Guten Morgen,

03-Mai-2023, die Federal Reserve erhöht ihren Leitzinssatz um 25 Basispunkte auf 5.25%.

03-Mai-2023, die Federal Reserve erhöht ihren Leitzinssatz um 25 Basispunkte auf 5.25%.

Eine prekäre Situation für die Weltwirtschaft, erstens? Einerseits treiben Inflation und inverte Yieldkurven das Schreckgespenst namens „Rezession“ um die Hochhausblöcke, andererseits war doch gerade ein gigantisches Quantitative Easing der Garant für die „financial market resilience“. Geht nebenher eine US-Bank den Bach runter, die kalifornische Silicon Valley Bank, so sieht man die FED mit dem Rücken zur Wand.

Was aber ist der Grund für den Kollaps der hiesigen Tech-Family, deren Einlagen im Zuge der Covid-Abwehrmaßnahmen von $60 Milliarden in 2020 auf $200 Milliarden in 2022 angesprungen waren? Start-Ups, und besonders Crypto und Marihuana Unternehmen, wurden mittels SPACs (Special Purpose Acquisition Company) ins Leben gerufen, noch bevor diese überhaupt existierten. Ja! Genau richtig gelesen! Zuerst wird Geld gesammelt – fund raising – um sich im Anschluss daran Gedanken zu machen, welch ein Unternehmen man damit gründen könnte. Glaubst Du wirklich, die hippen Kalifornier kaufen mit ihren Milliarden einfach nur US-Treasuries und Mortgage-Backed Securities? Crypto, Crypto, Tech-SS und Jungspund-Crypto sind der Grund für ein maßloses Risiko in ein Asset, mittels die Tech-Familie den US-Dollar und alle übrigen Währungen der Welt aushebeln wollen. Dieses Risiko hat sich nun selbst herausgekürzt, nebst der Crypto-Bank „Silvergate“. Anmerkung: Kursverluste können über ein geeignetes Unternehmen steuerlich abgesetzt werden :Anmerkung Ende.

Aus Sicht der kapitalistischen Eliten rund um die Zentralbanken, hat sich der Schimmel am Kuchen selbst abgeschnitten. Ein doppelter Beleg für die gesunde Funktionalität der Finanzmärkte.

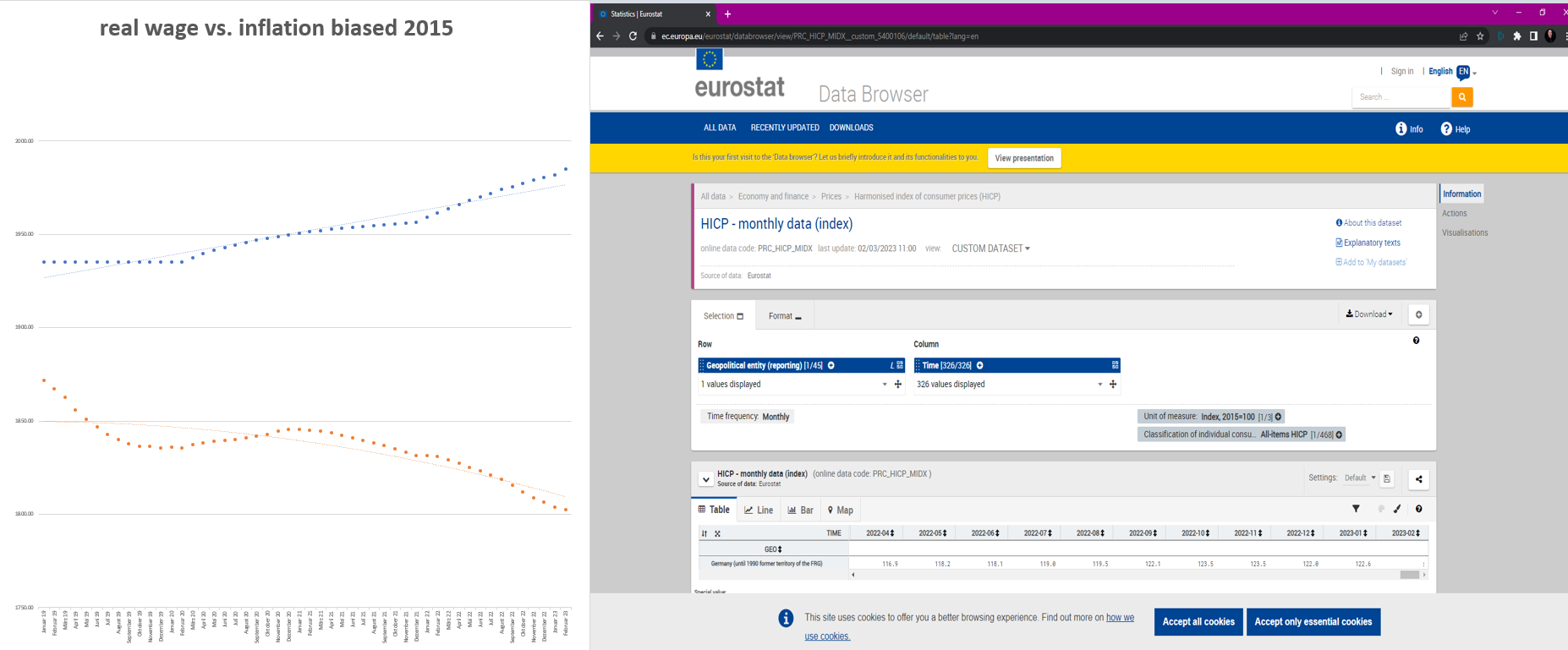

04-Mai-2023, die ECB erhöht ihren Leitzins um 25 Basispunkte auf 3.75%. Ein historischer Anstieg des Leitzinssatz, was auf die andauernd hohen Inflationswerte zurückzuführen ist.

Eine Gefahr für die Märkte, zweitens?

Das Geld ist zwar aus den Büchern der Zentralbanken, die gigantischen QE-Programme aber haben derart viel Kapital in Umlauf gebracht, was in dem Zeitraum zuvor 1/4 Jahrhundert gedauert hatte. Dieses Geld steht bereit, im Kontrast zu Situationen mit Inverten-Yieldkurven vorangegangener Marktsituationen, um jedweden Börsen-Dip aufzukaufen. Die reale Aufhängung lautet: Unternehmen sind die Speerspitze des kapitalistischen Paradigmas, ermöglichen Arbeitsplätze, Konsum und Umsatz. Diese Unternehmen werden mit Geldern aus Hedge-Fonds umspült, welche Klienten Regierungen von Hammerfest bis Kapstadt unterhalten. Regierungen erhalten ihre Mittel über Anleihen, welche die Zentralbanken nun aufgekauft haben. Darüber hinaus, selbstverständlich von der bürgerlichen Wählerschaft, welche ihre Arbeitsplätze gesichert sehen möchten.

Wo den nun exakt eine Gefahr für die Märkte bestehen soll, wenn nicht für die Vermögensmacht der unangefochtenen Kolonialstaaten, kann niemand numerisch genau bestimmen. Die Wurzeln der Macht reichen tief und die smartesten Leute schützen eben genau diese Valuta. Zwei Weltkriege sind von den Börsen der Welt absorbiert worden. Es wäre wenn denn gesetzten Falles, eine Transformation in Nullzeit hin zu einer Gift- und Green-Culture, eine hübsche Vision, deren Realität nur Schritt für Schritt erreicht werden kann.

Weitere Details und einen Ausblick auf den FX Exchange wie immer für Premium-Mitglieder.

Bünny

Goody Traders,

03-May-2023, the Federal Reserve raises its key interest rate by 25 basis points to 5.25%.

03-May-2023, the Federal Reserve raises its key interest rate by 25 basis points to 5.25%.

A precarious situation for the world economy? On the one hand, inflation and inverted yield curves are driving the specter of „recession“ around the skyscrapers, on the other hand, gigantic quantitative easing was the guarantor of „financial market resilience“. If a US bank goes down the drain at the same time, the Californian Silicon Valley Bank, you see the FED with its back to the wall.

But what is the reason for the collapse of the „Kali“ tech family, whose deposits had jumped from $60 billion in 2020 to $200 billion in 2022 in the course of the Covid defense measures? Start-ups, and especially crypto and marijuana companies, were created by SPACs (Special Purpose Acquisition Company) before they even existed. Yes! You read that right! First, money is collected – fund raising – in order to then think about what kind of company one could create with it. Do you really think hip Californians just buy US Treasuries and Mortgage-Backed Securities with their billions? Crypto, Crypto, Tech-SS (Waffen-SS, SA) and Nazi-Youth-Crypto are the reason for excessive risk in an asset, with which the tech family want to superseed the US dollar and all other currencies in the world. This risk has now reduced itself, along with the crypto bank „Silvergate“. Note: Exchange rate losses can be deducted for tax purposes via an appropriate company : end of note.

From the point of view of the capitalist elites surrounding the central banks, the mold has cut itself off teh cake. A double proof of the healthy functioning of the financial markets.

04-May-2023, the ECB increases its key interest rate by 25 basis points to 3.75%.

A historic increase in the key interest rate, which is due to persistently high levels of inflation.

A threat to the markets? The money is off the central banks‘ books, but the gigantic QE programs have pumped in so much capital that previously took 1/4 century to create. This money stands ready, in contrast to inverted yield curve situations of previous market situations, to buy any stock market dip. The real suspension is: companies are the spearhead of the capitalist paradigm, enabling jobs, consumption and turnover. These companies are being showered with money from hedge funds whose clients are governments from Hammerfest to Cape Town. Governments get their funds from their own bonds issued, which central banks have now bought up. In addition, of course, by the bourgeois electorate, who want to see their jobs secured.

Exactly where there is a danger for the markets, if not for the wealth power of the undisputed colonial states, nobody can precisely determine numerically. The roots of power run deep and the smartest people protect that very realm. Two world wars have been absorbed by the stock markets of the international community. If any revolution, it would be a zero-time transformation towards a gift and green culture, a pretty vision whose reality can only be achieved step by step.

More details and my outlook on the FX Exchange as always for Premium Members.

Sincerely Yours, Ben&Nic

連邦準備制度記者会見午後8時30分UTC+2(ベルリン)

連邦準備制度記者会見午後8時30分UTC+2(ベルリン) Federal Reserve Press Conference 08:30pm UTC+2 (Berlin)

Federal Reserve Press Conference 08:30pm UTC+2 (Berlin) Federal Reserve Press Conference 08:30pm UTC+2 (Berlin)

Federal Reserve Press Conference 08:30pm UTC+2 (Berlin)