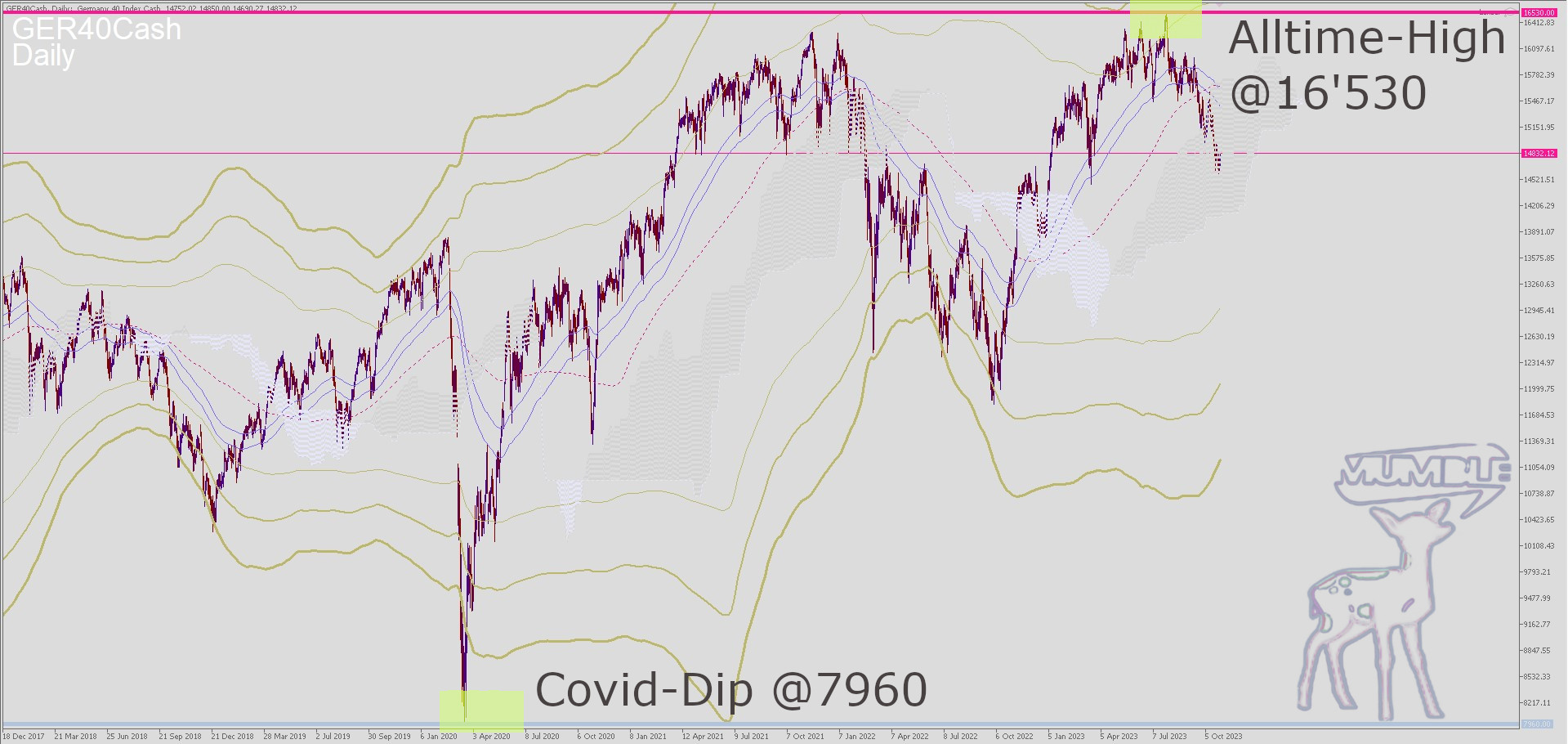

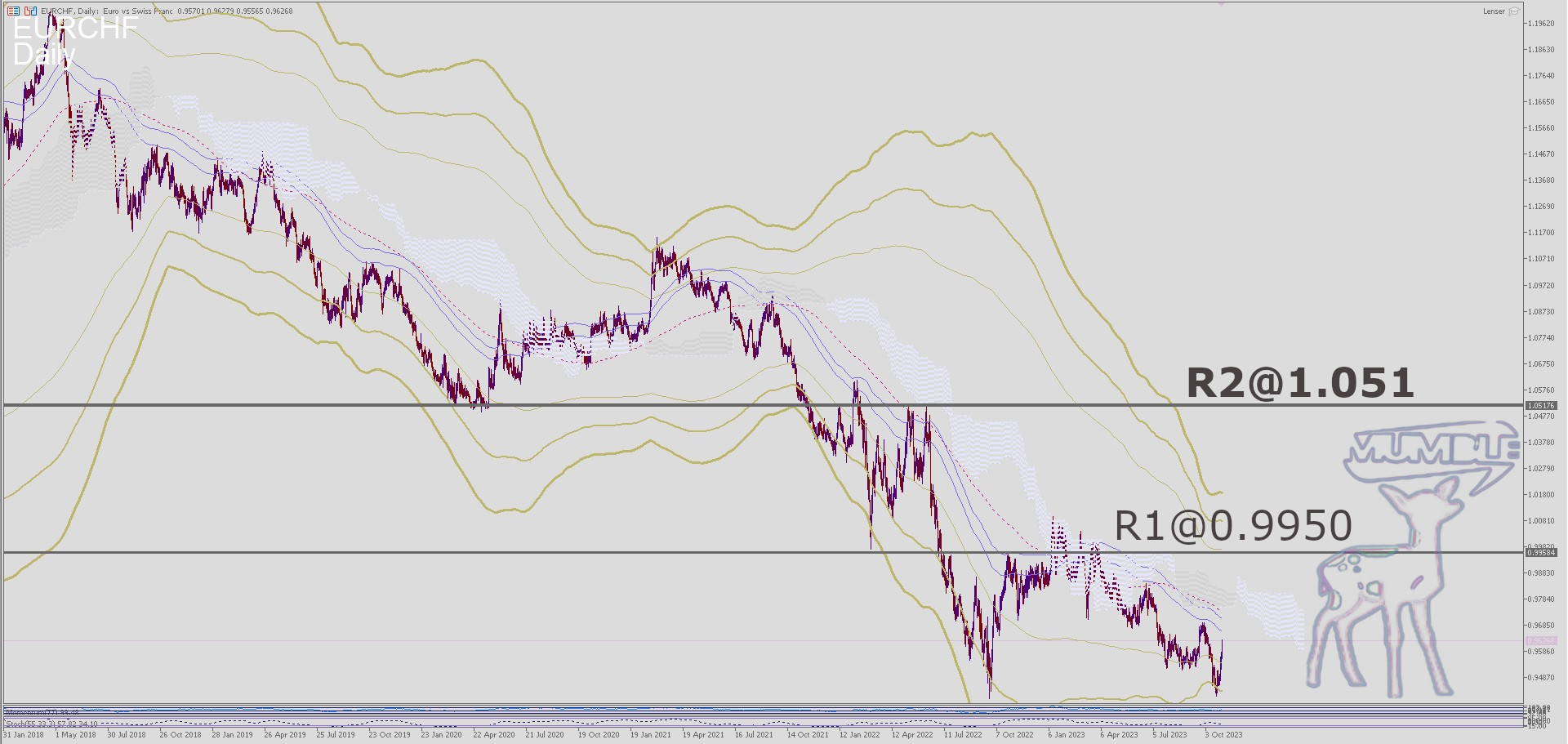

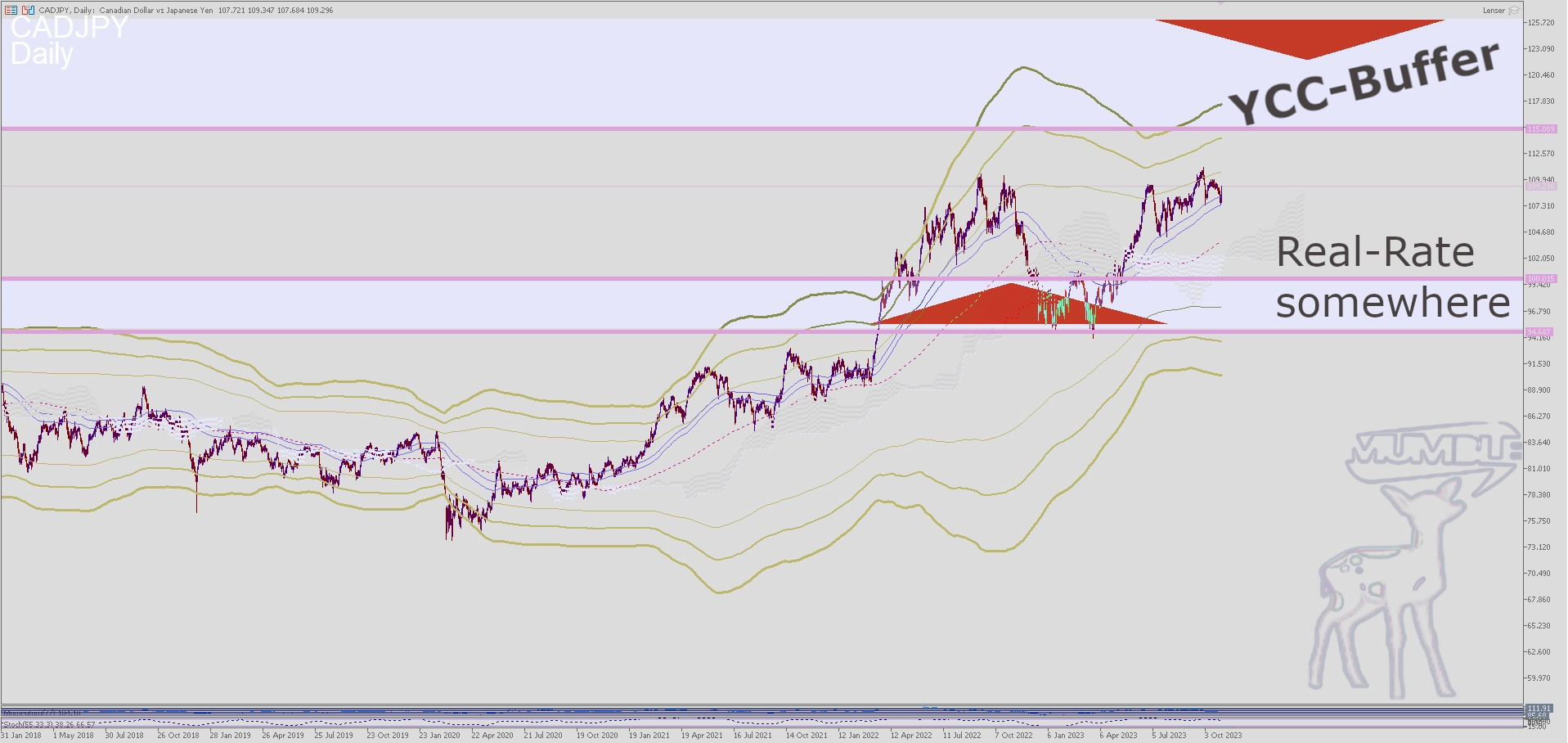

Phat green line

2023-11-13 19:02:59 GMT+1Guten Abend

2023-11-07, die RBA erhöht ihren Leitzins um 25 Basispunkte auf 4.35%.

2023-11-07, die RBA erhöht ihren Leitzins um 25 Basispunkte auf 4.35%.

Der neue Governor Michele Bullock mit einer Leitzinserhöhung ohne Pressekonferenz. In Ihrem Statement lesen wir „[…] globally, there remains a high level of uncertainty around the outlook for the Chinese economy and the implications of the conflicts abroad.“.

Damit sind natürlich der Krieg Russlands in der Ukraine sowie der Vergeltungsschlag Israels im Nahen Osten gemeint.

Der Markt zeigte keine nennenswerte Reaktion auf diese Erhöhung, es sieht vielmehr danach aus, dass die 25 australischen Basispunkte bereits voll eingepreist waren.

J (Jerome Powell) wurde in zwei seiner kürzlich gegebenen öffentlichen Reden von (Umwelt-) Aktivisten unterbrochen. Am Dienstag des 19. Oktobers bei einer Rede zum 730sten EconClubNY und am 09. November bei einer Konferenz des IMF. Hier waren zudem folgende Top-Ökonomen und Zentralbanker zugegen: Gita Gopinath (stellvertretenbde Geschäftsführerin IMF),

Ken Rogoff (Professor für Ökonomie, Havard), Amir Yaron (1. Vorsitzender der Zentralbank Israel) und Pierre-Olivier Gourincha (Chefökonom IMF).

Lustigerweise hat Powell das f** Wort in den Mund genommen. „just close the f*** door“ waren seine tiefsinnigen Anmerkungen. J hat seine Rede dennoch zu Ende geführt.

Warum demonstrieren diese ungehobelten Wichtigtuer nicht erst einmal ökonomische Grundkenntnisse? Wer ins Rampenlicht will, nutzt einfach die Umweltmasche, Idiotensicher.

An dieser Stelle sei gesagt, alle Argumente dieser Armleuchten liegen nicht erst seit gestern auf dem Tisch. Keinen Umweltaktivisten schert es, wenn ihre Bitcoins CO2 Schleudern sind,

oder ihre Pflänzchen im Wettstreit um den Phosphordünger der Dritten Welt steht.

Keine Technologie, von Solarpanels bis E-Mobilität sind Teil einer Lösung des Treibhaus-Problems.

Ein einzig nachhaltiger Paradigmenwechsel fängt auf dem Teller an, und dazu eignet sich meiner Auffassung nach, der (sozial verträgliche) Kapitalismus am besten.

Einen Raubtierkapitalismus á la U.S.A. können wir Europäer am ehesten bändigen. Niemand aber kann sicher wissen, ob eine Demokratie mit Gewaltenteilung und ohne Second Amendment am Ende überleben wird.

Eine Demokratie muss hin und wieder verschiedene Masken tragen, um dem Feind überlegen zu bleiben. Nur eines darf diese Gesellschaftsordnung nicht, da bleiben wir beim Nenner, dem Mittelalter einen Weg ebnen.

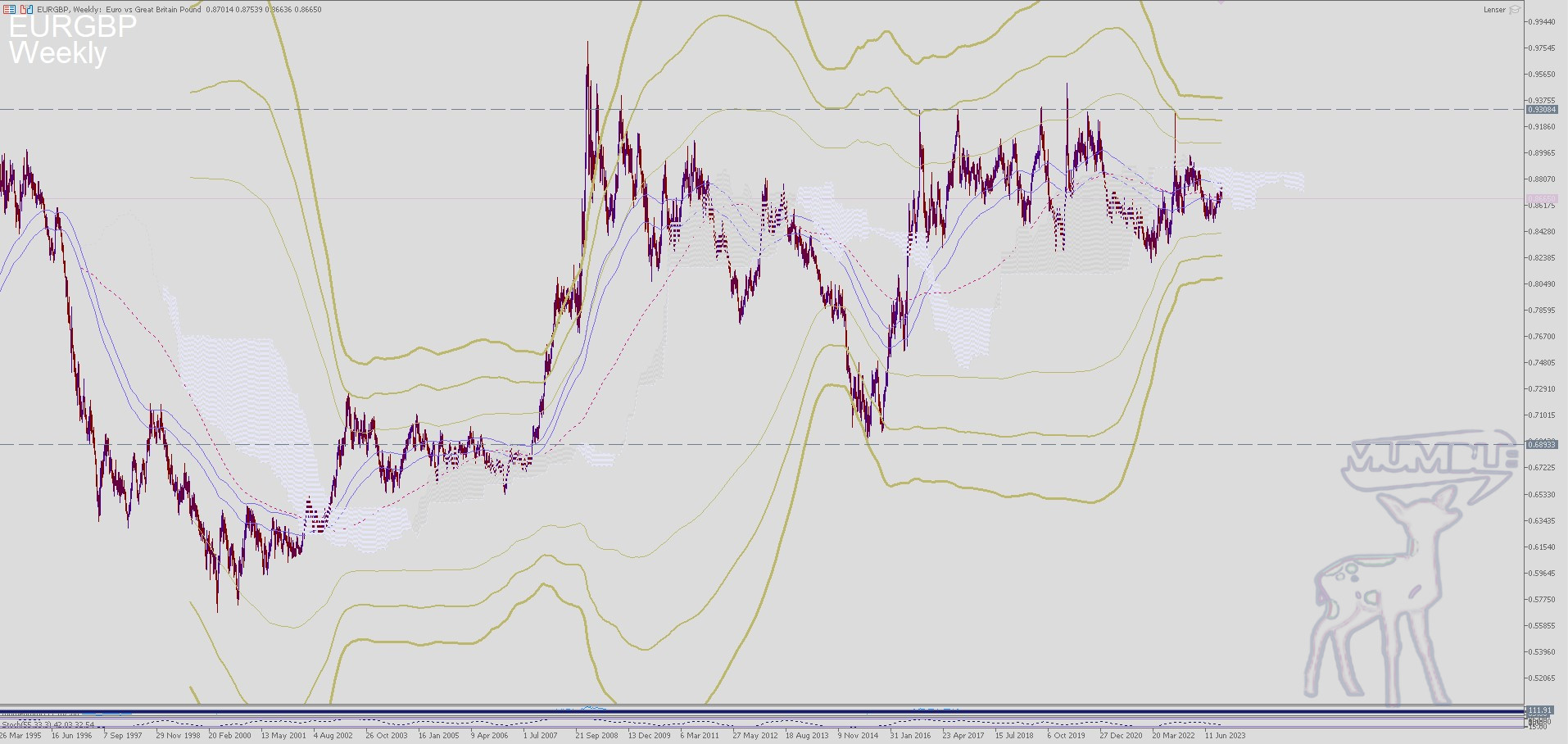

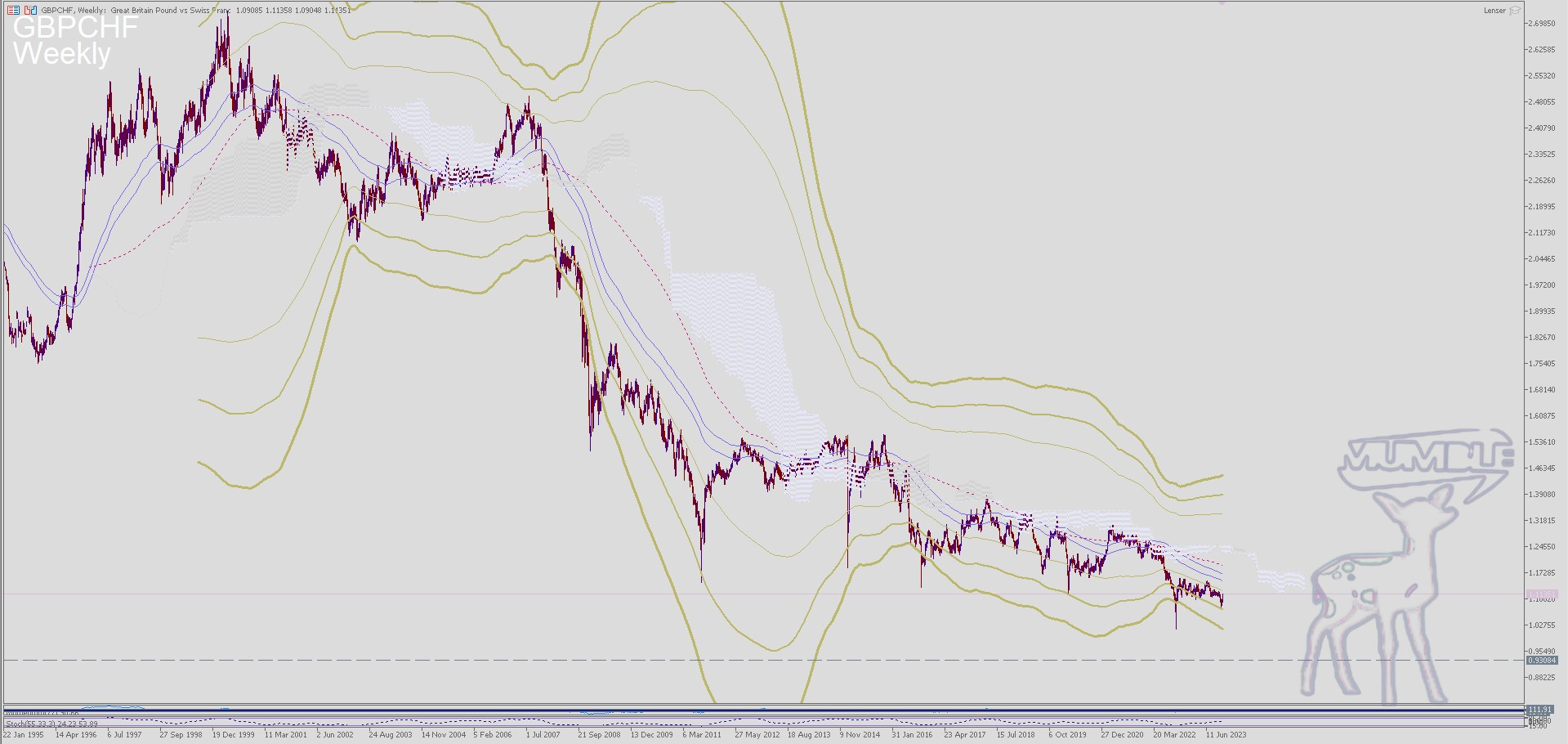

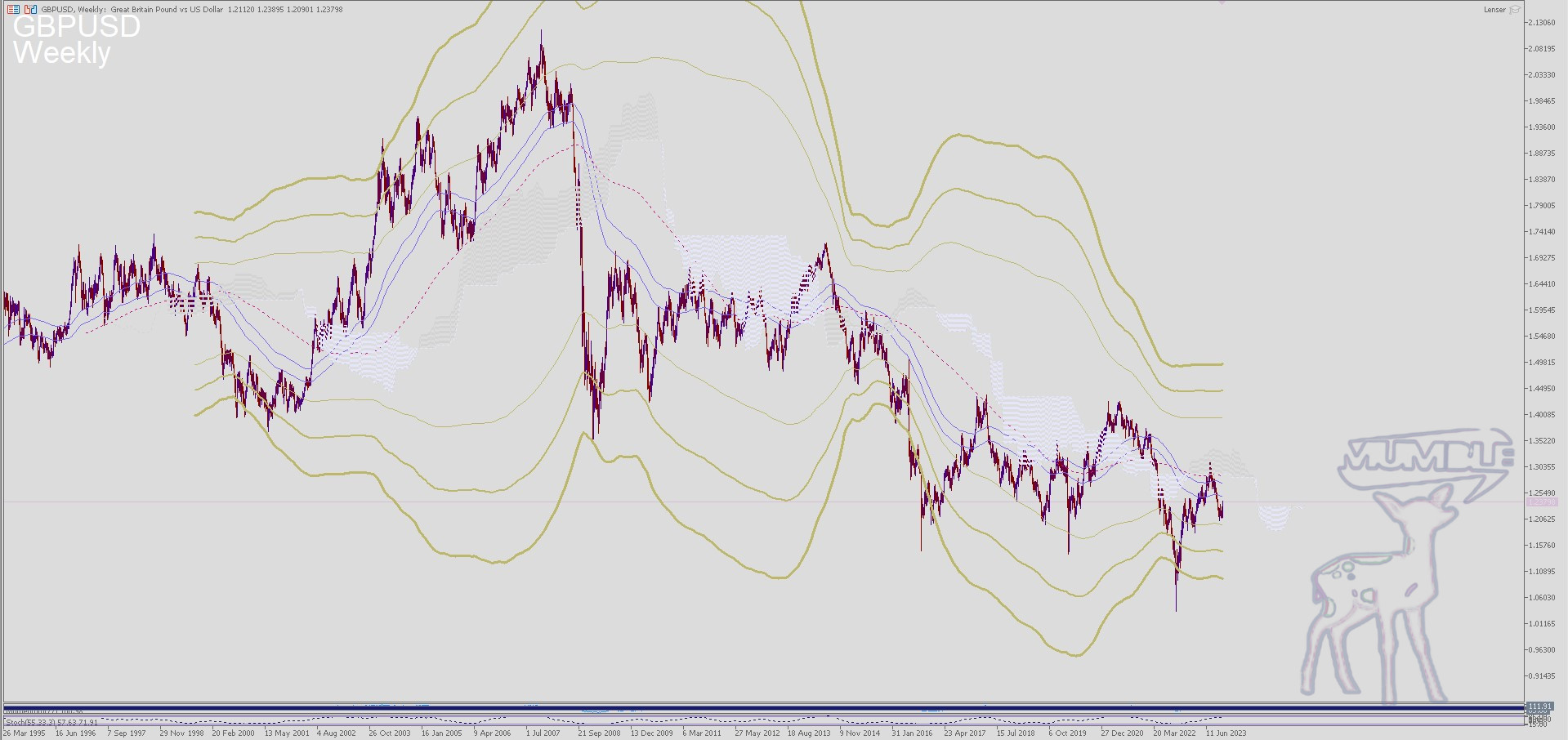

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

LG Ben

Goody Traders

2023-11-07, the RBA increases its key interest rate by 25 basis points to 4.35%.

2023-11-07, the RBA increases its key interest rate by 25 basis points to 4.35%.

The new governor Michele Bullock with a key interest rate increase without a press conference. In her statement we read „[…] globally, there remains a high level of uncertainty around the outlook for the Chinese economy and the implications of the conflicts abroad.“

This of course refers to Russia’s war in Ukraine and Israel’s retaliatory strike in the Middle East.

The market showed no significant reaction to this increase, in fact it appears that the 25 Australian basis points were already fully priced in.

J (Jerome Powell) was interrupted by (environmental) activists in two of his recent public speeches. On Tuesday, October 19th at a speech at the 730th EconClubNY and

on November 9th at an IMF conference. The following top economists and central bankers were also present, namely: Gita Gopinath (Deputy Managing Director IMF),

Ken Rogoff (Professor of Economics, Havard), Amir Yaron (1st Chairman of the Central Bank of Israel) and Pierre-Olivier Gourincha (Chief Economist IMF).

Funnily enough, Powell used the f** word. “just close the f*** door” were his profound comments. But with no suprise, brave and honorable J finished his speech with dignity.

Why don’t these uncouth busybodies first demonstrate basic economic knowledge? If you want to be in the spotlight, simply use the environmental scheme, idiot-proof.

At this point it should be said that all the arguments of these dushbags have not just been on the table since yesterday. No environmental activist cares if their Bitcoins are CO2 slingers, or if their Cannabis-farms are in competition with the third world’s phosphorus fertilizer.

No technology, from solar panels to e-mobility, is part of a solution to the greenhouse problem.

The only sustainable paradigm shift starts on the plate, and in my opinion socially acceptable capitalism (yes to the ‚burgergeld‘ experiment! it’s the opposite to fiefdom and feudal system) is best suited to pave way for this goal.

The Europeans are best placed to tame predatory capitalism like in the USA. But no one can know for sure whether a democracy with separation of powers (legislative, judicial, executive) and without Second Amendment will survive in the end.

A democracy must put on different masks every now and then in order to remain superior to the enemy.

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben&Nic

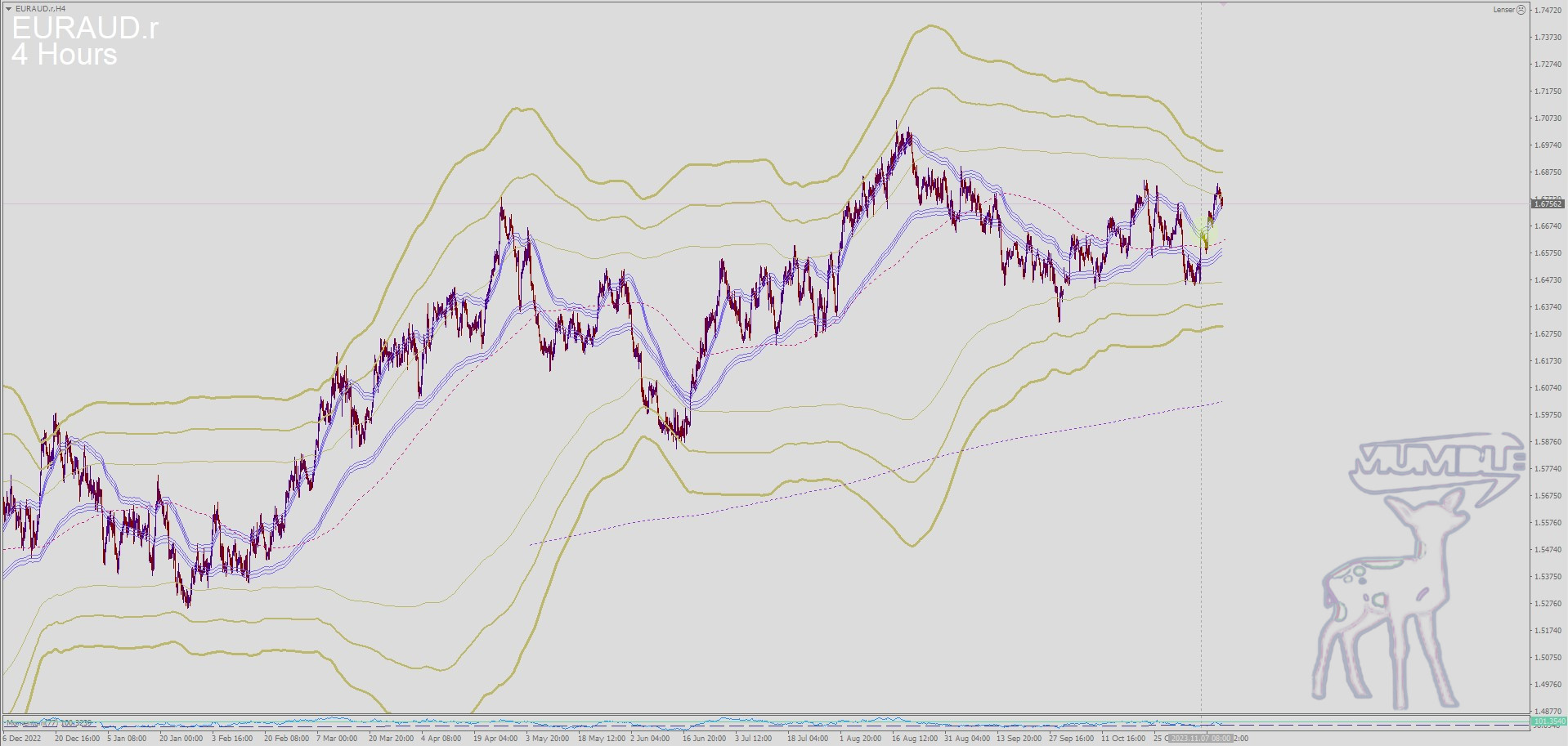

EURAUD H4-Chart

Psst… der Boden ist Lava.