspolitische Grundprinzipien stärken und werde dazu regelmäßige Geldmarkt-Lageberichte in Form von Pressekonferenzen abhalten.

Wir sind sehr, sehr dankbar hierfür Herr Jordan, weiter so, wir sind sehr gespannt auf den nächsten (zweitunten) Auftritt!

Weitere Details und Ausblick auf den Exchange wie immer für Premium-Mitglieder.

Bünyamin

Goody Traders,

Sveriges Riksbank, 20-September 2022, +100bp (0.75% -> 1.75%)

Fed, 21-September 2022, +75bp (2.50% -> 3.25%)

United Arab Emirates, 21-September 2022, +75bp (3.75% -> 4.50%)

Central Bank of Brazil, 21-September 2022, +0bp (13.75% -> 13.75%)

Saudi Central Bank, 21-September 2022, +75bp (3.00% -> 3.75%)

Bank of Japan, 22-September 2022, +0bp (-0.1% -> -0.1%)

Bank Indonesia, 22-September 2022, +50bp (3.75% -> 4.25%)

Swiss National Bank, 22-September 2022, +75bp (-0.25% -> 0.5%)

Norges Bank, 22-September 2022, +50bp (1.75% -> 2.25%)

Central Bank of Turkey, 22-September 2022, -100bp (13.0% -> 12.0%)

Bank of England, 22-September 2022, +50bp (1.75% -> 2.25%)

South African Reserve Bank, 22-September 2022, +75bp (5.50% -> 6.25%)

Hong Kong Monetary Authority, 22-September 2022, +75bp (2.75% -> 3.50%)

Welcome to the afterlife, the week of death is now behind us. The supposedly good news: it gets worse before it can get better!

The British Pound in particular has already been slaughtered, -5.00% on the week, a full -3.66% in the last trading day.

Fri 23-September 2022: GBPUSD Low-of-Week/Day @1.0839 (all-time low)

The Empire is playing blind man’s bluff with the markets, two versus four in mind, cutting a few taxes here and there. In addition, the effects of Brexit are fully felt, along with the supply chain and energy crisis. The new king is still a little taken aback and the newly minted Prime Minister, Mrs. Mary Elizabeth Truss, well brisk. The ‚House of Common‘ is the last bastion of the Empire, the most outstanding institution that the Roman-Greek high culture has produced. The art of speaking and debating offers the highest level, the parliamentarians are all part of the whole.

What about the pound?

1) The kingdom has a central bank whose history dates back to 1694. It is one of the 10 oldest banks ever. The reported balance sheet certainly does not show the entirety of all interrelationships that may be related to the British pound.

2) Assets can actually be undervalued, especially currencies. Which does not necessarily mean that the underlying intrinsic value has been lost.

On the other hand, due to Brexit, the pound had to lose its prestigious special position in London compared to Frankfurt am Main in high finance.

Clear escape or safe heaven currencies are now Swiss francs, Norwegian krone, the US dollar and less a sailor’s pound. Don’t write off the British pound too soon! There are few more robust central banks, money will continue to flow to London and from there to the world. The economy, the stock markets were at all-time highs, have pandemics and crises under their belts; Now let’s not be too quick to ask too much of a market that can distinguish reality from wishful thinking.

Thomas Jordan, stepped in front of the cameras and performed an incredible press conference. Completely convincing on a personal and professional level, he placed all critics under the umbra of his central bank. The practical simplicity of the pragmatic podium was also convincing.

Poor choise of words when Jordan initially states, that this rate hike (+75bp) into positive territory would probably be enough to keep inflation in the desired range. This statement modality was gradually softened in the course of the press conference, as the questioners then stoically wanted to know whether the SNB would raise its key interest rate as quickly and as strongly as the environment. Thomas was unable to defend his initial formulation and deviated somewhat in the direction of „sufficient catalog of measures“. The SNB intends to strengthen basic regulatory principles and will hold regular money market status reports in the form of press conferences.

We are very, very grateful Mr. Jordan, keep it up, we are excited about the next (second below) performance!

More details and my outlook on the Foreign Exchange as always for Premium Members.

2023-05-27: „Ich werde bis Ende Mai einige Updates auf MumbleFX einspielen. Die Seite wird vorübergehend auf „Maintainance“ gesetzt und damit nicht erreichbar sein.“

2023-05-27: „Ich werde bis Ende Mai einige Updates auf MumbleFX einspielen. Die Seite wird vorübergehend auf „Maintainance“ gesetzt und damit nicht erreichbar sein.“

2023-05-27: „I’ll be rolling out some updates to MumbleFX by the end of May. The page will be temporarily set to „Maintenance“ and will therefore not be accessible.“

2023-05-27: „I’ll be rolling out some updates to MumbleFX by the end of May. The page will be temporarily set to „Maintenance“ and will therefore not be accessible.“